As the US stock market reaches new all-time highs day after day after day, people ask, “When is your decline going to start? You promised!”

They are gracious, they leave out the, “you fucking idiot!” part.

When indeed is the ‘Big One’? Prognosticators announce impending catastrophe and it never happens. Prophets of doom are pilloried … the deflationary collapse never takes place. Instead there are the Pollyannas: “The good times are here, forever. You lost! Get over it!”

The overabundance of good times is certainly why every year thousands of ordinary suburbanites are overdosing on heroin: they obviously can’t stand all the winning! It turns out too much of a good (any)thing is toxic; more success and half the people in the country will be shooting Narcan into the other half. Meanwhile, ‘Brand X’ prognosticators are accused of crying wolf too often. Good grief! The wolf-criers are necessary because they create the ‘Wall of Worry’ that all bull markets must climb in order to reach new highs. Here is irony at work: we are murdering ourselves by way of our prosperity at the same time there is nothing we can do- or are willing to try in order to save ourselves from it!

Predicting out the future is … well, you know. The US government spends hundreds of billions of dollars to gather intelligence to predict … just about anything. There are a thousand different bureaus, agencies, organizations, one-man shops, Silicon Valley startups; also satellites, spy ships, aircraft, torture chambers, radio- and Internet intercepts: there are snoops, informants, analysts; the world is crawling with spies. None of above were aware the Soviet Union was about to come undone, they were unaware even as the collapse was taking place! None of these agencies foresaw the ‘Arab Spring’. They were caught with their pants down by every one of the various oil crises even as these were telegraphed by conditions on the ground well in advance. Analysts missed the fracking ‘revolution’, a forty-year old technology by the time it was finally deployed. Analysts missed the massive post-80s industrial revolution in China; they skipped school prior to the rise of #ISIS even though they had a hand in its creation. The analysts, bosses, money managers and central bankers missed one finance crisis after the other, they also didn’t recognize the tsunamis of excess credit that preceded each and every one of them. The word we look for here is ‘hard’. If it was easy to see into the future, everyone would do it and future would never happen, it would be predictable, like the past. Nothing would ever change. Predictability, permanence and stability … In a sense, the inability to predict serves our immediate interests. Predictability suggests ‘civilization’. We don’t want that.

We also don’t want a crash, that includes everybody in- and out of finance. Everybody wants to keep their jobs or get better ones, they want to keep their yachts and private jets, bonuses and stock options: we all have bills to pay. Even a modest decline in asset prices would mean collateral damage, (the) over-leveraged banks would be rendered insolvent. A 1931-style banking crisis would be devastatingly worse; managers are determined to do whatever it takes to prevent one. They’ve had almost ten years of practice as well as vast resources that can be brought to bear: key men are propped everywhere, there are bailouts. Moral hazard is infinite, real interest rates are negative. Banks effectively pay their largest clients to borrow — businesses, governments and tycoons. The statisticians lie, the media lies, economists are clueless and then they lie. Companies use cheap money to repurchase their own shares = these are Ponzi schemes. Manufacturers stuff inventory channels. Loans are extended to any- and all life forms that can draw breath. Because wars are good for business there are wars. Because depredation of nature is good for business our world and everything in it is … degraded. Because the economy is built around endless business expansion, there it is. If real expansion isn’t possible because of natural resource constraints, there is the fake expansion. We have become extraordinarily good at kicking the can, at keeping up appearances. This is why there is no crash today … we’ll worry about tomorrow when it comes. We predict the static condition of endless growth and by doing so we create it. The outcome is the bizarre, twilight ‘anti-civilization’- overly medicated world we have stuck ourselves with because we have given ourselves no other choice.

