This is the time of year when people look back over their Christmas gifts and take stock of them, to determine whether they meet ‘expectations’. What we have received this year, expected or not, is public relations campaigns and uncertainty … inside the shiny packaging is more of the same; nothing has been fixed either inside or outside of finance. The problems multiply; the same persons run the same civic- and business establishments, there is the same technology and the same promises; meanwhile, the shadows lengthen.

One Christmas present we all received last year, like it or not:

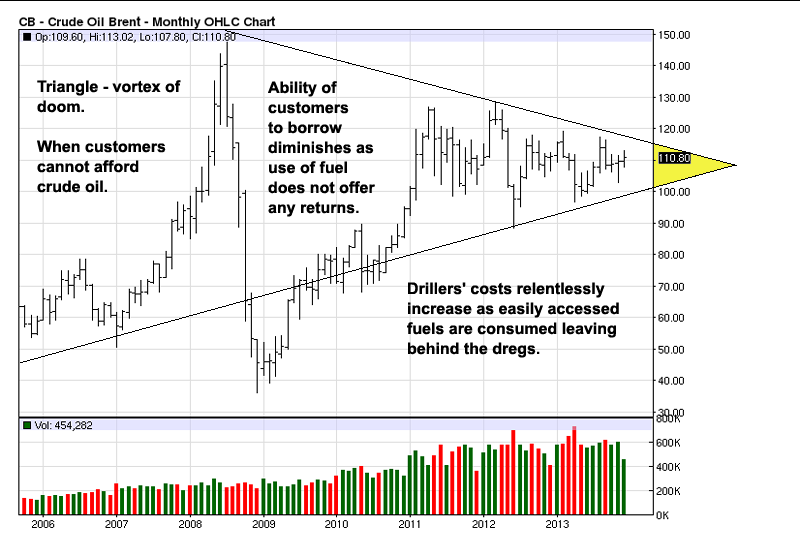

Figure 1: World-famous Triangle d’Doom: (CommodityCharts.com, click on chart for big). The upper bound declines along with generalized creditworthiness. The cost of fuel production increases due to geology and the increased difficulty in gaining fuel to replace that which we have wasted. $115/barrel has become the new $147; see what happens when the Brent price nears that level: the economies of India, Thailand, Brazil and Turkey begin to vomit.

What constitutes an oil shock is being redefined downward. At some point the price that sweeps economies into the pit will be too low to bring new oil-like substances to the marketplace. We are rapidly approaching the unhappy date when this occurs, at the end of this year or soon afterward … This is if nothing else goes wrong and the various managers make no errors. Keep in mind, any shortages that occur because fuel is unaffordable … will be permanent. Having the fuel supply constrained will not make countries richer; constraints will obviously not make more fuel supplies available.

The vulnerable developing economies face severe difficulties as the combined costs of fuel and credit have become breaking, (Bloomberg).

Energy Commodity Futures

| Commodity | Units | Price | Change | % Change | Contract |

|---|---|---|---|---|---|

| Crude Oil (WTI) | USD/bbl. | 95.49 | -2.93 | -2.98% | Feb 14 |

| Crude Oil (Brent) | USD/bbl. | 107.78 | -3.02 | -2.73% | Feb 14 |

| RBOB Gasoline | USd/gal. | 269.92 | -8.67 | -3.11% | Feb 14 |

| NYMEX Natural Gas | USD/MMBtu | 4.31 | +0.08 | +1.80% | Feb 14 |

| NYMEX Heating Oil | USd/gal. | 298.67 | -7.85 | -2.56% | Feb 14 |

Precious and Industrial Metals

| Commodity | Units | Price | Change | % Change | Contract |

|---|---|---|---|---|---|

| COMEX Gold | USD/t oz. | 1,224.60 | +22.30 | +1.85% | Feb 14 |

| Gold Spot | USD/t oz. | 1,225.37 | +8.53 | +0.70% | N/A |

| COMEX Silver | USD/t oz. | 20.01 | +0.64 | +3.30% | Mar 14 |

| COMEX Copper | USd/lb. | 338.65 | -1.00 | -0.29% | Mar 14 |

| Platinum Spot | USD/t oz. | 1,400.00 | +32.55 | +2.38% | N/A |

After the shock the prices decline as credit is adversely effected. High prices are their own cure as the less capable purchasers are excluded from the market. This is the consequence of competition for the marginal funds between fuel users and energy suppliers. The drillers’ victory is the ruin of everyone else, ultimately the drillers as well.

