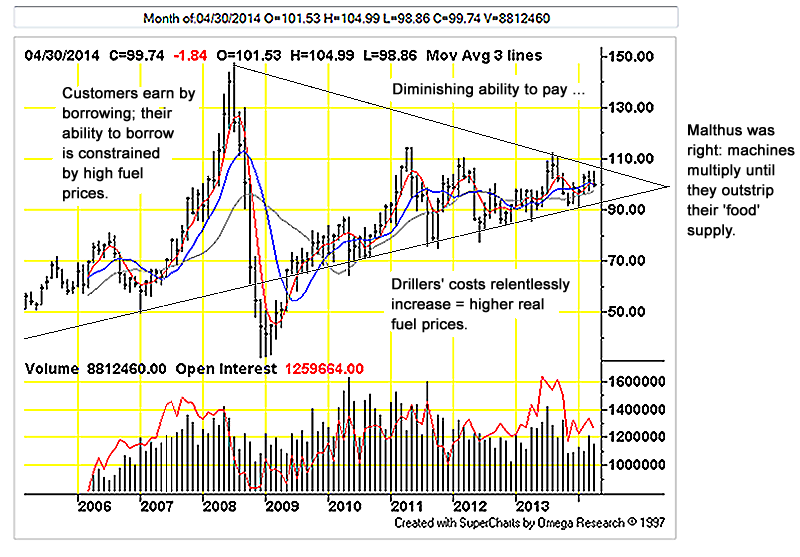

Figure 1: Funnel of Doom (by TFC Charts, click on for big): As we near the end of the auto age we twist in agony, first one way, then the other to avoid our fate, which is to walk everywhere we need to go. Problems are emerging everywhere, not simply car-dependent US and EU; Russia attempts to rattle the saber so as to force fuel prices higher. The outcome: Russia’s foreign exchange collateral flees the country, (Ambrose Evans-Pritchard):

The European Central Bank says capital flight from Russia since the Ukraine crisis erupted may be four times higher than admitted by the Kremlin, a clear sign that sanctions pressure is inflicting serious damage on the Russian economy.Mario Draghi, the ECB’s president, said the outflows from Russia have been large enough over recent weeks to push up the euro exchange rate, complicating monetary policy for the ECB.

“We had very significant outflows that have been estimated by some to be in the order of €160bn out of Russia,” he said, without specifying where the information came from.

This is equivalent to $222bn. It is the highest figure suggested so far by a senior official with access to confidential data. The Russian finance ministry said outflows had been just $51bn in the first quarter, though the total has almost certainly risen since then.

“Draghi’s figure is a huge amount. If this is correct, it shows that Russia is in much more trouble than people think,” said Tim Ash, from Standard Bank. “This is the same scale of outflows we saw in late 2008 after the Lehman crisis.”

Russia needs higher prices so that its oil extraction industry can meet its skyrocketing costs. Putin, like the rest of us, has reached the neck-line of the Triangle of Doom, the pointy-end of the gangplank where there is negligible room to maneuver, where the conventional solutions — such as threats of war to inflate the oil prices — don’t work any more.

There is almost nothing Putin can actually do: he certainly cannot escape the triangle. He dares not risk a conflict with Europe as that would entail Europeans deciding to do without Russian petroleum and gas; this would cause prices to drop, the opposite of what Putin intends. He also dares not risk an outright war with Ukraine that Russia might is certain to lose. He dares not risk a credit embargo, although the market voting with its feet amounts to the same thing. Putin pretends … he cannot control his own destiny.

He cannot afford to build a larger, more threatening army, nor could he use one if he had it. Russia would have to borrow more from London and Frankfurt. Armies like cars are non-remunerative. Anything Putin could gain in a war would be worth less that what his army would cost!

Despite the whoopla and armored brigades, the crude price is holding steady. The best evidence of the oil peak is the inability of the threat of wars in an oil producing- regions to inflate the price. It means the customers cannot borrow any more; they are broke. Under the circumstances, something has to give, if the oil price cannot jump (w/ more funds proportionately flowing to Russian energy companies), the ability of ordinary Russians to buy fuel with roubles must plummet. This is underway right now: Russia’s national account is deleveraging, foreign currency collateral is flying out of the country as fast as Russians can get their hands (computers) on it. To some degree, Russia = Cyprus.

