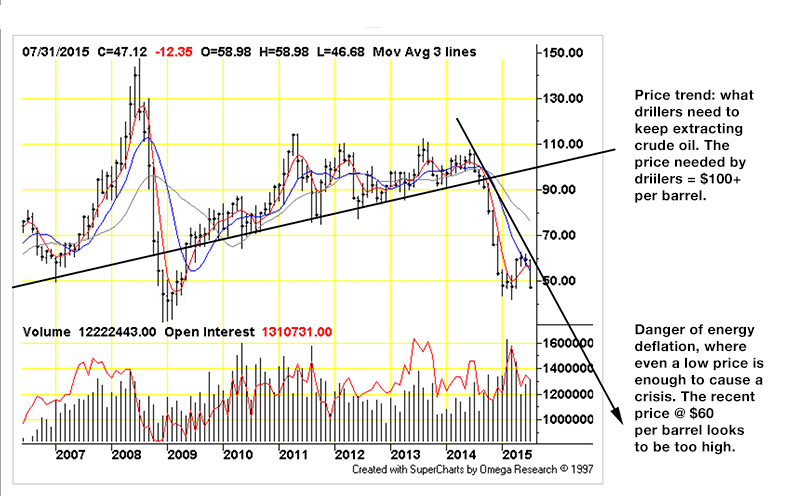

Figure 1: the not-quite-triangle of not-yet doom: World is slipping relentlessly toward energy deflation. Chart by TFC Charts, (click on for big).

Since last summer oil prices have crashed 50% (in dollars). The media fairy tale suggests an output contest between Saudi Arabia and US oil drillers with the resulting glut overwhelming demand. This is yet another reprise of the modern myth of plenty and prosperity, eternally bountiful supply enabling bottomless demand in a consumption paradise. Indeed, demand exists everywhere there is a TV set and paper money; it is the ability to exercise demand that is slipping away.

The Undertow story is of an unacknowledged energy shortage leading to exclusion of less-solvent customers from petroleum markets world-wide. Instead of odd-even days or gas lines, fuel is rationed by way of access to credit. As the fuel shortage propagates, the number of solvent customers declines. This is natural and should not need explanation: oil prices fall because customers are broke. There is the illusion of excess supply because the number of solvent customers falls faster than extraction rates. Attempts by drillers to lift more petroleum exaggerates the illusion of excess supply; prices fall which strangles drillers in a vicious cycle.

Low prices are unable to stimulate consumption, instead, they illuminate the failure of consumption to earn anything … that the economy itself is bankrupt-by-design rather than mismanaged.

The absence of real earnings means all returns must be borrowed. Debt is expensive, the costs are added to those of extracting- and distributing fuel. The marginal consumer is excluded from fuel markets because he cannot afford to borrow or the lender rations credit for solvency reasons. The outcome is a margin call across the economy leading to bankruptcies that ration credit further. Ultimately, credit becomes unavailable and fuel is allocated to those who can earn an actual return on its use … provided there are any real returns to be had. If the returns are not sufficient to support energy extraction there is no energy. This is the outcome of energy deflation, why every effort must be made to keep from slipping into it.

Just as leverage amplifies itself in a virtuous cycle during the expansion period, leverage works violently ‘the other way’ as credit contracts. Self-amplification of customer insolvency is the point of no-return. When low prices strangle- rather than enable consumption, there is no way to reverse the process. If relative solvency cannot enable output then neither will insolvency. If governments cannot enable output by way of subsidies during a period of credit expansion they certainly cannot do so when credit is contracting. Governments must borrow the subsidies they offer to drillers, in doing so they ultimately borrow from the same customers who cannot meet the drillers’ costs; as such governments are no more solvent than their bankrupt citizens.

The great post- World War Two buildout of American style suburbs in the US and elsewhere has succeeded in devouring its resource base and replacing it with claims against what (little) resource capital remains. We are certain to fail spectacularly because we have succeeded at our fools’ errand so spectacularly.

When Is the Crash Coming?

