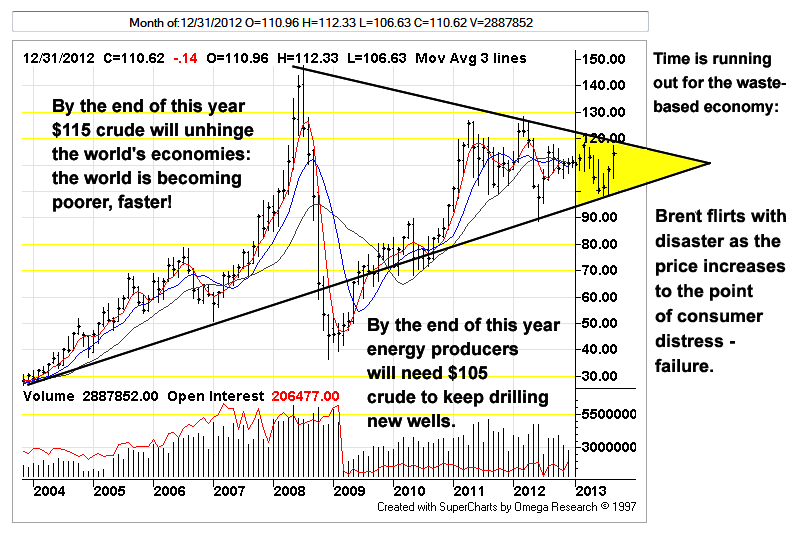

Figure 1: The Triangle of Doom, closing in on countries near you! The frenzy over a possible US-led attack on Syria resulting in a wider war has pushed Brent bidding to $119 per barrel the same way the possibility of a US- Israeli attack on Iran drove prices to $128 in 2012. A price much over $120 per barrel for more than the shortest period would cause a gigantic economic spasm the same way $147 per barrel undid the world in 2008.

For this reason, there is diminishing likelihood of a US or NATO attack on Syria, only saber-rattling to keep the crude price from plunging below cost of production. The consuming world cannot afford to attack Syria, it cannot afford the risk of a wider conflict, it cannot afford for the Saudis and Iranians to launch missiles at each others’ tankers, pipelines, fuel terminals and desalinization plants. As with everything else in this not-quite-so-green Earth, there are diminished returns to war.

At the same time, the world cannot afford sub-$100 crude as the real cost of production creeps relentlessly higher. Easily accessed light crudes are being exhausted leaving only hard to find, poorer quality replacements: when the price declines, there are no waiting reserves of low-cost fuels to be put back into service, only shortages.

Since 2008, the highest tolerable price has declined steadily as the system of interlocking banks and debt-money unravels. Credit diminishes and countries struggle to import both goods and crude oil … as is the case now in Europe and in South Asia. The process is self-reinforcing: when a country cannot borrow it is unable to retire maturing debts and is insolvent … because a country is insolvent it cannot borrow.

The establishment strategy has been to force lending and inflate serial bubbles. There are zero percent interest rate policies (ZIRP) by the Federal Reserve and other central banks, the non-stop moral hazard and carry trades. Cheap dollar credit is shipped overseas to become collateral for loans offered in local currencies at a higher rates of interest. The idea is for the borrowing country to hold both the dollars-as-collateral plus the newly issued local currency. This effectively multiplies the countries’ money supply.

Dollar collateral is not currency rather it is loans. Funds are borrowed from the money markets, commercial paper and repo. These loans require constant roll-over, that is new loans obtained to retire amounts due on maturing loans. When roll-over cannot be had or is expensive — or when Americans import fewer manufactured goods — the flow of dollar credit overseas shrinks rapidly, the collateral vanishes. Ditto, when the collateral must be re-exported then swapped for petroleum. Dollar-borrowing countries are obliged stump up more collateral to maintain stable exchange rates — a kind of dollar margin call. As always, the fewer the dollars available, the greater the demand for them, (Ambrose Evans-Pritchard):

India pushes ‘shock and awe’ currency plan to save BRICS“It is going to happen in a matter of days rather than weeks, Brazil and India can start the move,” said Dipak Dasgupta, a top Indian official.

Mr. Dasgputa told Reuters that China, Brazil, India, Turkey, Russia and South Africa have all been squeezed as the US Federal Reserve prepares to tighten monetary policy. Joint action would give emerging markets greater firepower, allowing them to deploy their combined $8.7 trillion (£5.6 trillion) of reserves and crush “speculators”, rather than being picked off one by one.