A reason for the flight of funds out of Russia and the other BRICs is the fact of their dependence upon overseas loans in the first place. Countries like Russia and China are desperate to industrialize, to ‘get rich quick’ and damn the consequences. Managers never look to see whether industrialization is appropriate or even possible in their countries, they improvise using whatever comes to hand, relying on funds borrowed from overseas. These outside creditors are both capricious and untouchable; they act with impunity, lending- or withholding funds as the spirit moves them, when there is a better deal elsewhere or after they have assembled short positions in the borrowers’ assets. There is nothing the borrowers can do to control the lenders or protect themselves from the unpleasant consequences when the credit tides turn.

Because there is shrinking (forex) collateral relative to claims against it the Russian rouble is underwater. Like a bank in the midst of a run, the Russians won’t stand aside and watch foreign exchange fly out the window leaving the rouble effectively worthless. Interest rates in Russia will jump. If this doesn’t work there will be capital controls, effectively ‘closing the bank’ … but also cutting off Russian domestic credit — and Putin’s nose to spite his face.

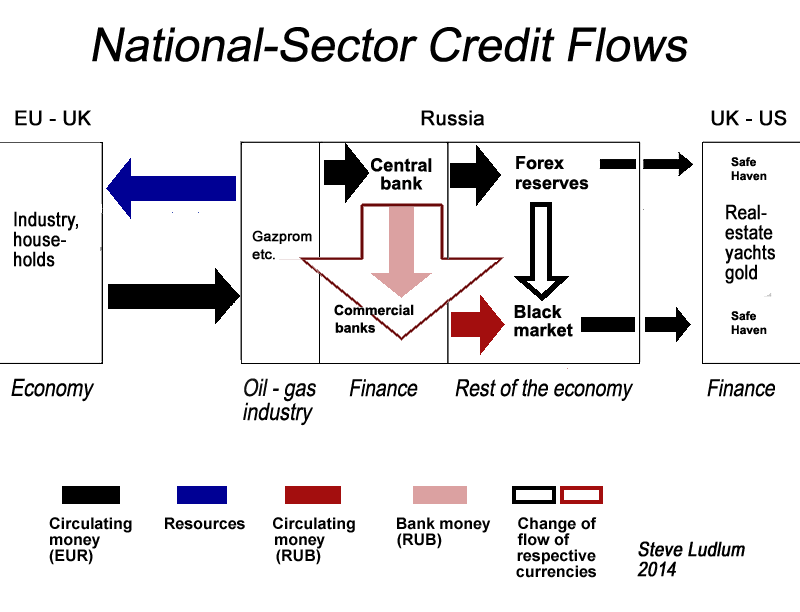

Figure 2: The Russian economy and finance is basically a money-laundering scheme that directs the returns from energy sales to tycoons. Funds flow from EU and UK banks by way of fuel customers to Gazprom and the Bank of Russia. Some funds are held as currency reserves, the rest flow to tycoons’ overseas accounts where they are used to purchase luxury real estate, yachts, artworks, gold and other easily exchangeable goods … The Bank of Russia uses overseas currency as collateral for rouble loans, refunding the roubles to commercial banks, thence into the Russian economy. See ‘Debtonomics; Currency Crisis’ for an explanation of how the process works.

Russia lacks the ability to produce needed organic credit, it lacks infrastructure including strong banks, a freely tradeable currency, goodwill and the rule of law; instead there are weak banks, a rouble that circulates little outside of Russia, absence of trust and arbitrary rule by Putin. Because Russian credit is no good the country requires overseas loans from European lenders acting indirectly through Russia’s energy customers.

Industrial modernity requires a credit subsidy to function. A constant flow of new funds into Russia from overseas is necessary as the leakage to tycoon safe-havens is a collateral drain with an accompanying reduction in rouble purchasing power. If Russia holds onto its collateral the tycoons are starved of funds. The alternative is for the Bank of Russia to make unsecured loans to its commercial bank clients in an attempt to ‘make good purchasing power losses with volume’. The outcome is there is no lender of last resort and bank runs … which are underway right now.