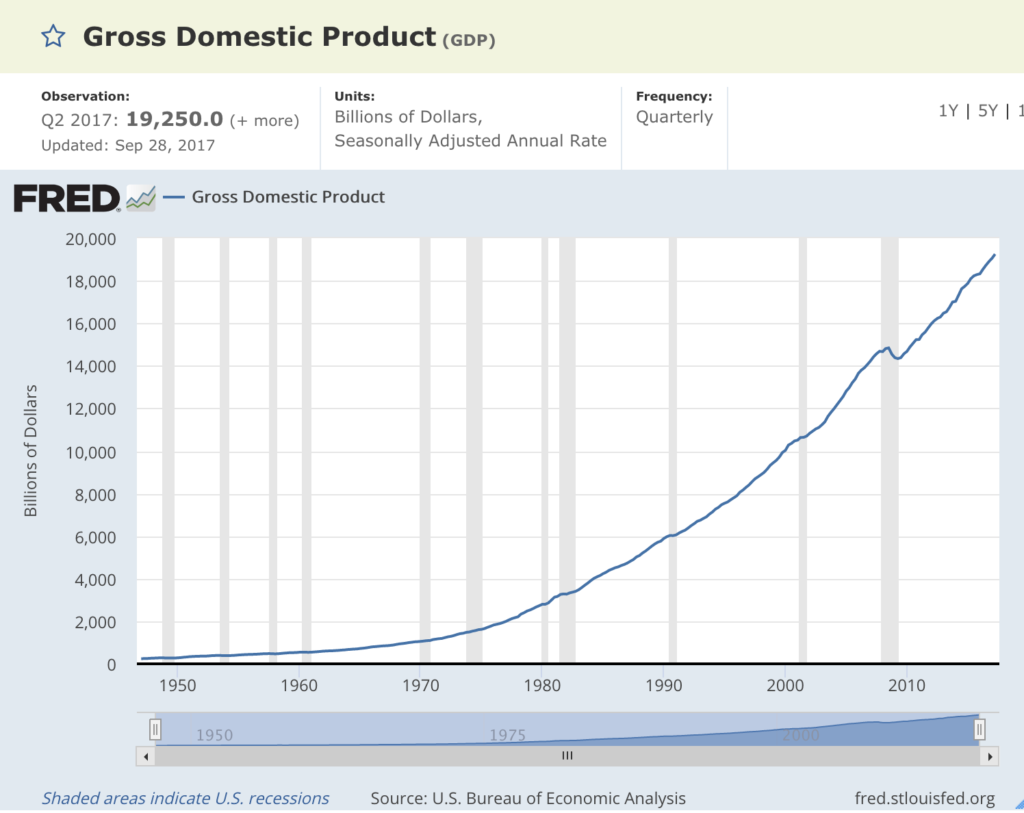

Figure 1: US GDP since the end of World War Two (Chart by Fred, click for big): Just as nobody correctly predicted collapse, nobody predicted our prosperity! Who in 1950 could have possibly guessed?

Looking at this chart it would be safe to predict national income would continue going forward as it has in the past. Yet, for most of human history the line was flat or changed very slightly, tracking the rise- and fall of human population. It summed up what resources (capital) could be accessed with muscle- and animal power, plus water, wind and firewood. As it is, everything below the blue line represents the total natural capital converted into waste by industrial America over the past 80 years = the ‘liability’ side of the GDP balance sheet. This is capital that can never be accessed a second time. The implication is there is are limits and that they are closer than they were 80 years ago. What the chart cannot indicate is how much capital remains accessible or how long it might take to exhaust it. As such, national income is an inadequate forecasting tool.

During the 82-year period on this chart there have been eleven recessions, added together these amounted to a total of 35 quarters, eight-and-a-half years of downturns. This means the US economy experiences declining growth about ten percent of the time with incidences being for the most part relatively brief, less than a year. Past performance suggests the next eighty year period will be similar with the economy being in recession about ten percent of the time. This isn’t set in stone: countries such as Australia and Netherlands have been able to avoid recessions for long periods; 25 years and more. An argument can be made that no obvious reasons exist why the US cannot do the same.