However, it is unclear whether such action would serve any useful purpose if the real problem is exhaustion of catch-up growth models in these countries, and boom-bust credit cycles. “This could backfire,” said Ian Stannard, of Morgan Stanley. “If they did this, they would have to sell US and European bonds and that would push up yields. It was rising yields that started this process in the first place.”

The side-effect of such intervention would be monetary tightening, pushing countries into deeper trouble. India’s growth fell to 4.4pc in the second quarter, the lowest since the post-Lehman crisis in 2009. This is eroding tax revenues and pushing the budget deficit back over 5pc of GDP, with a ratings downgrade looming.

“We are no doubt faced with important challenges,” said Indian premier Manmohan Singh. The rupee is in freefall, crashing 25pc over the past four months to a record low of 68.84 against the dollar.

All of these are of a piece with the strategy followed in Europe after the euro appeared in 2000. Rates were repressed to favor Germany which resulted in the Mediterranean PIIGS countries being flooded with cheap euro-denominated credit. The outcome is everywhere identical: ‘leveraging up’, asset price inflation, speculation and pyramid schemes that are all dependent upon perpetual ‘hot money’ flows. This is what passes for industrial ‘economy’ when ‘catch up growth’ is exhausted, everyone is surprised when it fails.

Credit expansion adds to petroleum demand while supply remains more-or-less unchanged … as it has since 2005. The PIIGS used cheap credit to buy German cars, consumers in India, China, South Asia and elsewhere have done the same thing. The absence of return from buying and using cars while borrowing to do so has stranded consumers and their countries, leaving them at the edge of the insolvency abyss.

‘Development’ becomes toxic as demand balloons: cars, airplanes, highways, retail malls, office buildings are easier and cheaper to build and deploy than new oil fields are to find then exploit. The increase in car sales is considered to be ‘positive’ but costs multiply, emerging as interest rate increases. Hot money flows — whether euros or dollars — are reduced or reversed, the outcome is inevitable deleveraging and asset price deflation. In Europe, Irish and Spanish real estate were deflated along with state debt instruments. In the developing ‘tigers’ the vulnerable assets are the local currencies.

Fuel is a speculative asset, it can be bid up by cheap credit. Unlike stock- or real estate prices, the high fuel price has a real-world consequence; it forces a user-choice between speculation and gas for the precious cars. Something has to give and that is the carry; when it fails, so does support for inflated asset prices as well as fuel. Brazil, India and Indonesia are the ‘new’ Spain, Greece and Portugal … all are victims of failed carry.

As currencies depreciate, imports become more costly including fuel which must be paid for with increasingly scarce dollars. The outcome is for countries to set aside dollar reserves to pay for fuel. As the fuel is wasted so are the dollars which are eventually exhausted.

Taking place under everyone’s noses is ‘conservation by other means’. Dollars and other hard currencies become the proxy for fuel rather than proxy for fuel waste, they are hoarded as a consequence. Depreciation of local currencies such as the rupee drains citizens’ purchasing power; the outcome is permanent exclusion of vulnerable users from the fuel marketplace. Overseas fuel consumption is exportable: fuel not burned up for nothing in New Delhi, Tokyo or Madrid can be burned up for nothing in Northern Virginia. It is not America seemingly against the world so much as it is America’s car dealers … against the rest of the world.

Besides diminished worth of money, purchasing power is diminished by way of defunct banks, insolvent governments and dysfunctional central banks. The worst case scenario is that everything fails at once with both money and institutions useless and discredited … leaving the citizens to their own devices or with no devices at all.

In India, there is inflation in rupees and deflation in dollars; in Brazil there is inflation in reals, deflation in dollars; in Indonesia, there is inflation in rupiah, deflation in dollars. Despite all the talk of US ‘money printing’ there are few if any dollars to be had. Dollar credit is not the same as dollar currency. It is the ephemeral nature of credit overseas that is at the heart of the currency mess, not dollar persistence.

The Real Versus Fake …

While currency depreciation needs to be understood, scale and finance mechanics — as well as propaganda — obscure the larger perspective. There are the threats of war, there are actual wars underway. In the Middle East there is the titanic struggle between petro-superpowers Saudi Arabia and Iran for regional hegemony including control over Iraqi and eastern Mediterranean hydrocarbon reserves. Sunni Saudia versus Shiite Iran: right now the conflict is being fought with- and between proxies including the United States.

The consumer superpowers US and China have taken sides: the US supports Israel, Saudia, Qatar and their al Qaeda surrogates while the Chinese support Iran, Hamas and Hezbollah. The ‘wild-cards’ are Turkey and Russia, both with ambitions in the eastern Mediterranean as well as the erupting masses in Egypt. The contest is presumed to be over energy but in reality is about rationing demand; it is over cars, to determine who will be able to own and drive one … and who won’t.