The usual finance suspects are queuing up to predict an imminent market crash, aome have been predicting one for twenty years. They don’t want to be seen as missing the Titanic, others have proven to be prescient: Jeremy Grantham, Nouriel Roubini, Professor Steve Keen. Robert Shiller warns investors to beware the ‘New Normal Bubble’; Dean Baker … well, maybe not this time. Martin Armstrong suggests October this year for the big bang (slump). Nicole Foss suggests that the unraveling is already underway as does Economic Undertow. The problem is most economists view the problem as confined to finance and interest rate policy. This misses the point, monetary- and financial adjustments are irrelevant to an outcome that is driven by resource depletion. Finance difficulties are symptoms of the disease not the cause; we are undergoing a self-propelled regime of hard rationing that is taking shape under everyone’s nose.

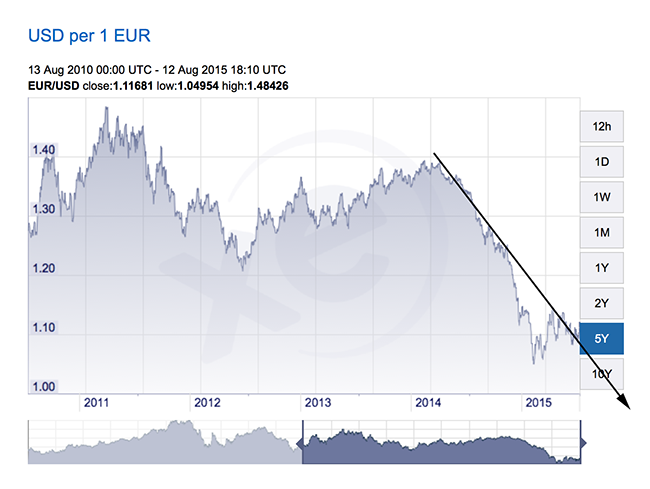

Recent China currency depreciation (vs. dollars) puts more downward pressure on fuel prices even as OPEC drillers Iran and Iraq send more crude to the markets, currency depreciation (vs. dollars) in Japan and Europe reduces the overall bid for crude; demand in countries that supply China such as Brazil are likewise blowing up due to ripple effects and unwinding carry trades.

U.S. stocks fell in early trading on Tuesday in a broad-based retreat as China’s surprise devaluation of the yuan pushed the dollar higher and pressured commodity-related shares.Oil erased most of its gains from Monday following the devaluation by the world’s top energy consumer. Other commodities such as copper, aluminum, nickel and zinc also fell.

Eight of the 10 major S&P sectors were down, with the energy index and the materials index both lower by nearly 2 percent (and more).

Exxon Mobil’s 1.8 percent drop was the biggest drag on the energy index and Freeport-McMoRan’s 12.5 percent slump dragged on the materials index.

Concerns around the health of the second-largest economy in the world also weighed on shares of U.S. automakers and industrials. General Motors was down nearly 3 percent, while Caterpillar was down 2.4 percent.

The yuan fell to its lowest against the dollar in almost three years following what the country’s central bank described as a “one-off depreciation”.

Stock prices are variable, what matters is the price trend (in dollars) relative to the trends of other currencies. Dollar-preference can be seen at work: China needs dollars to import fuel, so do other fuel importers. China also needs dollars to prop up its gargantuan stock- and real estate swindles – slash – Ponzi schemes. To gain dollars it must offer more RMB to foreign exchange holders than it did the day previously. This becomes a sort of dog-chasing-his-tail process where every depreciation gives cause for further depreciations down the road. The name of the game is to trade the ‘Brand X’ currencies including RMB at any price to gain dollars; as these are bought up becoming scarce and more desirable the trade amplifies itself.

With time, the causes that propel depreciation become indistinguishable from effects. China depreciates because of the flight of dollars overseas represents shrinking demand for its own currency. Yet, the depreciation itself is incentive to ditch the currency! Over the span of two days China and everything that it contains is today worth five- percent less than it was, previously. Out of $6.8 trillion in GDP, $340 billion has vanished without a trace, in the blink of an eye: whatever increase the country expected to gain this year is lost by way of its depreciation.