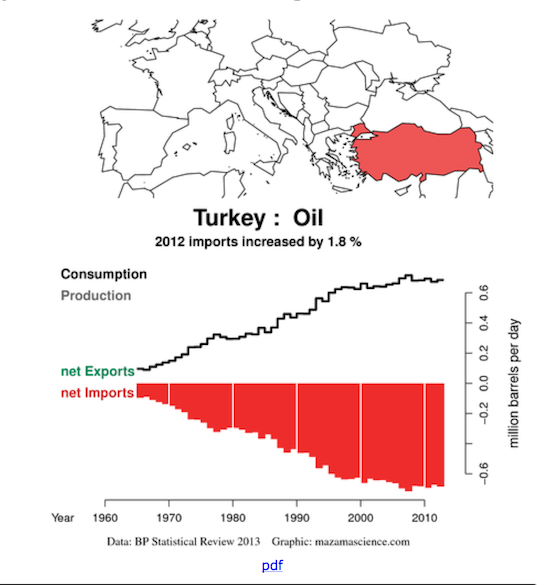

What happens when the credit dried up can be seen in Turkey. Countries must import credit in one form or another, either as investment ‘capital’ by way of carry trades or returns from export sales. The credit is then spent on petroleum. A country with its own oil supplies can pay with its own credit but imports must be paid for with some form of freely-exchangeable currency such as dollars … these can be gained on foreign exchange markets but not always easily at all times. The tether to forex markets and the need for small European countries to ‘buy’ dollars or sterling at a sharp discount before buying fuel was an impetus for creating the ‘euro’; it became the native currency of small countries such as Netherlands and Portugal.

Figure 2: Energy maps from Mazama Science: Turkey;s energy profile looks just like its neighbor, Greece. It has almost nothing in the way of native fuel supplies, the country must borrow to finance needed fuel imports. It has been able to do so with short term dollar- and euro loans which have recently become increasingly costly. The reason of course, is the absence of return on the ‘use’ of the fuel in Turkey and elsewhere. Retiring loans requires continual rounds of replacement loans. These new loans have become difficult to gain.

Turkey’s rush to modernize meant the flooding of the country with tens of millions of useless, energy-sucking cars as well as the associated infrastructure. All these things require credit to obtain, so does the fuel needed to run everything. As with the hapless PIIGS, there is little the Turks have to offer in exchange for their imports other than the need for more borrowing tomorrow, thereby providing origination fees to financiers. Credit is constrained, there is a contest for loans, the bankers look elsewhere and Turkey is stranded along with its still-born modernity.

As is often the case, the country has seen violence in the streets as the promised prosperity is deferred. Turkish unemployment — particularly for youths — is very high with no end in sight. Higher education is a claim against the future, as can be seen around the Mediterranean, in the US, Japan and elsewhere … youth unemployment indicates there is no future. The current national government is under severe pressure; as with the European- and other energy deadbeats, the next step is replacement with a technocrat regime aligned with one giant New York City bank or another and the slide into irrelevance and ruin.

With interest rates set to rise in America and Europe, credit flees away from Turkey which is now deemed to be ‘risky’. The outcome is ‘conservation by other means’; look for Turkey’s energy consumption to decline as credit evaporates and the economy crumbles.

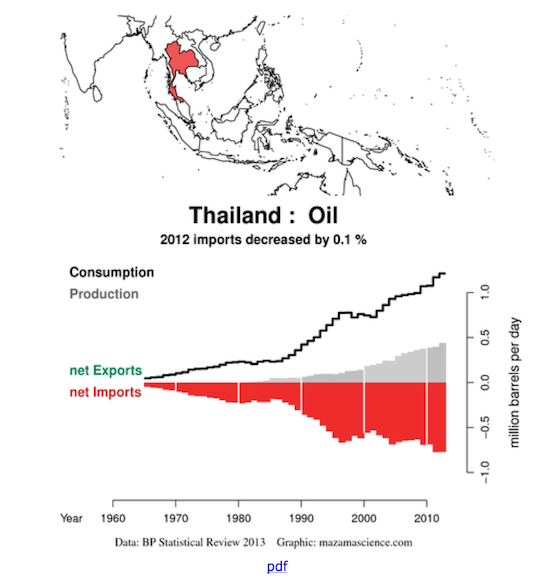

Figure 3: Thailand’s energy import imbalance; its runaway energy consumption is funded with short-term dollar loans gained by way of the interest rate differential and the dollar carry trade. All of this falls apart with increases in debt and rising interest rates.

As with the Greeks, the Thais believed that progress is mechanical fetishes as seen on TV. Western industry was more than eager to provide these items at a price; finance was eager to provide financing. The outcome is a Thailand filled with millions of cars that cannot offer a return for the hapless users. Cheap Thai labor toiling in sweatshops cannot fill the gap; provide the return needed to offset the cost of non-productive progress.

What keeps Thailand from total collapse is the country’s organic fuel supply that is being depleted as rapidly as possible. Once the fuel is gone, so will Thailand’s American-style ‘way of life’. Meanwhile, the Thai government is under severe strain as the progress-inflamed citizenry demands more of it … or else!