Unsecured rouble lending by Bank of Russia is indicated by red-outlined arrow. Weak Russian banks are unable to distribute their own losses into the Russian economy, attempts to force such losses results is a vicious cycle- black market currency arbitrage leading to hyperinflation as in Argentina, Venezuela, Belarus, Iran and previously in Russia, itself. Citizens and speculators use whatever local currency they can get their hands on to ‘purchase’ the desired hard currency heedless of the affect on the exchange/inflation rate as indicated by the black-outlined arrow.

The ground rules are changing under the Russians’ feet; it is possible their foolishness will by itself trigger the exact crisis they are desperate to avoid. Events that signal major economic turning points can be hard to identify as they occur; the background accompaniment tends to be rising borrowing costs that are added to already-bankrupting fuel costs.

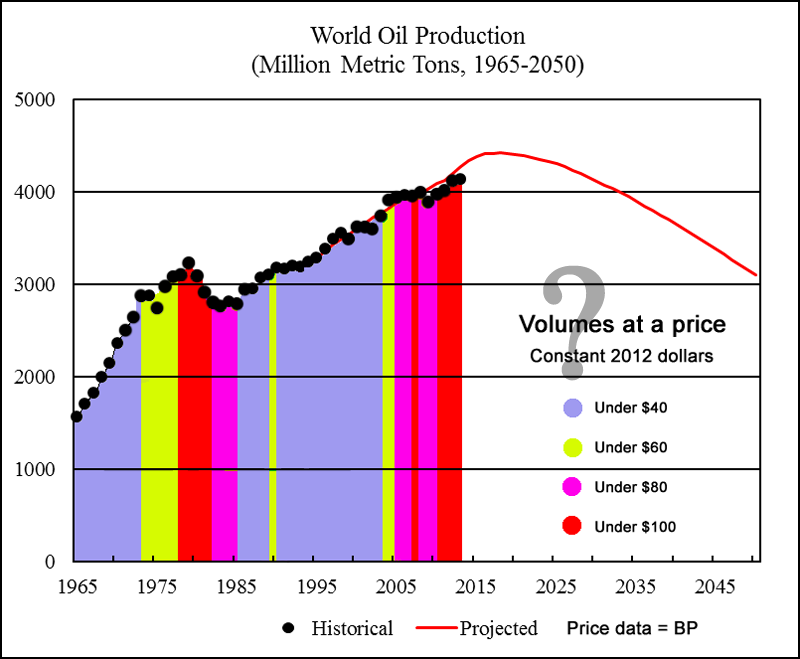

Figure 3: Chart by ‘Political Economist’ by way of Ron Patterson’s ‘Peak Oil Barrel’, (Click on for big). A record of cumulative crude- and condensate (C&C) since 1965 with prices in constant 2012 dollars (from BP Statistical Review).

Notice that the bulk of C&C extraction cost less than US$40 per barrel; prior to 1973, the inflation adjusted cost was less than US$20.

Back of the envelope calculations give the following quantities at different price levels:

- Less than $40/barrel (2012 dollars) = 73,175 million metric tons since 1965.

- Less than $60/barrel (more than $41) = 23,050 million metric tons. It’s likely that oil in the sub-$60/barrel price categories has been completely exhausted, all that remains is petroleum and near- petroleum substances that are more costly to extract.

- Less than $80/barrel (more than $61) = 20,200 million metric tons.

- Less than $100/barrel (more than $81) = 35,300 million tons. roughly 12,000 million MT of this crude was extracted during the period of Middle East wars that occurred during the 1970s and early 1980s.

Without the wars and their affect on transport, it is likely that crude price would have remained $40/barrel or less ($16/barrel in 1972); there was no shortage of petroleum in the ground and demand was inelastic. Higher rates of consumption at lower prices would have brought forward the onset of depletion-related difficulties that we are facing now. Critics of Hubbert linearization point out that it does not adjust for changes in oilfield technology. It also cannot adjust for above-ground interruptions in the consumption regime: the various Middle East conflicts in the seventies and eighties put off the world oil extraction peak by about ten years.

The question mark in figure 3 represents what crude are we going to use going forward? Peak oil analysts insist that the production plateau does not mean ‘running out of oil’. It is hard to see it meaning anything else when the only petroleum our economy can afford has already been burned up.

