Since the beginning of the financial crisis in 2007, this question has never been satisfactorily answered. Obviously, both conditions exist – particularly the closer one gets to the monetary and credit regimes – but neither condition dominates. The Great Depression of the 1930’s and the ‘Lost Decade’ in Japan were deflationary. The ‘Double- Dip’ recession of the early 1980’s was inflationary.

The latter was ended by deflationary (high) interest rates, although rapidly declining oil prices also helped end that recession. This decline was largely propelled by new crude supply from the North Sea and Prudhoe Bay.

Central bank created inflation did not end either the Great Depression or the Japanese recession … something to keep in mind. Mobilization for WWII ended the US depression – inflation came later. Bank ‘reform’ – belatedly putting insolvent banks out of their misery and accepting the consequences – ended the Japanese deflation, which also took place within a positive balance of trade context and a largely expanding world economy.

Inflationists point to large trade and fiscal/current account deficits and structural borrowing imbalances with China and to a lesser degree Japan. These analysts also point to increasing carry trades which now include the US dollar v. high yield currencies such as NZ and Australian dollars. They point to ‘expansion’ in China and the lessening of crises in Europe, Russia and latin America.

Inflation bulls point to hedging strategies such as rising Treasury rates, rising gold and commodity prices and the large overhang of Fed/Treasury liquidity which suggests ever- more dollars will start chasing fewer goods into the indeterminate future. This then suggests the possibility of accelerating downstream credit creation.

With oil prices heading solidly toward $75 a barrel, and the 10 year in a year long bear market – with the dollar getting thrashed in consequence – the inflation case seems pretty convincing. Traders believe the US government is willing to sacrifice the dollar in order to save the growth potential of the status quo:

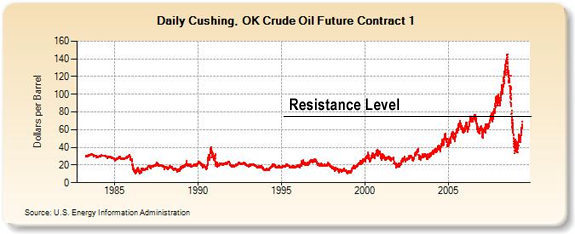

The EIA price (Cushing, WTI) is nearly at the level reached by the long- term surge from 1998 to 2007. If the price level of approximately $78 is breached there are technical reasons for the price to re- test last years $145 high.

Chart by Stockchart.com

This chart indicates the long- term decline in price for 10 year Treasuries. This decline in price would suggest inflation. Added to the increase in crude price and the ripple effect taken out of context is clearly part of an inflationary spiral. The government’s- and Fed’s strategy to monetize housing prices and sovereign debt are succeeding. One only has to read the New York Times, Wall Street Journal, listen to CNBC and other mainstream media outlets. The issue of the day is the need for the Fed to consider how best to combat this inflation before it accelerates out of control.

None of this is convincing. Without an increase in wages or some mechanism to put ‘liquidity’ into the hands of the general public, the rise in credit costs and energy are not inflationary but instead sharply deflationary. The increase in 10yr yields has effectively put the mortgage re-fi industry on hold. While a housing ‘recovery’ isn’t completely off the table, the increase in mortgage costs pushes any recovery farther into the future. Unsecured personal credit is also disappearing. Finance companies are steering away from lending to individuals. Credit reform measures are shifting risk costs to banks away from borrowers, who cannot afford more risk at any price.

Continuing decliines in housing prices have closed the home- loan ATM. Foreclosures are increasing and more homeowners with means are losing their investments. None of this is inflationary.

Banks are hoarding reserves. Customers aren’t borrowing and those that are are simply rolling over existing higher rate loans. Increased money costs reduce the refinancing incentives. None of this suggests the ability of business to pass along increased costs to customers, in fact the greater likelihood is for increased costs to increase business bankruptcies.

Regardless of slowing rise in unemployment claims, the overall rate of unemployment continues to increase. The total of hours worked is declining. The un- and underemployed cannot add to the wage- price spiral. Increasing costs of goods and services due to increased credit and energy costs simply shrinks the market for these.

The mechanism driving oil prices is both technical and administrative. The influx of liquidity into the markets has inflated some asset (stocks) and commodities prices. If there was any chance of inflation, the stock markets would be falling and most bond yields increasing even more sharply. At some point along that trend, borrowing would become expensive so that credit would be rationed. Put another way, there is some unknown yield point where what is being priced is not inflation but default. This is dangerous because nobody can say what that yield point is!

Chances are it is a much lower yield than market professionals would consider. The massive overhang of sovereign supply amplifies risks to the downside. The Fed – and the rest of the bond market – could find itself in an uncontrollable feedback loop rapidly amplifying yields.

The price risks of oil – and other commodities – to the general economy are also increased. The price point where oil costs start shutting down the overall economy is unknown although it is probably far lower than oil traders and producers have suggested. The market for crude like the market for debt has its own dynamic.

Traders who have arbitraged oil contango have more reason to store crude as that commodity increases in value steadily week by week. The dynamic of contango feeding off itself is becoming stronger than the inventory overhang fundamental that the contango simultaneously represents. This mechanism and the flood of ‘hot money’ into commodities markets – and away from Treasury markets – has decoupled inventory from ordinary pricing constraints. Since 1999, the balance in the crude market has swung away from the consumer toward the producer. Sellers have gained the ability to set prices against the ability of purchasers to bargain. This overall fundamental is not to be changed without large, new supplies coming onto the market.

There is the probability of profit taking along the way but the only thing I can see bringing this current market down is another deflationary break as was the case late last summer.

When that happens all the (happy??) talk of inflation will disappear. Liquidity will vanish into the equity, CRE and commodities markets black holes and we all – the Treasury, Fed and other speculators – will be the poorer.