Note Brent/WTI crudes, from Bloomberg:

Energy

| PRICE* | CHANGE | % CHANGE | TIME | |

|---|---|---|---|---|

| BRENT CRUDE FUTR (USD/bbl.) | 102.000 | 0.180 | 0.18% | 08:57 |

| GAS OIL FUT (ICE) (USD/MT) | 864.500 | 6.500 | 0.76% | 08:57 |

| HEATING OIL FUTR (USd/gal.) | 275.280 | -1.610 | -0.58% | 08:57 |

| NATURAL GAS FUTR (USD/MMBtu) | 4.020 | -0.024 | -0.59% | 08:57 |

| GASOLINE RBOB FUT (USd/gal.) | 251.750 | -0.850 | -0.34% | 08:57 |

| WTI CRUDE FUTURE (USD/bbl.) | 86.240 | -0.470 | -0.54% | 08:57 |

Another thing to notice is WTI is within a few trading days of falling below $80. That would be a ‘risk- off’ indicator and would suggest closing dollar- short positions.

There is a glut of fuel @ Cushing: there is likely a glut of fuel elsewhere but the Brent price does not currently reflect it. Traders are ‘selling’ the US price premium to hapless Europeans and Asians desperate to drive their first car.

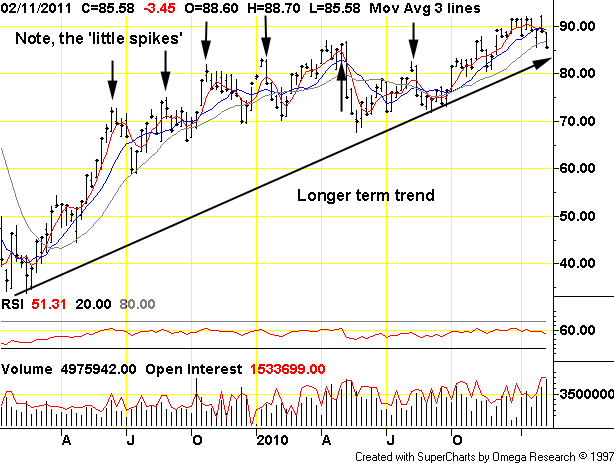

Last year Nymex crude would hold +$80 for short periods then decline as the market turned up its nose @ the high prices. This is a chart from TFC Chartz:

Price spikes since the low in in Spring of 2009 have been- self correcting up until the past couple of months.

Right now, Nymex crude is near the critical $83- 84 support level. The break to the downside makes $80 the next level of support. This presumes the self- correcting mechanism of high prices restraining demand remains in place.

Holding the price below $80 would break the medium- term trendline and suggest the bull market in crude that has existed since Spring of 2009 is over. Since the high in 2008 the oil market has experienced a bull rally in a longer- term bear market similar to bear market rallies in stocks and commercial bonds. A return to the bear trend in crude would mean bear markets elsewhere as well as deleveraging and redemptions. Under the current regime of structural imbalances and defective central bank strategies such deleveraging could prove chaotic.

A break in the bull euphoria would certainly be embarrassing to the US establishment which has been shamelessly pimping ‘recovery’. Predicting the future is beyond anyone’s grasp but sensible people should be able to acknowledge what is taking place right under their noses! High oil prices have devastating consequences.

Prices have been pushed upward by flows of finance credit into commodity markets. This is a tactic of central banks: credit formation is both the parent and child of negative real interest rates alongside moral hazard. There are problems with this this tactic:

One is that this credit is not coupled to real output. Rising prices are a finance market phenomenon that sits on top of indifferent organic demand. Finance’s ‘fake money’ is lent against trillion$ in worthless mortgage collateral rather than ongoing business activity. Accompanying this farrago is the eagerness of governments to lie and a parallel willingness on the part of the public to believe the lies. Finance’s credit cannot be anything but fake. Real productive/output is constrained by the same high fuel prices which are the outcome of finance fakery, market manipulation along with the disappearance of easily accessed ‘cheap oil’.

Another problem is that high fuel costs embedded in food and other basic goods put entire populations under siege. People can stop driving at small cost to themselves: everyone in the world wakes up hungry every morning. Americans fixate on the pump price of gasoline but high fuel costs emerge in the final price of all goods and services. Cash- strapped customers must somehow stump up for goods and services: if they cannot the producers fail. In developed countries this failure widens the already large output gap or ‘slack’.

In nations where basic survival costs represents final demand the ‘producer’ is the government. Corrupt ruling elites skim producer ‘profits’ and send them overseas to tax havens even as fragile allocation structures collapse.

Slack by itself does not allow declining prices because it includes components idle due to business failure. Slack is the graveyard of ‘entities’ that are unable to pass on or absorb high input costs.

As customers disappear and profit margins shrink firms must raise prices. Companies export wages and final demand overseas. Governments raise taxes and cut services. The outcome is cash- strapped customers forced by the high prices to ration their purchases. For consumption economies based on retail sales and marketing, this is a death sentence.

The deflationary cycle of business failure is entrenched and feeding on itself. This takes place silently, even as economists’ flim- flammery insists the economy is ‘recovering’.

Attempts to mitigate cost- push effects on consumers shifts costs but does not eliminate them. Fuel subsidies provide incentives to wastefully consume more fuel. Food subsidies are paid out of revenue that would ordinarily be used elsewhere more productively. Fuel constraints impose a ‘Zero Sum’ regime where activities in one area or sector take place at the expense of activities elsewhere. Instead of voluntary conservation which allocates rationally away from sensitive distribution networks and productive activity, ‘conservation the hard way’ bludgeons distribution networks triggering cascading vulnerabilities across economies.