Whatever China seeks to gain by way of cheaper exports is lost due to higher import prices (in dollars):

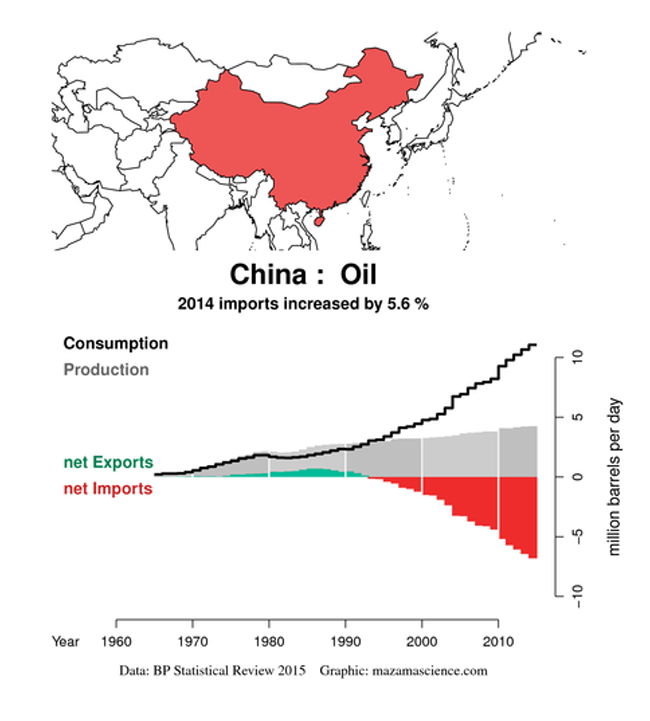

Figure 2: China net petroleum exports by Mazama Science (click for big). The gap between what China extracts domestically and what it must import is financed with borrowed dollars and euros. China turns out to be another energy deadbeat little different from Greece, Argentina or Spain. While China domestic crude output is significant, it cannot keep pace with the country’s galloping consumption.

As China property- and stock markets crash, China aims to dump its deflation onto its trading partners … who are all trying to do the same thing. Like Germany within the eurozone, China has its bunch of captive punching bags to which it can export its misery: Australia, Peru, Myanmar, Brazil, Canada among others. For China’s largest trade partner the US, depreciating RMB is a defacto interest rate increase whether it is considered as such or not. This renders irrelevant whether the Federal Reserve raises policy rates later this fall or not … the result is deflation for the US leading to recession.

Economies are nothing more than fuel wasting enterprises, with the financing edifice erected upon this scaffold. Because fuel itself is hard to hold and store (without a tank farm), ‘money’ is held instead of fuel. With the passage of time, the dollar becomes preferred over other currencies as a fuel carrier. This is because there are plenty of dollars, because Wall Street produces the bulk of the world’s credit; because the US has been the ‘consumer of last resort’, because so many countries export goods or workers to the US that dollars are in wide circulation in these countries … because the dollar is proxy for the American hyper-wasteful lifestyle that almost everyone on Planet Earth aspires to.

Dollar preference turns this last dynamic on its head: instead of being a proxy for waste, the dollar becomes a proxy for what is being wasted. Once that point is reached it becomes a hard currency like the gold-backed dollar of 1932, the same dollar that was hoarded out of circulation causing most of the banks and businesses in the country to fail. The difference was that going ‘off gold’ did not affect how the US consumed energy, going ‘off oil’ would mean just that: switching from a non-functioning industrial economy to a non-industrial version that uses little or no oil at all.

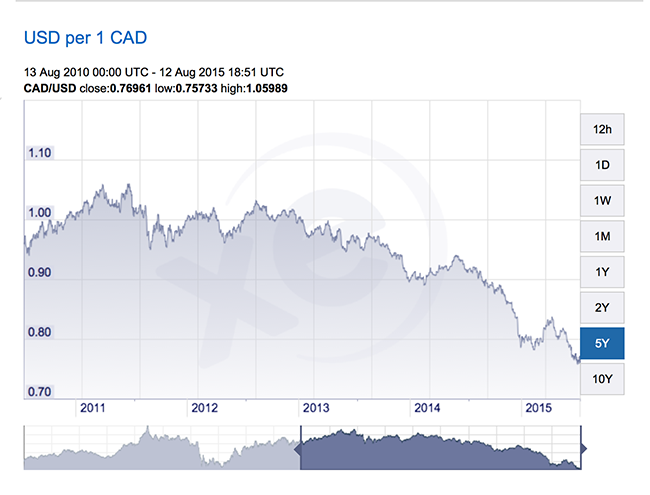

Figure 3: The Canadian loonie (in dollars); Forex charts by XE.com, (click for big). China exports deflation: the loss of crude oil customers in China and elsewhere leaves Canada at the brink of a recession.

