Figure 1: Left-handed Triangle of Doom from TFC Charts; we aren’t there yet, even with the policy errors by Japanese, Chinese, US government and others. Business as usual appears to be resilient … this is a temporary illusion.

The chart indicates a steadily rising price for crude vs. a steadily declining ability of customers to pay. We live in the world of converging adverse consequences. For instance, in Turkey interest rates must be low to support lending and business activity at the same time interest rates must be high to defend the currency. Ditto India, Russia, Argentina. Drillers need high prices to gain replacement crude, the same high prices undermine the customers’ ability to borrow. Toward the point of the triangle, the price needed by drillers represents an oil shock that undermines our precious waste-based economy. Without high prices there is no fuel at all because the lower-priced varieties have been largely exhausted, there is little remaining in the way of $20 oil to fall back on. Room to maneuver at the end of that gangplank is vanishingly scarce; our impossible choice is to bankrupt ourselves or do without oil.

Bankrupting ourselves is a version of doing without; this is our future. We either choose to conserve voluntarily or we suffer conservation by other means.

The trend toward a higher real crude price is driven by geology. New technology makes hard-to-access crudes and crude-like-substances available but at a steadily increasing real cost, that is, relative to other costs. The output of goods- and services per barrel is the same whether fuel costs $20/barrel or $120. This productivity decline rebounds against the customer/users who are less able to borrow. This in turn rebounds against the driller who is the recipient of the customers’ loans.

At any given moment there is a finite amount of credit. The amount changes from moment-to-moment, but there is no ‘spare credit’. With time, the fraction of credit flowing to the oil driller increases while the fraction remaining for the customer — and the lender — declines. One interest competes against the rest; because of geological constraints, more credit flows to the drillers, less to the customers … even though the drillers are dependent upon the customers for their funds.

Increasing credit to the driller by way of subsidies or tax adjustments cannot change the proportions: the greater- and increasing fraction must flow to the driller and less to everyone else. At some point the the customer is ruined => there is no price support => the price declines and fuel supplies are shut it.

Energy Commodity Futures

| Commodity | Units | Price | Change | % Change | Contract |

|---|---|---|---|---|---|

| Crude Oil (WTI) | USD/bbl. | 101.67 | +0.39 | +0.39% | May 14 |

| Crude Oil (Brent) | USD/bbl. | 108.07 | +0.24 | +0.22% | May 14 |

| RBOB Gasoline | USd/gal. | 293.75 | -0.51 | -0.17% | Apr 14 |

| NYMEX Natural Gas | USD/MMBtu | 4.49 | -0.05 | -1.17% | May 14 |

| NYMEX Heating Oil | USd/gal. | 295.79 | +1.02 | +0.35% | Apr 14 |

Precious and Industrial Metals

| Commodity | Units | Price | Change | % Change | Contract |

|---|---|---|---|---|---|

| COMEX Gold | USD/t oz. | 1,294.30 | -0.50 | -0.04% | Jun 14 |

| Gold Spot | USD/t oz. | 1,295.23 | +3.92 | +0.30% | N/A |

| COMEX Silver | USD/t oz. | 19.79 | +0.08 | +0.42% | May 14 |

| COMEX Copper | USd/lb. | 304.15 | +4.85 | +1.62% | May 14 |

| Platinum Spot | USD/t oz. | 1,408.88 | +9.32 | +0.67% | N/A |

Chart by Bloomberg. Despite saber-rattling in Ukraine and the putative Russian ‘invasion’ there is little in the way of a corresponding oil price increase. Should push come to shove there would certainly be a cut-off or embargo on Russian fuels, ordinarily the prospect would drive crude prices higher. It is possible that uncertainty in Ukraine is outweighed by China deleveraging. Another uncertainty is how a shortage of Russian fuels would affect European credit; chances are it would cause credit to shrink further.

At + $100/barrel, crude prices are historically very high; fuel waste infrastructure in the West as well as in China is designed assuming sub- $20 petroleum fuels into far-distant future. The waste-habitat of freeways, tract houses, concrete towers and fifteen miles between living room and bathroom is stranded at today’s price. All that remains is for users to recognize the losses this nonsense represents => more deflation and less ability to meet necessary high prices.