The credit miseries in the Eurozone are of a piece with conservation the hard way. To support the auto-centric waste-based EU economy, the stability of the whole is undermined by the inability of fuel consumption activities to fund themselves. Greece fails first, then Ireland: Spain and Italy tremble on the brink of the abyss. Who follows them? Conservation the hard way cares not for Irish pensioners, Latvian school children or UK bank investors: it acts to annihilate all.

It would be better for Europeans to surrender a percentage of their cars and use the liberated funds to restructure their members’ solvency while saving fuel @ the same time. The cars will be surrendered no matter what happens. What is unsustainable will stop; the issue is whether the stopping process can be made practical.

High fuel prices increase risk and volatility out of proportion to what supply and demand by themselves would indicate. Alternatively, dropping fuel prices signal an end to the effectiveness of central banks’ monetary masturbation. Credit markets are saturated with unproductive liquidity. Finance seeks to substitute credit for fuel which is pointless and stupid. The act of forcing rates by itself calls into question whether monetary policy can effect output or demand at all. This is not a good question for the banks.

Here is the current Treasury yield- curve chart from the estimable Doug Short. (Please click on chart for a larger image):

Notice that all Treasury maturities have increased in yield since the Autumn of last year except for bills. Since the Fed has been buying two-to-five year Treasuries as part of QE2, the implication is that the Fed has no control over the debt- pricing process. The Fed’s rationale for quantitative easing in the first place was to force longer- maturity Treasury yields lower. Obviously, the Fed has failed.

For those who read this blog, this is no surprise. The centrality of fuel to the world’s economies and the relationship between money and crude — the free exchange on demand of one for the other — renders both central banks and monetary ‘policy’ irrelevant.

If $92 WTI or Brent $102 represents the upper bound, any decline in fuel prices due to cost revulsion represents a corresponding increase in dollar value. The upper bound is the price level that cannot sustain economic activity for more than a very short period. That the upper bound is at current levels is reasonable. The average 2008 price for crude was $97 per barrel. The period of extremely high ‘spike price’ which reached $147 was relatively short. It was the long period of + $90 oil and the years of high prices leading to the $90 level that bled out the lending bubble economy. Prices approaching $100 on world crude markets are having the same effect right now.

Easy money creates the illusion of economic health while undermining that health @ the same time. Here is another chart of the rate of change in Treasury yields beginning with the Great QE2 Science Experiment; (click on this chart for much larger version):

This is the rate of change in yields, not the yields themselves. Pay attention to the 2 year yield. Right now QE is counterproductive. So much risk- free credit being made available that it isn’t risk free anymore. What the rising rates indicate is the cost of cash in Treasury credit is rising. The Fed is pushing on a string to make itself relevant but this effort has failed. Now what?

Once the markets see that the Fed cannot effect outcomes its ability to act as a ‘fireman’ and lender of last resort evaporates. We are witnessing in real time the decline and fall of the Fed Chairman’s final attempt to overcome the policy- making power of hundreds of millions of US drivers. Since the Fed has been a primary enabler of sprawl, highways, automobiles along with the finance industry that supports it all, the Fed is revealed as its own worst enemy.

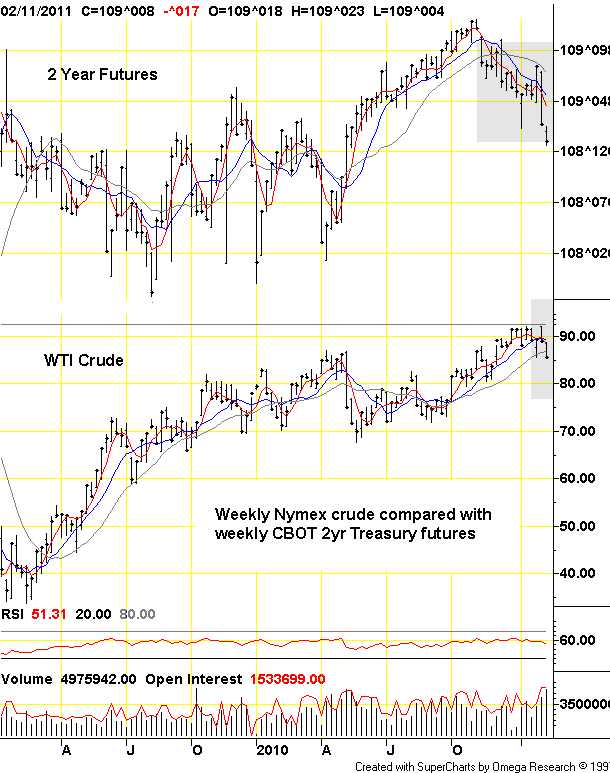

Here is a chart of WTI futures compared to Chicago Board 2yr Treasury futures. Yields rise as prices decline. As you can see, the market for the 2yr began to decline months prior to the current decline in WTI crude. As credit becomes more expensive, the ability of customers to ‘borrow and bid’ for energy- and other products shrinks.

Oil prices decline not because of more supply hitting the market but that oil customers are broke and cannot borrow. Customers are broke because they don’t make any money ‘using’ oil. Adding more credit solves nothing: only a restructuring of the economy away from waste will work!

Treasury yields are leading this market: risk accumulates across all markets. There are murmurs of haircuts and defaults, restructurings and a massive and growing overhang of Treasury supply. All of these along with a real economy that is fatally hobbled by its designed- in non-productivity. Higher rates are to come. Priced in credit cash dollars will become ever- more valuable.

Cash- preference takes place alongside is the likely decline in fuel prices as users balk at paying out of declining discretionary income. Welcome to the new world of conservation the hard way, with nothing in the way of mitigating mechanisms put into place to alleviate effects on our most vulnerable.

But conservation it is, and there is no way around it.