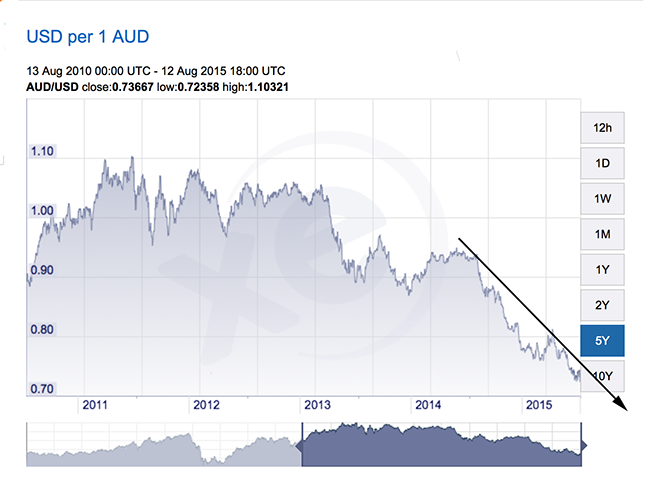

Figure 4: The US dollar — Australian dollar cross; like Canada, Australia bought the ‘it’s different this time’ hype about China resource capital consumption. As it turns out, Australia, like China, is worth a less today than it was over several years of yesterdays. Its reliance on China manufacturing leaves it with assets that have become liabilities.

Figure 5: The US dollar — Brazilian real cross. Sez Bloomberg:

Investors are concerned that the political instability (in Brazil) will push the country into a deeper recession and make it increasingly vulnerable to a sovereign-credit downgrade. The real has depreciated 8.1 percent in the last month, the biggest decline among 16 major currencies tracked by Bloomberg.

Currency depreciation is a dynamic that drives itself. Monetary- and fiscal policy is irrelevant: the worst-case scenario is well- meaning policy blunders amplifying dollar preference unintentionally. As with debt, once on the depreciation treadmill it is almost impossible to get off; this offers a continuum of opportunities for errors, these tend to be self-amplifying as well.

Figure 6: Welcome to Eurolandia, the home of self-propagating policy errors (in dollars). Turns out Germany beating its trading partners to a pulp is not good for business. Who could have guessed? As the fuel buying power of dollars increases, they flow toward the highest bidders, out of Europe, China, Japan and elsewhere toward Wall Street … and offshore tax havens. The outcome is a margin call against leveraged assets. Credit flows are never one- way. After flooding into a country, credit reverses and the funds that are necessary to support leveraged assets are withdrawn. This results in deflation. The same credit rationing underway in Greece is scaled up monumentally in China … with the same outcome!