The suggestion that similar amounts of fuel will be available after extraction peak as before is not borne out by cost/volume analysis. The lower-priced, sub- $60/barrel fuels have been exhausted; lower price made fuel a loss-leader for the burgeoning automobile industry; the consequence of low prices was a world filled with cars and accelerating rates of depletion. Lower costs reflected the ready accessibility of pre-2000 crudes: volumes were easy to extract from large, conventional onshore- or shallow-water offshore formations. Going ‘up’ the extraction rate curve was affordable with relatively little credit being required, the external costs were easily pushed into the future.

The fuels we have today are not the same fuels we used to build out our consumption infrastructure. We have cleverly trapped ourselves: we must support higher prices because there are no low-priced fuels available. At the same time, our waste-infrastructure does not offer returns that would support the higher prices! We either bankrupt ourselves with loans from criminals to support our lifestyles or learn to do without.

Figure 4: oil price chart from BP. Nominal prices from the end of the 19th century to 1973 were less than $10/barrel; from the 1978-82 period to the late 1990s the nominal crude price did not reach US$40/barrel. Nominal wages during this period were also very low. Fast forward to the present; wages have been stagnant since the late-1990s while cost of fuel has jumped in both nominal and real terms by over 500%.

What is emerging from background noise is current business practices offer the prospect of geometrically expanded costs for credit and fuel access … without end. Automobile waste was a losing proposition at $15 per barrel, genius is not required to imagine how poisonous $95 per barrel is to the same enterprise. Our economy does not meet its ordinary expenses by way of cash flow, we are insolvent. We are able to ‘fake it’ for a little while; this is because finance is willing to lend … until we are undone by the absence of real returns and our refusal to face reality.

Figure 5: Enter American Dream- killing four dollar gasoline; the heat map from GasBuddy.com. (Click on for big.) Fuel industry costs emerge in wealthy California where residents are better able to stump up for fuel; in lesser parts of the world, folks address the structural fuel constraints by not buying.

Californians create the constraints the same time they battle its effects by destroying every bit of gasoline they buy! They are trapped like the Russians. If they continue to drive they push the cost of gasoline to the level where demand is ‘effected’ and the price cannot be met, where consumers begin to vanish. At the same time, Californians cannot afford to stop driving, they have invested too much in the process. Aside from speculating in real estate, the entire economy of the state — as well as the rest of the developed world — revolves around buying and using cars for everything.

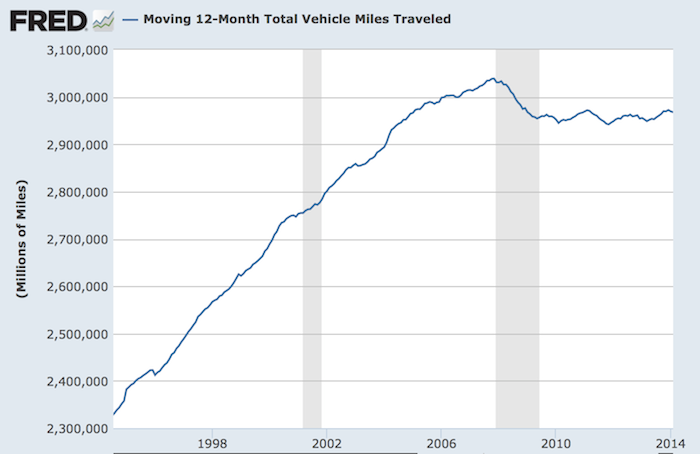

Figure 6: Vehicle Miles Traveled by way of the St. Louis Fed: Americans by right should be driving 3.6 trillion miles this year but are stuck in reverse. Sadly, less driving has little effect on the fuel price, there needs to be far less driving and less fuel waste, this would reduce prices further but would bankrupt oil drillers at the same time.

China finds itself perched at the end of the same triangular gangplank as the Russians, (New York Times):

China Flexes Its Muscles in Dispute With VietnamJane Perlez and Rick Gladstone

BEIJING — China’s escalating dispute with Vietnam over contested waters in the South China Sea sent new shudders through Asia on Thursday as China demanded the withdrawal of Vietnamese ships near a giant Chinese drilling rig and for the first time acknowledged its vessels had blasted the Vietnamese flotilla with water cannons in recent days.