American recessions have tended to follow the credit cycle; periods of expansion followed by inventory buildup then fire sales. Credit is expanding now but this only feeds the illusions, (Andy Xie):

The mistaken stimulus (bank lending) has the unintended consequences of dissipating real wealth and increasing inequality. American household net worth is at an all-time high of five times GDP, significantly higher than the bubble peaks of 4.1 times in 2000 and 4.7 in 2007, and far higher than the historical norm of three times GDP. On the other hand, US capital formation has stagnated for decades. The outlandish paper wealth is just the same asset at ever higher prices.

Banks simply trade each others’ securities back and forth using self-generated credit, all the while pretending the process means something. As long as the banks can preserve the illusion of solvency the process can run on indefinitely: Dow 45,000,000.

Maybe not: the end comes when debt service costs consume total borrowing capacity; a ‘Minsky Moment’; what occurred in Argentina and Greece and is underway in Venezuela.

The end comes when finance players are perceived as insolvent in the way of Walter Bagehot:

“Every banker knows that if he has to prove that he is worthy of credit, however good may be his arguments, in fact his credit is gone … “

“Every banker knows that if he has to prove that he is worthy of credit, however good may be his arguments, in fact his credit is gone … “

This is what happened to Lehman Brothers in 2008: they were considered insolvent despite the protestations and proofs offered by the company, they could neither borrow nor lend, their credit was gone. And because Lehman was in most ways ‘like’ all the other money-center banks, it’s failure reflected on the others, their credit was gone as well.

The outcome was a bailout by the government and Federal Reserve: funds were handed over to the banks no questions asked, funds borrowed from the exact same banks that were bailed out! Outrageous … there was nowhere else the funds could have come from: the $700 billion dollars demanded by Treasury Secretary Hank Paulson in September of 2008, “Now or Never”- plus the tens of trillion$ offered afterward by Bernanke! Both government and Fed held their noses and ignored the widespreading rot and criminality. There was grumbling from the public but soon enough they followed the ‘lead’ of their betters, and why not? The alternative was a smashing depression that nobody wanted. Over time, the banks were seen to survive, executive bonuses remained intact: fakery succeeded and perceptions changed. A handful of companies were sacrificed, others nationalized or gobbled up by other firms. Meanwhile, ‘Green Shoots’: the sub-$40 oil prices of 2009 allowed the consumers to jump back into their SUVs and start shopping again, leading everyone to the point, “When is your decline going to start?” When, indeed …

