The Nobel Prize for Incompetence goes to …

– Barack Obama! That was what that was for!

WASHINGTON — As the health care debate moves to the floor of Congress, most of the serious proposals to fulfill President Obama’s original vow to curb costs have fallen victim to organized interests and parochial politics. And now the last two initiatives with real bite that are still in contention — a scaled-back “Cadillac tax” on high-cost health plans and a nonpartisan Medicare budget-cutting commission — are under furious assault.

Most economists’ favorite idea for slowing the growth of health care spending was ending the income tax exemption for employer-paid health insurance to make lower-cost plans more attractive. But that would hurt workers with big benefit plans, and a labor-union lobbying blitz helped kill that idea by the Fourth of July.

Lobbying by doctors, hospitals and other health care providers, meanwhile, dimmed the prospects of various proposals to cut into their incomes, including allowing government negotiation of Medicare drug prices and creating a government insurer with the muscle to lower fee payments.

“The lobbyists are winning,” said Representative Jim Cooper, a conservative Tennessee Democrat who teaches health policy.

Many Democrats would like to see the government negotiate far lower prices for the Medicare drugs it buys. But drug industry lobbyists say — and the debate on the finance bill appears to confirm — that Mr. Baucus’s agreement to limit the industry’s costs excludes such price negotiations. Now the drug lobbyists are pushing to be sure the Medicare commission could not force negotiations either. The relevant text of the bill is still being written.

Some analysts contend that in other ways the drug industry deal could even encourage unnecessary spending on brand-name drugs. As part of its $80 billion, the industry would provide discounted drugs for certain Medicare patients who had previously been forced to pay for them until their bills reached a certain level. The deal will thus eliminate what had been an incentive to switch to cheaper generics. “It is market protection,” one drug company lobbyist said of the deal, speaking anonymously for fear of alienating the White House.

This is how it goes, the idea is great and it bleeds out in hundreds of secret meetings between legislators and lobbyists. The hand of the leader is nowhere to be seen or felt. The process is a failure, how can the outcome be any different?

The question now is whether the Congress can pass a bill at all. A sham health care bill is touted as superior to the present state of affairs but the discount is for the likelihood of the situation deteriorating. The current rate of price increases is causing companies to ditch coverage. A higher rate – which would satisfy the business lobbyists – will reach a tipping point where the whole scheme collapses under its own weight.

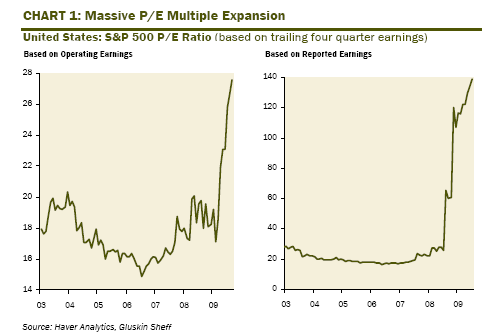

The Nobel Prize for Cupidity goes to those who express belief in a general recovery by buying stocks. I saw these charts by David Rosenberg posted by Mish and I had to laugh out loud:

What flavor Kool aid are these stock market dudes drinking?

Rosenberg (and Mish by extension) don’t think there is anything to this rally- in- a- bear market. The question is what will bring an end to the bull party. Keep in mind that the Quantity Theory of Money added to Fractional Reserve Lending gives an expansion of available funds which drives more lending in a virtuous cycle.

The stock market is generating its own liquidity! It’s not ‘pump and dump’, it’s ‘Pump and Pump Some More!’ The stocks being bought/sold are derivatives; the companies these derivative themselves represent need only to remain discreetly irrelevant. They must evade out- and- out bankruptcy. The companies are outliers, ‘underlying’; their lack of performance matters little to a system that exists only to generate more and more liquidity. The market is measuring not the values represented by ‘earnings’ but rather the ability of the market to lend more and more funds into petit circulation.

It does this rather well, no?

The Nobel Prize for Liquidity goes to Goldman- Sachs and the New York Stock Exchange.

What really will end the current rally? Good question? Rosenberg really doesn’t say. Most focus lies on the banks, with Michael Panzner remarking:

Whether you call it a reality check… a wake-up call.. .or a splash of cold water reality,…

…based on the following MarketWatch report, “October Surprise from Bank Earnings?” it appears that lots of people are going to be caught out when banks announce their earnings in the weeks and months ahead …

Some experts worry results may be much more negative than investors expect

Bank stocks surged during the third quarter, but as companies prepare to report results from the period, several industry experts remain concerned.

“We are very early on in this credit cycle,” Timothy Long, chief national bank examiner at the Office of the Comptroller of the Currency, said at a recent conference.

“That statement caught everyone by surprise,” said Nancy Bush, a veteran bank analyst who attended the conference.

Keep in mind, there are two separate and unequal economies, both in the USA and elsewhere. The physical economy is tethered to energy supply, particularly crude oil. As crude oil availability shrinks, the productive economy will shrink along with it. While a crash here cannot be ruled out, an erosion along what has taken place since 2000 is more like it.

Meanwhile, the accumulation of risk that accompanies the expansion of finance’s ‘balance sheet’ is truly breathtaking. The amounts outstanding in credit/interest rate and other swaps totals over $500 trillion dollars!

The bulk of these include interest rate swaps to hedge interest rate volatility; with much of the world’s interest held near zero there is little volatility to hedge. What remains is a(nother) means to bloat some balance sheets and amplify risk. The rapid expansion of debt is reaching a point where ZIRP policy must be fixed indefinitely: the cost of servicing the ballooning debt at yields which would historically be considered ‘normal’ would be impossible to bear.

With the stock and other markets engaged not so much as reflecting ‘real world’ values but rather creating much more debt, can an interest rate demand be what pulls the plug on this rally?

Of course, the reason to increase rates is to price inflation; what else could the massive expansion of finance’s balance sheet represent other than inflation on a cosmic – or at least solar systemic – scale? Asset prices increase … this is surely a monetary phenomenon! What Rosenberg notes is the disconnect between the physical economy, mired in deflation and unemployment and the stratospheric economy of hyper- inflating ‘investments’. This indeed is what his happening under – or rather – over our noses!

The same dynamic that took place in Weimar in 1923 is taking root in the S&P 500. What is the outcome? Investors could certainly trade extremely inflated collateral across markets to retire bad debt held elsewhere. Trades could be made in the OTC swap markets where the notational amounts of bad debt as well as unfunded future liabilities are trifling.

‘Unfortunately, as was the case in Weimar, the prices driven by expanding debt and liquidity do not and will never will reflect the underlying productivity which these things are supposed to represent. At some point, as was the case with the ‘trillion mark loaf of bread’ what Citi or AIG are supposed to represent is nothing but a crumbly husk.