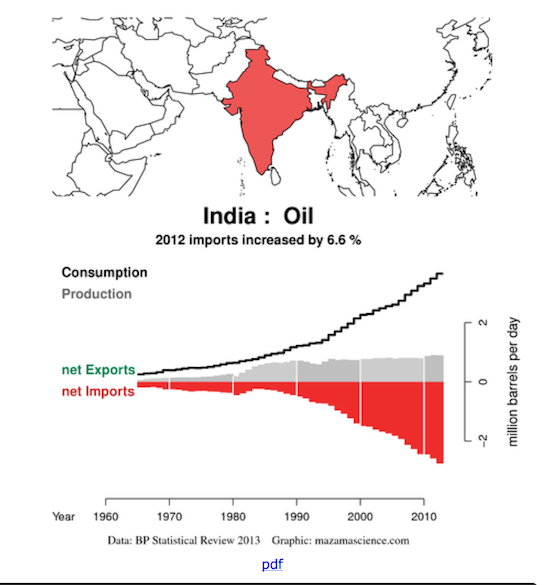

Figure 4: India’s fuel budget looks little different from the others: hopeless. India grows its human population along with its population of fuel-greedy cars … without restraint. The country’s galloping fuel consumption is paid for with funds flowing from its overseas’ trading partners. As long as interest rates remain low, funds flow toward India which has used these flows to finance its imports, both fuel and bullion. Now, credit is a problem: the tide of overseas funds has reversed leaving the rupee to fall sharply in price. This has led the Indians to import gold and abandon the rupee; the Indian establishment has taken aim at the gold to support its currency. It would make more sense to take aim at the cars and fuel imports, instead.

India is less vulnerable than Turkey to an outright energy shortage due to its modest domestic petroleum reserves, yet the country shows no sign of any effort other than that to exhaust its own fuel supply as rapidly as possible. In the war between India and its own automobile fleet, India is losing.

Figure 5: Different continent, same sad story. Ironically, analysts hold out the hope that Brazil will become a major oil producer and propel economic expansions in other countries. What it looks like is that Brazil’s production has peaked and will enter terminal decline … with deep-water offshore production barely able to keep pace with depletion elsewhere in Brazil. Meanwhile, consumption is galloping ahead as the country ‘modernizes’: not only is Brazil a major importer of automobiles but also a manufacturer. Nobody seems to recognize that motor vehicles are the core economic problem, that there is no return for their use except as buses and taxis, agricultural tractors, delivery trucks and construction equipment; that fuel demand is unproductive waste.

Both India and Brazil attract capital flows with relatively high interest rates. This supports their currencies but increased rates are a form of rationing. At the same time, the higher cost of credit is itself inflationary, to keep this malady from running out of control requires even higher interest rates = tighter rationing. The countries wind up in an interest rate trap.

The expectation is that very high fuel prices will ration consumption and that prices will increase to the point where this takes place: $150 – $200/barrel. The question never examined is how consumers are expected to come up with the needed credit to meet these very high prices.

– If prices are the means of rationing then prices must decline when the rationing process becomes effective. Otherwise, the prices must continue to rise! However, because a price decline occurs does not mean that the new price is affordable. The same forces that made the highest price unaffordable are still in effect rendering the not-quite-highest price likewise unaffordable. The ability to meet the new price diminishes steadily. This is the ‘cost’ extracted by the rationing process. This cost increases with the passage of time; the fuel price must continue to decline even as it is always ‘unbearably high’.

Even @ $5/barrel, there are some excluded from the markets because that price is unaffordable; what matters is the increase-decrease of this group of potential — excluded — purchasers.

– Generally, the demand for fuel has to be considered infinite; it exists everywhere in the world there is the TV and paper money. With the TV comes the advertising; marketing = demand. It is foolish to assume that demand can be destroyed or that it shrinks of its own accord. Any and all effects on demand are exogenous … just as demand is the creation of marketing, demand is destroyed only when the marketing itself is annihilated as during a war. Under ordinary circumstances demand will persist long after the means to meet it vanishes. Demand lurks in the collective mind of culture like a rat hungering in the hole, waiting for some- or any means to come to hand.

– Consumption of fuel is credit-dependent in every instance. If there is insufficient credit or it is rationed, consumption is diminished. Otherwise, consumption is inflexible. Right now, in the margins of the world, credit is being rationed … as the means to ration fuel.

– Very low interest rates along with asset-price ‘bubbles’, off-shoring jobs and allowing inflows of cheap, immigrant labor, the euro and its accompanying fiscal regime are all energy price hedges, all have failed or are failing. This is because the fuel ‘asset’ is destroyed by way of its use. As has been pointed out previously, with fuel, the road between worthless and worthless is very short: worthless in the ground, worthless as a gas in the atmosphere. This self-annihilating aspect of our way of life is unexamined by other so-called ‘economists’.

– The credit system is breaking down in countries dependent on external capital (credit) flows. Brazil, Thailand and India depend on dollar credit inflows Wall Street. Blame is fixed on the US central bank and ‘tapering’ however, this is only partially true. Central banks cannot create new money only fix- or manipulate the price of certain assets. The central bank cannot oppose- or direct the markets for more than a modest period of time, after all, central banks are simply small parts of the greater lending whole. Because of recession, because of very high and increasing real fuel prices, the demand of credit is diminished, there is deleveraging and a generalized shrinkage of private sector balance sheets (Keen). As the private sector returns to lending and chases asset returns to hedge higher fuel prices, the marginal countries such as Brazil must compete for funds. This competition — not tapering — indicates higher borrowing costs. As has been pointed out here over and over, the cost of credit + the cost of fuel have become unaffordable. In 2014 as has been the case since 1998, the effect of those costs together will be felt more heavily around the world.