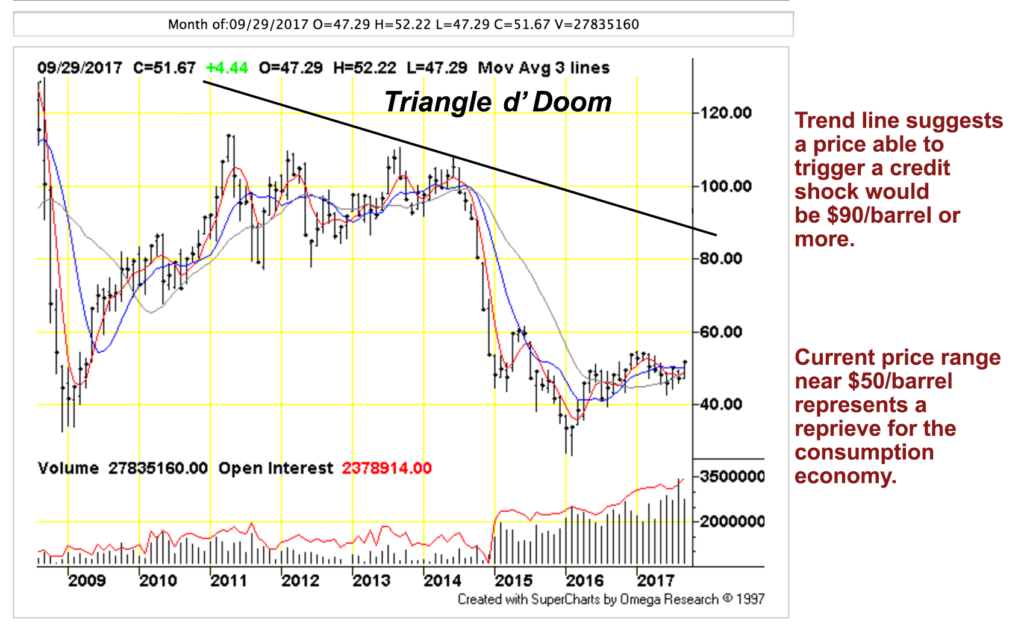

Keep in mind, the Lehman debacle was part of a crisis that only a handful were able to foresee. Here is a proven forecasting tool, the Economic Undertow ‘Triangle of Doom™’:

Figure 2: Triangle d’ Doom, (by TFC Charts, click on for big): The descending trend line suggests the real credit capacity is shrinking. In 2008, the high price was $147 per barrel. By 2014 the triggering price could only reach $115 … there was insufficient credit to allow end users to bid past that price! All else being equal, the price high-enough to cause a credit event this year would be about $90 per barrel. If the price was that high, everyone would be feeling it including traders on Wall Street. The current price range of $40 – $60 per barrel represents a significant discount. It’s high enough to constrains consumption to some degree — by historical standards $50/ is high — but it’s not high enough to walk the system off the plank.

The smallish crash in the energy sector is why we haven’t had the giant crashes everywhere else. Even as low prices hammered drillers and fuel speculators, they saved the rest of the economy and boosted the stock markets! The drillers are further underwater than ever but this does not matter as they were underwater at the higher prices, they simply borrow more. Their job is to keep bankruptcy at bay each day as it comes … while looking for tomorrow to take care of itself.

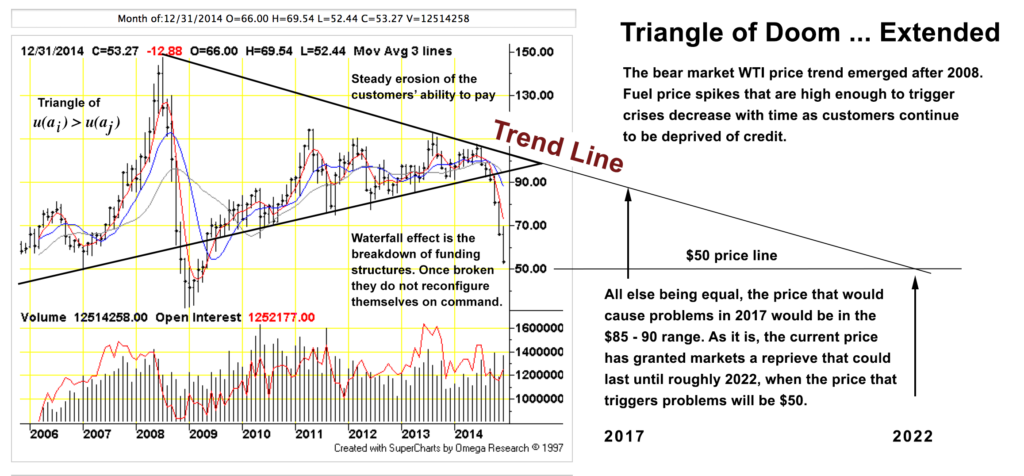

The question next is how long would it take for declining credit sufficiency to cause the current fuel price to be ‘too high’?

Figure 3: The Triangle of Doom Extended (click on for big); this is a better representation of the trend line than Figure 2 which does not include the highest price point in 2008. Extending the line suggests a few more years of ‘cheap-ish’ fuel before even that price is unaffordable and the fuel regime collapses: roughly 2022. It could be a bit farther out or there could be another fuel price collapse. Should the Minsky Moment arrive or a major bank fail, the crisis would occur sooner.

