Christmas comes early to the world’s children in the form of unlimited supplies of fracked shale oil and gas for all. So says Fatih Birol and company over at the International Energy Agency:

The tide turns for US energy flows!Energy developments in the United States are profound and their effect will be felt well beyond North America – and the energy sector. The recent rebound in US oil and gas production, driven by upstream technologies that are unlocking light tight oil and shale gas resources, is spurring economic activity – with less expensive gas and electricity prices giving industry a competitive edge – and steadily changing the role of North America …

Etc.

The world is in the middle of three intertwined crises right now: a finance crisis, a petroleum energy crisis and a climate crisis. A characteristic these three crises share is that all of them are denied … or the truth is massaged by the establishment or those who claim to speak for it. Promoters of finance recovery regularly assure continued growth regardless of circumstances, climate cheerleaders downplay the effects of fossil fuel waste gases in the atmosphere while fuel supply experts find lakes of crude oil wherever they choose to look.

The finance-recovery promoters are diverse and include the Federal Reserve, the IMF and the European Commission.

Figure 1: Economic reality = structural unemployment. The purchasing power of workers declines: this graphs the duration of unemployment. Happily, as people reach the end of unemployment benefits they drop off the list of available workers, unemployment looks better than it really is!

Without income from gainful employment, there are diminished earnings for industries both in the US and elsewhere. Happily, industrial firms can earn by speculating in finance markets: making and selling real goods is unnecessary.

Behind the curtain, actions are more eloquent than (soothing) words. There are ongoing monetary easing programs in the US and elsewhere, elsewhere and elsewhere. If conditions are as pleasant as the cheerleaders insist, there is no need for stimulus. Right?

Meanwhile, the climate crisis is denied:

There is an entire cadre of shills — subsidized by the energy industry — who regularly appear across the breadth of the media-sphere as well as before Congressional committees where they are ‘warmly’ received. There is little strategic space between the climate denial creatures and the extinct smoking-tobacco-is-good-for-you versions. The idea is to sow uncertainty among the public so that the businesses tycoons can continue to make money. ‘Success’ for the one-percenters comes first … everything else is secondary.

Comes now the petroleum shortage deniers, who like the others, are ‘experts’ with impressive-appearing credentials fronting similarly-situated organizations. The international media — dependent as it is on car advertising — eagerly grasps the good news with both hands and runs with it. The public is happy to be reassured that there is nothing really wrong with fuel supply.

If there fuel supply conditions are as favorable as the experts insist, reassurance is unnecessary … right? Here is reassurance from the New York Times:

The United States will overtake Saudi Arabia as the world’s leading oil producer by about 2017 and will become a net oil exporter by 2030, the International Energy Agency said Monday. (Gasp!)That increased oil production, combined with new American policies to improve energy efficiency, means that the United States will become “all but self-sufficient” …

Etc … Here is more from the Financial Times:

Fatih Birol, chief economist at the International Energy Agency, the western countries’ oil watchdog, says Europe spent €32bn to import oil in March. This month, the bill is on track to be €27bn. In the US, oil imports cost $33.5bn in March, and will be $27.5bn in June, he says. Emerging economies, particularly China, Indonesia and India, should see fiscal burdens fall as lower subsidies are required.

Everyone has heard it all before, over and over and over and over. Here is spam from ex-petro company executive Leonardo Maugeri at MIT:

Oil: The Next RevolutionTHE UNPRECEDENTED UPSURGE OF OIL PRODUCTION CAPACITY AND WHAT IT MEANS FOR THE WORLD!!!

Contrary to what most people believe, oil supply capacity is growing worldwide at such an unprecedented level that it might outpace consumption. This could lead to a glut of overproduction and a steep dip in oil prices.

Based on original, bottom-up, field-by-field analysis of most oil exploration and development projects in the world, this paper suggests that an unrestricted, additional production (the level of production targeted by each single project, according to its schedule, unadjusted for risk) of more than 49 million barrels per day of oil (crude oil and natural gas liquids, or NGLs) is targeted for 2020, the equivalent of more than half the current world production …

Etc.

“Will overtake Saudi Arabia” … “will become a net oil exporter” … “might outpace consumption” … all these weasel words: “could lead to a glut”, perhaps tomorrow … and perhaps not! With industrialists the utopia is always set to arrive tomorrow provided access to capital is “unrestricted”! Keep in mind, if what Maugeri and Birol were saying was true, the effect would be obvious and there would be no need for anyone to say anything! Fuel prices would decline and the economy would expand. Fleets of new machines would be deployed to waste the newly extracted fuel. This is not happening, the shills are simply lying.

Public relations campaigns have no effect on reality. The countries suffering financial distress continue to falter, despite the best worst efforts of the European establishment. The finance crisis has continually deepened since it appeared in 2007. More countries are afflicted with the passage of time. There are no signs that any conventional economic policy efforts will solve anything: it says here that they won’t.