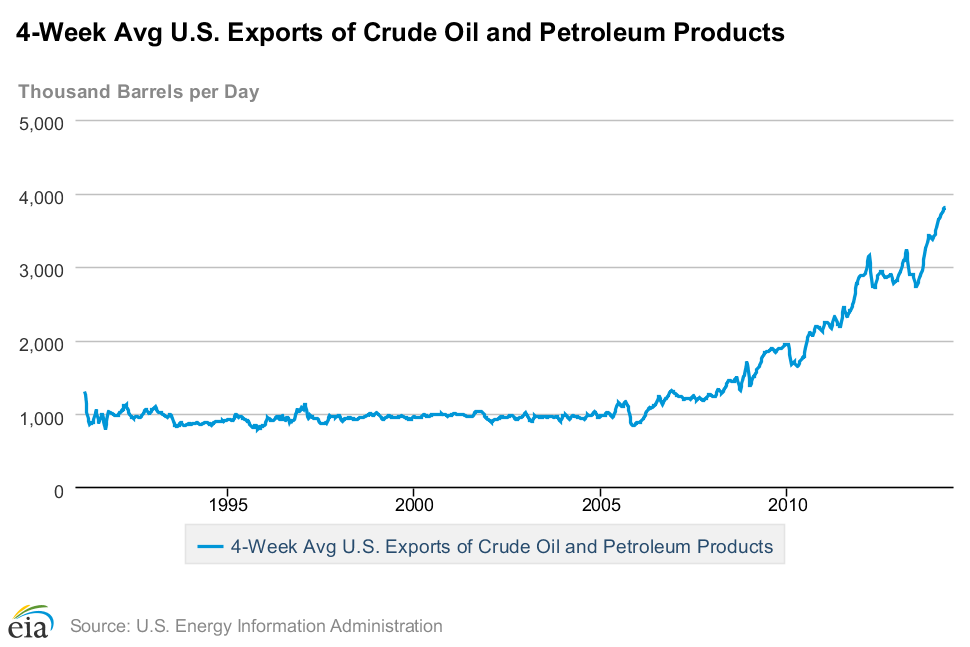

The spread between WTI and Brent crude prices has been narrowing. A cause is increased flows of fuel from the US Midwest oil-producing regions to the coasts and thence to the rest of the world by way of reversed pipelines and rail transport. The trick-of-the-day is for energy companies to refine un-exportable US crude just enough for it to pass as ‘product’ which can be freely exported at the world price.

Figure 2: The trick of the past five years. Exports of petroleum products from EIA; sooner or later, citizens will confront the world price, whether they will afford it is another matter.

Triangulation suggests that there is little time remaining before there is a fuel supply – credit supply ‘problem’. As always, this will catch the establishment off-guard; ‘nobody will have seen this coming’. Keep in mind that the ongoing fuel shortage is not comparable in many ways to previous iterations. It is the result of over-consumption and resource/capital depletion rather than a production bottleneck or gate-keeping by dictators or OPEC. World-wide, there is little if any petroleum spare capacity. The infrastructure to create alternative fuels such as oil-from-coal or oil-from-gas does not exist in a meaningful way: natural gas and other exportable fuels are over-promoted and over-subscribed. Managers’ efforts are directed toward public relations, US energy policy is Sarah Palin’s “Drill, Baby, drill!” A large percentage of US total petroleum output comes from stripper wells that each produce less than 50 barrels of oil per day. In effect, a large national bet has been wagered on oil and gas extraction from shale formations. There is nothing else in the pipeline to replace these sources when they to, ultimately, begin to decline.

Fuel shortage will not take the form of gas lines, odd-even days or the hated ‘double-nickel’ speed limit. Rather, there will be more credit breakdowns and runs out of currencies and banks. Already the cracks are forming … in China, Latin America, in Europe. After credit breaks, the real physical shortages will emerge. Within the waste-based economy, reductions in supply of capital to be destroyed does not make customers richer, so shortages that occur because fuel is unaffordable will be permanent.

As always, it is good to prepare, at least be mentally ready.