Creditworthiness is an analog for available resource capital. As capital is exhausted, a greater proportion of what remains must be deployed to extract and consume what little remains. At some point this process itself … becomes unaffordable. Even now, end users’ credit access is up for grabs. Moral hazard, low interest costs and current monetary policy shift credit away from customers toward their vendors, tycoons and finance itself. As the customers are ’emptied out’ and fall by the wayside support for those who depend on them and their flow of credit evaporates: over the longer term, tricks used to keep up appearances cannot substitute for top line revenues and actual solvency.

… and It’s called ‘progress’.

In the ‘old days’ civilizations were local. One could fail ‘over here’ even as others survived ‘around the corner’. Our industrial waste-based economy is global; universality brings all resources including crude oil within our grasp. Regardless of the markets, resource exhaustion is ongoing, this is the background story: it must be paid attention to. Everything else we do is part of the fooling ourselves process.

The goods offered by now-obsolete civilizations were permanence and stability. These are not really goods at all but rather moral virtues representing the ascendance of human ambition to an idiosyncratic upper limit of physical and mental development. Periods of high civilizations were considered to be ‘golden ages’ and for good reason. The narrative was one of humans emerging from animalistic savagery and barbarism, evolving to the point of imagining themselves possessed of the characteristics of gods. Reaching this near-godlike state was meant to be permanent; why not? If not actual gods how about the next best thing? The dynamic was virtue — civic and otherwise — leading to its attainment set in granite; ‘how to’ could only be earned with mastery and sustained effort. The means to virtue was self discipline, creativity and imagination. The civilized were certainly not paupers but it did not matter; the civilized whole was always greater than the sum of individual components.

Fast forward; godliness has been reduced one of a long line of frauds and sales-pitches, replaced by consumer goods and the banal processes to emit them. Virtue to- permanence is the antithesis of economic growth. Permanence means no markets for (new) smartphones, ‘e-cars’ or tract houses every other year or so, it also means nobody cares whether they have these things or not. Social media gadgetry, Sheetrock and plastic junk are offered up as aspirational, but these are meaning-free counterfeits, available to anyone with a charge card. In the place of civilization we have ‘the’ economy: it permits us to buy, to speculate, cannibalize, burn and waste and to borrow. Economy doesn’t allow us to ‘create our way out of the box’ — any box. Creativity gets in the way of the buying and the borrowing needed for the economic throughput regime to continue. Economy exalts mediocrity, sameness, loss of identity and transience, all in the service of fashion as the highest and most comforting (non-) virtues. The standards industrial economy set for itself are minuscule, the bar is always low, stumbling over it is easy, the costs, so far, are low. At the same time, the inability to stumble is never enough to undo the project. In this way mediocrity ‘normalizes’ or recalibrates the meaning of success in all the different ways to serves itself … to the point where half the people are busy reviving the corpses of the other half.

Mediocrity is itself an industrial product like (canned) pleasure and the ‘good jobs’ that never materialize. The physical products of industry are clichés rendered as such by design, they are the containers- or bearers of mediocrity. The mediocratic status of the products reinforces that of the enterprise that extrudes them like turds from the endless furnaces, pit mines and assembly lines. (False) hope — marketing — propels the process, the promise of something better, of a slightly less mediocre tomorrow. No wonder we are in a state of clinical depression: it’s “gimme the dope or get me out of here”! By jettisoning civilization we have left ourselves with nothing to reach for, we are stranded in the twilight, half-men, no longer godlike but not quite devils, either. We have become nothings, we are the sour taste inside our own mouths.

Growth has become the only permissible revolution against the status quo. ‘Old stuff’ is never good enough except with the added ‘nostalgia premium’. The imperative is always more, everything ‘more’ must be new. All else is subject to ‘creative destruction’. Even as these old things are proven useful, they ‘stand in the way of progress’ so out they go! Where does that leave us? Waiting for our chance at the Narcan.