While China characterized the use of water cannons as a form of restraint, it punctuated the increasingly muscular stance by the Chinese toward a growing number of Asian neighbors who fear they are vulnerable to bullying by China and its increasingly powerful military. The latest back-and-forth in the dispute with Vietnam — the most serious in the South China Sea in years — sent the Vietnamese stock market plunging on Thursday and elicited concern from a top American diplomat who was visiting Hanoi.

Political and economic historians said the China-Vietnam tensions signaled a hardening position by the Chinese over what they regard as their “core interest” in claiming sovereignty over a vastly widened swath of coastal waters that stretch from the Philippines and Indonesia north to Japan. In Chinese parlance, they say, “core interest” means there is no room for compromise.

Chinese saber rattling is no different from the Russians. The desire is to reflate the economy and push prices higher, to forestall deflation or ship it overseas to its trading partners. This endeavor is certain to fail, like Russia viz Ukraine, China dares not risk a war with violent and militaristic Vietnam which has been the graveyard of Chinese ambitions for centuries.

Like Russia, China is dependent upon Western (dollar) credit. Collateral for China credit and its currency (RMB) is trillions of US dollars, euros, yen and sterling. When overseas credit flows out of China, RMB purchasing power evaporates. Unlike Russia, China has strong banks, tens of trillions of bank system losses have been distributed into the Chinese economy in the form of worthless infrastructure, all that remains is for the extent of these losses to be revealed as the credit tides flow out.

China is dependent upon the solvency of its biggest customer and credit provider, the US. As the Land of the Free becomes the Land of Out of Reach, so does China at a remove. China also goes broke for reasons its own. One is the government’s ‘Tapering Error’; it must reduce the flow of RMB credit and face the inevitable consequences. The alternative course is to continue with credit expansion which offers sharply diminished returns. Credit shrinkage will remove a large part of World fuel- resource demand along with support for petroleum drillers.

China is overdue for an ordinary inventory-driven business-cycle recession, not having experienced such a slowdown since the country began to modernize during the mid-1980s. China also faces what Richard Koo calls a ‘balance sheet recession’. China’s finance losses overhang the economy, these reside uneasily as ‘assets’ on China’s ledgers. Deleveraging reveals assets as worthless, which causes further deleveraging which in turn reveals more losses in a vicious cycle. China has little in the way of effective tools to manage this sort of thing: it is at the end of a long regime of very easy credit. Since 2008, there has been a ‘money dump’ by SOE (state-owned enterprise) banks and shadow- ‘loan shark’ banks. Once enough foreign exchange collateral flees there is likely no more easy credit to be had. China’s currency will be underwater, essentially worthless.

The land of 1.2 billion faces an agricultural emergency. As much as seventy-percent of China’s land and water contaminated with metals and mining waste, toxic chemicals and fertilizers; pesticides, sewage runoff and pharmaceuticals, fuel, smog components, soot and radionuclides (mostly from coal burning). This leaves out agricultural land and watershed areas surrendered to urbanization, desertification plus the over-draw from aquifers. This takes place within the context of global warming, driven to a large degree by aggressive Chinese industrialization and massive fossil fuel waste.

China is also subject to dollar-preference, the desire to hold dollars because of what can be obtained with them relative to what can be had with other currencies or by way of barter; the eagerness of locals to trade local currencies to gain dollars at any price; the ‘currency war’.

Russia claims it can offset losses in the West with trade gains from China. This is nonsense; Russian managers don’t understand that China is just as dependent upon Western credit and flows of funds as Russia, itself.

Our fuel system exists to support the automobile industry and all its dependencies. Take away the autos and there is a vanishingly small need for petroleum, the reverse is also true: take away or diminish the fuel system and the autos are stranded along with all the frivolous junk that has been put into service to rationalize universal auto use. None of these bits of junk pay for themselves; what is occurring in Russia and China and their trading partners is the necessary coming-to-grips with both credit- and resource limits. Malthus was right; machines multiply until the outstrip their supply of ‘food’; the outcome is catastrophe, coming to a freeway or strip mall near you.