The ‘alliance of fuel necessity’ between the US and Saudia is the ‘secret’ reason behind both the Iraq invasion in 2003 and further US military adventures in Egypt, Africa, Yemen, Afghanistan and elsewhere. Saudia is an absolutist regime, a paranoid ‘Nazi-lite’ state that — along with absolutist Israel — has a throttle on US policy by way of the gasoline hose. Saudia is the marginal crude producer to the United States as is Iran for the Chinese. Any hesitation on the part of the consumers’ invites critical scrutiny from the various Saudi- and Iranian autocrats.

… after all, US fuel consumption is exportable, any fuel not wasted in California is available to waste in Beijing … and vice versa.

The Sunni-Shia struggle will likely carry on a few more years — or more centuries with sticks and stones. It will be driven as it has been by ambition, false doctrines and religious prejudice … until the adversaries are bankrupted by their own stupidity as well as that of their dependents. Simple energy conservation on the part of the consumer states would tamp down the conflict; it would preserve in the ground reserves of scarce readily-accessible fuels while liberating fuel dependents from usurious lenders, Conservation would financially constrain the suppliers and render them more peaceable. This alternative is too sensible: the exporters are desperate to exchange their irreplaceable capital for false promises lifted from comic books … to do so in order to ‘win’ an apocalyptic conflict that has lasted over a millennium. At the end of the day there is nothing but the (hard-won) empty bag and universal ruin.

Outside of the Saudi goad … the obligation of the American servant to his master … there is no point to a US missile- or airstrikes against Syria. There is nothing to gain. At best a strike would bounce the rubble, at worst the Syrians would sink an American ship which would severely damage the prestige-and presumed ‘invincibility’ of the military. A strike at the whim of the president without a coalition or support from Congress would be a manifestation of his personal insecurities and weakness of character; like a Macbeth or a murderous barbarian king who orders random subjects be put to death so as to demonstrate to himself and to others that he is indeed king.

Our greatest problem is that we refuse to discuss our problem. We eliminate perspective by scrutinizing the world instant-by-instant, what occupies us is the all-encompassing present. We dare not look deeply into the future or even speak its name … there is the possibility of offending it. Looking forward ten years or even less is too frightening: within the scope of our willful blindness the future sets up shop right under our noses, a trap we cannot avoid:

Unknown photographer, the slum as the apotheosis of industrial modernity, comparative advantage at work, (Lebbeus Woods). What grows within the modern, industrial economy is costs. Trade between nations includes export of poverty from the developed world to the rest; poverty is an ‘opportunity cost’, best borne by ‘others’ such as those in this stupendous slum outside of Mumbai.

The larger conflict is between people and their toys; humans versus cars. We absolutely refuse to look at the world this way. We love our toys and give them human attributes, artificial virtues that they cannot as machines possibly possess. The toys silently ask, “How much do you love us?” They demand that we prove it. The costs are metastasizing; eventually the entire world becomes a gigantic slum visited with savage conflicts and unimaginable disasters … with the inhabitants having no idea why …

Even if the human species could adapt itself to endure such an outcome, who would choose to do so? For how long? To what end?

Since 2008 there has been crisis; deleveraging, bank bailouts, bankruptcies, food shortages, currency collapses and hyper-inflation, mass unemployment, negative growth, spreading wars, insurrections, piracy and failed governments … the slum-ification of the world. We pretend that all of these events are nothing more than disconnected episodes; a run of ‘bad luck’ that will soon pass. We expect recovery, our economists and policy makers insist upon it, they pray for it in quiet moments when they believe nobody is watching. ‘Recovery’ is what progress offers to us as our evolutionary prerogative along with endless growth.

Sadly for us, our onrushing events represent a change in conditions, not episodes. All of them are the aggregated costs of industrialization. Pushed into the distant future by way of finance credit and fossil-energy availability starting in the 18th century … the future has arrived … with more (abysmal) futures certain to come. We enter a world of ‘less’. Less does nothing, it simply is: we’re not used to less. Nevertheless, we either deal with it somehow or it deals with us.

In place of the recognition that we must adapt and do so quickly we borrow from Hollywood and television producers pleasing fairy tales offering ‘more’. If one fantasy does not satisfy us we try another. In the mega-slum we confront our inescapable destiny: what John Michael Greer calls the ‘salvage society’ far beyond what he can imagine … here and now … coming to countries near you.