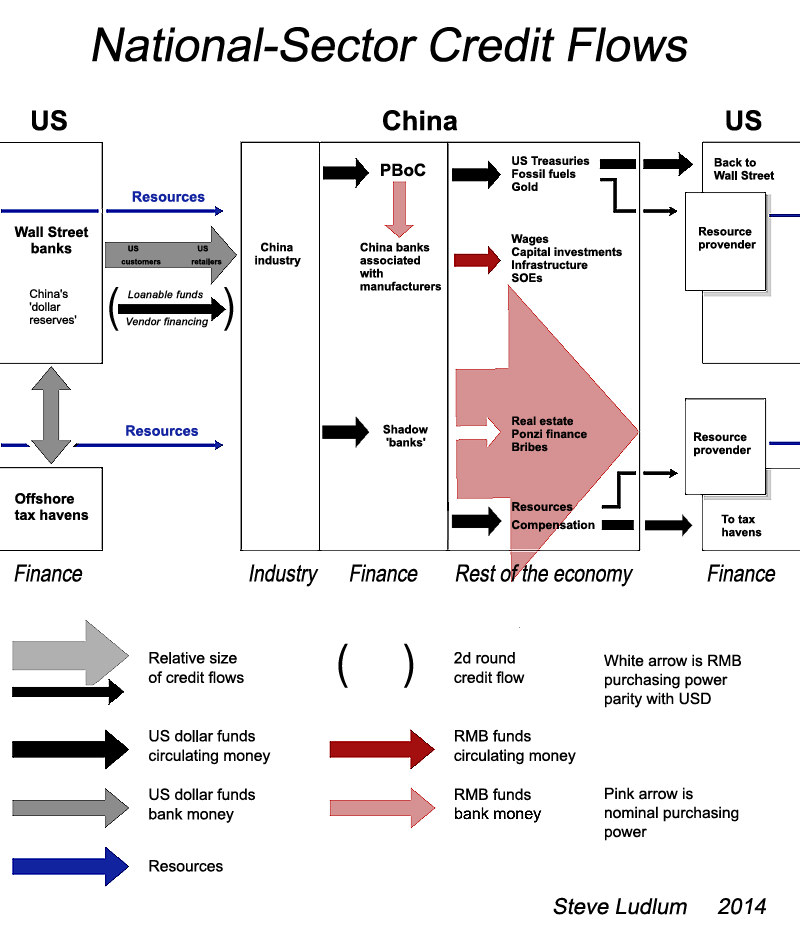

Figure 7: China’s problem takes the form of a giant pink arrow: China’s finance structure is like Argentina’s because China is dependent upon dollar- and other hard currency inflows as collateral for domestic loans. This contradicts conventional analysis which has China as a US creditor. China cannot create dollars or dollar credit; China ‘lends’ energy (coal) and human labor to the US in the form of manufactured goods, these cost the country very little to produce. Repayment is in the form of dollar loans which cost Wall Street almost nothing to produce.

Within China there are two parallel dollar economies. Dollars flow by way of US customers and retailers to Chinese manufacturers. Some are forwarded to the Peoples Bank of China at the official exchange rate where purchasing power is replicated in the form of secured RMB loans into the Chinese economy. The balance are diverted by manufacturers into the loan shark economy where they become quasi-collateral for as many RMB loans as the market will bear. This lending is universally unsecured: when there is no collateral to seize in the place of circulating money, both borrower and lender are ruined.

In China, the shadow banks are very strong, they have distributed losses into the economy a long time ago; these losses have simply not been recognized. Deflation occurs when these losses are finally measured, when inflated Chinese assets are marked to market.

Analysts insist that Chinese dollar reserves can be deployed to bailout its shadow lending business. This is not possible because there is no refunding channel between the central bank and shadow finance. Lenders are simply shells erected to enable the theft of Forex reserves. Any redeployed reserves would be stolen as well. This in turn starves manufacturers of customers who lack vendor credit with which to purchase Chinese goods. Because shadow banks are strong, any unsecured central bank lending would be distributed into the Chinese economy as more unrecognized losses. Attempts to bail out shadow banks precipitates the deflation crisis the Chinese establishment is desperate to avoid: flight of dollar collateral => decline in RMB purchasing power => recognition of losses => bank insolvency and runs out of banks.

Credit cannot expand forever; the ‘Minsky Moment’ occurs when the cost of servicing (unsecured) debt plus the cost of running the actual economy exceeds the cash flow that can be generated by more borrowing.

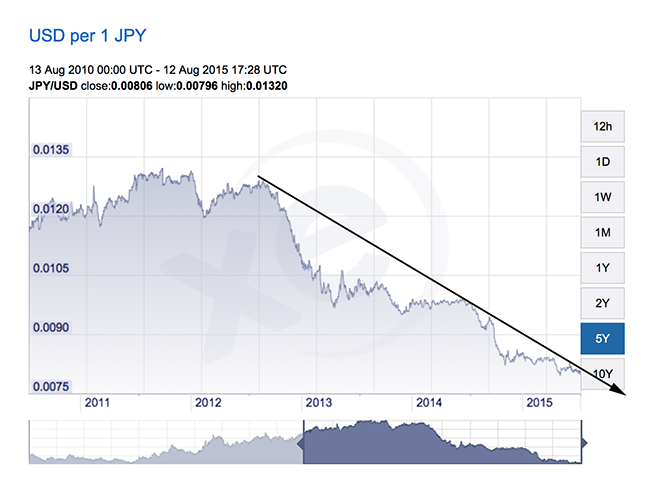

Figure 8: The yen (in dollars). The Japanese government purposefully aimed to depreciate the yen and monetize government spending at the same time. The outcome has been higher import prices and less consumption, “Conservation by Other MeansTM“.