Climate conditions have also deteriorated. What has undermined the climate deniers hasn’t been picky arguments of scientists, rather it is repeat bouts of severe weather and the burdensome costs to the insurance industry. The scientists are now in the happy position of being able to say, “I told you so!” … even as their houses are washed away by floods and hurricanes.

Petroleum extraction and consumption are bounded by costs. The shills never mention the current cost of fuel relative to prior years’ cost … or to what customers can afford. It is the change in price relative to what customers can support over the past ten years that is ‘fracking’ the world’s economies! This ‘real’ price has changed because the supply rate has not kept pace with demand. What is underway is fuel rationing by price and access to credit.

The shills assume — and some non-shills as well — the world’s economies will continue to function as-per-normal in the background with the customers simply stumping up out of spare change whatever amounts the petroleum industry demands. The shills fail to acknowledge that high fuel prices — as well as high credit costs — bankrupt firms and press upon individuals. Fuel rationing by price and access to credit isn’t just a collection of meaningless sounds, it is a dynamic which has smashing effect. Without the bankruptcies … the rationing process would not work! There would rise in its place some other baleful process to ration fuel … as indeed there will be when the credit system finally breaks down. When credit ceases to meter access to markets, there will be permanent physical shortages, allocation will be made by police means.

The effects of aggregated costs aren’t restricted to the lowest rungs of the economic ladder: national governments and large finance entities such as multinational banks are impacted. Costs matter.

Whatever the Europeans pay for fuel right now is too much. Every bit of that €27bn mentioned in the Financial Times article is borrowed … and each month’s €27bn thereafter … month after month, year after year. This is the reason Europe is broke! High cost per-barrel crude oil has destroyed the European economies. There is no organic return on the use of the oil, most transportation usage is simply waste for ‘convenience’. Filling the ‘Waste Gap’ between what crude costs and the zero it returns requires a modest debt-subsidy at €20 per barrel. While the lower price is destructive over long periods, the current higher price destroys that much faster.

America’s $27 billion for its monthly fuel is also borrowed: like the Europeans, the claims these loans represent are added to the tens of trillions of outstanding claims. These obligations cannot be repaid by the use of the petroleum or they would have been paid already! Rather than organic earnings the wasting process is offered as collateral for endless rounds of new loans.

Up until a decade- or so ago the ‘waste-collateral-loan’ cycle has been virtuous. Credit extended against the wasting process was sufficient to bring large volumes of fuel to consumers. Both fuel costs and real credit costs were affordably low. When the higher real cost of credit is added to the current cost of fuel the economies’ fuel waste infrastructure is stranded. Suburbs, toll-roads, autos, airports, vacation ‘villas’ … banks and government benefits … are unaffordable luxuries. Even when the customers can afford to buy fuel … they cannot buy a new house or a new car. The industries that provide these goods are worn down then broken: this is the effect of fuel rationing by limiting access to affordable credit.

Adding more high-cost fuels is pointless because the low-return, credit-dependent economy can only pay for it if cuts are made elsewhere … this is why there is an economic crisis in the first place! Fuel and credit inputs cost too much for an economy whose wasteful infrastructure provides minuscule organic returns.

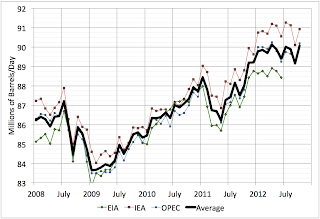

Figure 2: Despite the hoopla there is no sign of any net increase in world petroleum extraction. Maybe cost has something to do with this (Stuart Staniford). Add to the hard numbers the periodic appearance of shortages here and there in the country indicates a breakdown.

{kind=link}

Here is something else the ‘smart people’ don’t talk about (from an article in May), the credit demands of consumption versus the credit demands of the petroleum industry.

Figure 3: Chart by Jeffrey Brown: compare the bolt in demand in this chart to the missing output on the Staniford chart. Every day in this world millions more people want a car:

Net export guru Brown does not include demand on his chart because it cannot be measured with certainty, however it exists everywhere in the world there is a TV set and paper money. Prior to 2002, extraction was able to remain comfortably ahead of demand (for the most part). Excess became spare capacity or was shipped into inventories. The outcome was the plunge in fuel prices to $12 per barrel and less in 1998. Since 2005, the rate of extraction world-wide has stalled while demand in China, India and elsewhere has exploded. High-cost technology and new oilfields have not been able to push supply even as depletion from existing fields accelerates with the drillers falling farther behind.

Consumption is a matter of infrastructure: oil drilling infrastructure cannot lift crude as fast as auto factories, house builders and banks can create consumption … or demand that is impossible to satisfy. Debt-dependent drillers with high-cost plays must compete with consumption for a shrinking pool of lendable funds. Consumption must borrow otherwise it cannot service its debts. By doing so consumption crowds out the drillers. When consumption is unable to borrow, the effects cripple drillers as well as the rest of the economy. Right now drillers can fund themselves … what happens tomorrow?

The petro-shills have gotten ahead of themselves. It is too early to determine how much crude oil- and crude-like substances will be made available in the future in a margin-challenged enterprise. Success depends upon costs and what the customers are able to pay. So far, the best-efforts of the drillers work against the drillers themselves! The flood of product depresses prices at the wellhead where the market price of the product is uncomfortably close to the cost of extracting it. A reason for this is the rapid decline in the rate of flow for individual wells. A sequence of repeat wells is needed to maintain the flow rate.

Is Shale Oil Production from Bakken Headed for a Run with “The Red Queen”?Rune Likvern

In this post I present the results from an in-depth time series analysis from wells producing crude oil (and small volumes of natural gas) from the Bakken – Bakken, Sanish, Three Forks and Bakken/Three Forks Pools – formation in North Dakota. The analysis uses actual production data from the North Dakota Industrial Commission as of July 2012 from what was found to be a representative selection of wells from operating companies and areas.

MAJOR FINDINGS FROM THE STUDY

Findings from this in-depth study of time series for production from some individual wells:

– Presently the estimated breakeven price for the “average” well in the Bakken formation in North Dakota is $80 – $90/Bbl In plain language this means that presently the commercial profitability for new wells is barely positive.

– The “average” well now yields around 85 000 Bbls during the first 12 months of production and then experiences a year over year decline of 40% (+/-) 2%

– The recent trend for newer “average” wells is one of a perceptible decline in well productivity (lower yields)

– As of 2007 and also as of recent months, the total production of shale oil from Bakken, has shown exceptional growth and the (relatively high) specific average productivity (expressed as Bbls/day/well) has been sustained by starting up flow from an accelerating number of new wells

– Now and based upon present observed trends for principally well productivity and crude oil futures (WTI), it is challenging to find support for the idea that total production of shale oil from the Bakken formation will move much above present levels of 0.6 – 0.7 Mb/d on an annual basis.

Of course, like other industrial enterprises the drillers can borrow — against fictional collateral represented by their ‘reserves’ — but not forever.

Meanwhile, high costs and modest returns, rapid decline rates and the absence of distribution infrastructure are adversely effecting the shale gas efforts. See Chris Nelder for a detailed critique of the shale gas industry. According to Art Berman the enterprise is another credit-driven speculative bubble.

“Money is pouring in” from investors even though shale gas is “inherently unprofitable,” an analyst from PNC Wealth Management, an investment company, wrote to a contractor in a February e-mail. “Reminds you of dot-coms.”

There is nothing new about the establishment’s self-deluding nonsense. On October 15, 1929 …. exactly nine days prior to the great stock market crash on ‘Black Thursday’, National City Bank (Citibank) boss Charles Mitchell remarked:

… the ‘industrial condition of the United States is absolutely sound,” that too much attention was being paid to brokers’ loans, and that “nothing can arrest the upward movement.” … he enlarged on the point: “The markets generally are now in a healthy condition … values have a sound basis in the general prosperity of our country.” That same evening Professor Irving Fisher made his historic announcement about the permanently high plateau and added, “I expect to see the stock market a good deal higher than it is today within a few months.” [1]

In 1929 much of the world’s business was invested to some degree in the stock market, certainly Mitchell and Fisher were both very wealthy men by way of stock investments. Today, moderns are equally-invested in the waste-based economy. There is a herd, there are few that will run against it … to do so is unprofitable.

When the stock market collapsed much of the world’s finance capital was destroyed because it was used to support prices as ‘call money’, to leverage stock holdings. Right now, the world’s finance capital is used to leverage fuel waste activities. Birol, Monckton and others are doing now what Fisher and Mitchell were doing in 1929.

There was a sense of panic in the air starting in 1928, increasingly so during the last surging runup to the October crash. The upward movements in the tape were fabulous, hard to believe. Market participants understood they “had a wolf by the ears and dared not let him go”. The establishment was cornered: any effort to relieve the speculative pressures — by constraining call money or cracking down on speculators — would trigger the market collapse that the establishment was desperate to avoid. No one wanted the blame: as it was, the inevitable consequence of the speculation was the crash occurring anyway.

The same dynamic is in effect now. Any official pronouncement of petroleum shortage would cause the finance markets across the world to implode. The ‘Planet Earth Inc.’ business experiment teeters at the edge of economic abyss. In Greece, Portugal, Ireland and other previously-prosperous states, depression is a real fact on the ground. Both ordinary and extraordinary monetary and fiscal remedies have been applied repeatedly to no effect. Credit, banking and money are blamed but the disaster continues to unwind as if credit, banking and money are peripheral to it.

Modernity has made an economic virtue of waste, while the hegemonic tendency of modern ‘culture’ disallows the consideration of any alternatives: we moderns are constrained by fashion sense run amok. Meanwhile, our destiny is bound to be determined by circumstances that our waste has set in motion. One way or the other our fossil fuel consumption is to be brought to an end, whether this ending is profitable to us or not. Only that part is under question: are we humans clever and disciplined enough to CHOOSE … to earn the return on conservation. The overall outcome is not in doubt, we will conserve regardless of consequences or as result of them.

– ‘The Great Crash’ John Kenneth Galbraith pp.99 (Houghtin-Mifflin)