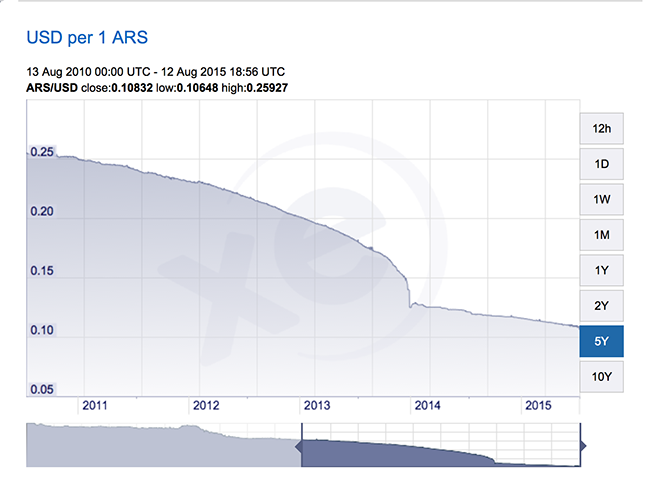

Figure 9: Argentina would rather not depreciate but it has little choice. The country is desperate to develop even as it becomes another economic road kill. Argentina shares with Brazil, Canada and Australia a dependence upon Chinese purchase of commodity goods; as China falters so does the peso. Sadly, Argentina’s plight does not offer it any relief from its overseas creditors …

Figure 10: Even oil producing giants such as Russia are not immune to dollar preference. Like other countries, Russia uses foreign exchange dollars, euros and sterling as collateral for its own lending. As a result, it is in trouble when the Forex starts flowing out of the country; there is nothing supporting the ruble. Russia’s fortunes have not been helped by its sclerotic ruling cadre and military adventures; Russia is only a powerhouse in the history books.

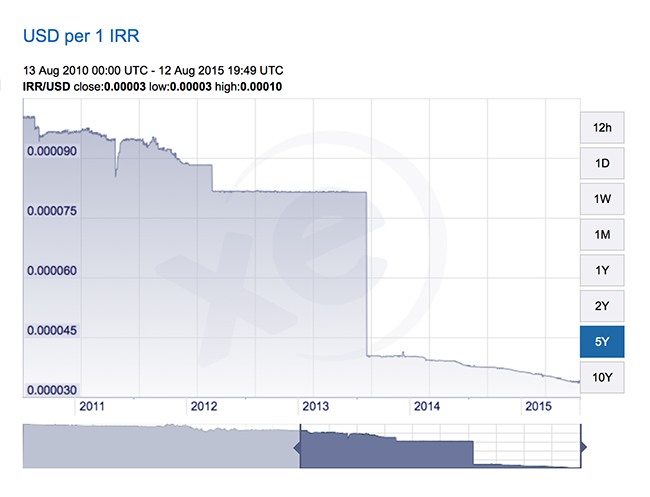

Figure 11: US dollar – Iranian rial. The chart clearly indicates when Western sanctions were applied in 2012 and later in 2013. Iranians were desperate to swap whatever rials they could get their hands on to gain precious dollars. Oil exports do not give any country wealth, instead the wealth is pumped onto ships and sent away to be annihilated somewhere else. Sadly, our economists don’t see things this way, they call the parasitic claims on wealth ‘capital’ and the wealth that is destroyed … ‘inputs’; they whine when the inputs can’t be had cheaply, they whine louder when they are too cheap. Because of economists’ blindness, it is always a surprise when countries like Iran, Russia, Brazil and Mexico find themselves in hot water; economists refer to the ‘Dutch disease’. These countries are hollowing themselves out as fast as they possibly can. What might save some of them is the ruin of their customers; a bit of oil might remain in the ground until some day in the future when someone can figure out what to do with oil besides burn it up for nothing!

Figure 12: Mexican peso (in dollars). Another petroleum exporter facing the hardest of times: the government is incompetent and corrupt, the countryside is overrun with violent bandits, its largest oil field is in terminal decline … the peso is worth less every minute. Checking through other currencies and countries the indicators are much the same. Save for UK sterling and a few others, the world’s currencies are worth much less — over a considerable period of time — relative to the dollar.

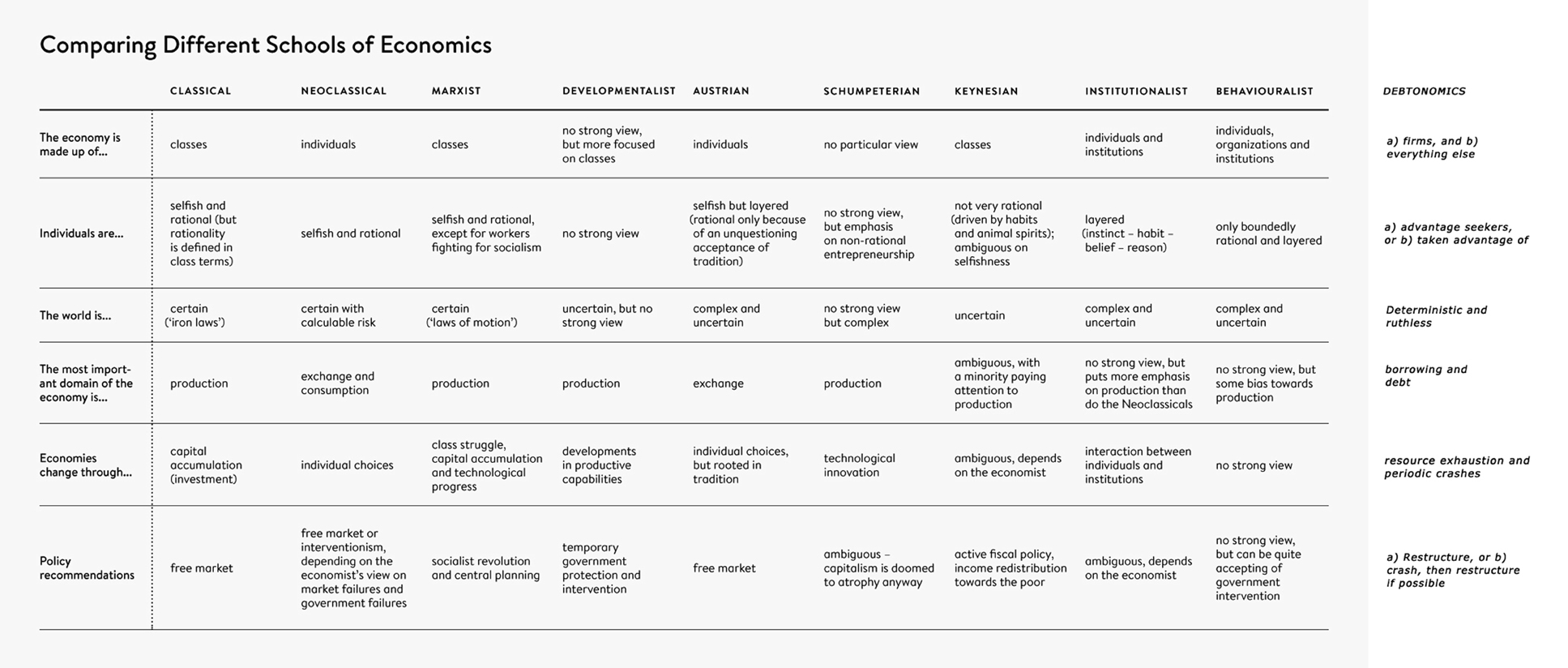

Regarding what can be done, vs. what will be done: consider the role of crashes within debtonomies (click on thumbnail then look to the far right):

Technology and institutions are suggested as change-agents by conventional analysts. Within Debtonomics, the change agent is the process itself. Increasing the capital burn-through rate results in more changes which in turn serve to amplify capital exhaustion. Technology is the instrument of waste, institutions take form to rationalize the use of technology and to provide credit to enable more waste.Crashes are the consequence of resource depletion (Great Finance Crisis) or aggregated surplus-related costs that cannot be shifted. The outcome is that costs rebound against the aggregators themselves; (Great Depression, Long Depression, ongoing Great Finance Crisis). In advance of a crash there is no general incentive to make management changes so as to reduce risks … even as risks compound. Crashes result in mass bankruptcy and obvious changes including public demand for accountability. Crashing is the hardest way to change but seemingly the only way for Debtonomies.

It is hard to say right now whether the depreciation seen worldwide represents dollar preference or something else. It is possible that currency movements are marketplace phenomena that will revert to some sort of mean over time. In any event, the time to take steps to avoid this problem and energy deflation … is slipping away. Obviously, the most important step is to stop wasting resource capital. Because one way or the other, like it or not, capital is going to be conserved.

“A sound banker, alas, is not one who foresees danger and avoids it, but one who, when he is ruined, is ruined in a conventional way along with his fellows, so that no one can really blame him.”

— John Maynard Keynes,

© Copyright Steve Ludlum 2015