Maurice Utrillo ‘Montmartre’

Maurice Utrillo ‘Montmartre’Not content with the stream of free money they have already received from the rest of us the banking ‘industry’ demands more:

WASHINGTON — The call from business for less government has a notable exception: the mortgage market.

The Obama administration invited banking executives today to offer advice on changing the government’s role in backing the mortgage market. While they disagreed on the exact level of support needed, the group overwhelmingly advocated the government should maintain a large role in the $11 trillion market.

If the government pulled out, executives said, millions of Americans wouldn’t be able to convince banks to take the risk of giving them home loans. Ending government support could lead to a spike in mortgage rates. That could deter many from buying homes, and banks, mortgage lenders and Realtors would lose money over time.

“It will take on a different form, but there is a role for government,” Kevin Chavers, a managing director at Morgan Stanley, said in an interview.

Most attendees agreed the time had come to do away with Fannie Mae and Freddie Mac. Rescuing the two mortgage giants has cost the government nearly $150 billion so far.

Bill Gross, the managing director for bond giant Pimco, suggested Fannie and Freddie should be formally merged into the government. He also called on the administration to allow millions of homeowner to automatically refinance their loans to help stimulate the economy.

A more widely held view at the conference is for government to do away with Fannie and Freddie, and instead provide a guarantee that mortgage investors get paid even if borrowers default in droves.

Figuring out a plan for Fannie and Freddie is also a political challenge for President Barack Obama and his party. Republicans have seized on the administration’s management of Fannie and Freddie to illustrate Democrats’ push for growing the reach of the federal government.

While the banking industry has joined Republicans in criticizing the administration for instituting stronger regulations of Wall Street, they understand the need for government to play a large role in the mortgage market.

“There would be a lot of homeowners who wouldn’t be able to afford homes because we’d be dealing with higher interest rates.” said S.A. Ibrahim, chief executive of mortgage insurer Radian Group Inc.

Outrageous! Would there be enough lampposts to hang them all! The racketeers who make up the US banking “industry” cannot be any more transparent. All that is left out is the, “or else!” that accompanied their identical demands during the Lehman Brothers debacle.

They certainly didn’t need a weatherman to tell which way the winds have been blowing since this crisis began. Whilst the overseers of the finance system, Greenspan and Bernanke, were blithely unaware of the consequences of laissez faire regulatory oversight – fed to them by the bankers themselves – the industry itself was well prepared to take advantage.

The entire rotting apparatus is illuminated in a flash as if by lightning: the remaining dumb- money rats are abandoning the sinking financial ship hard on the heels of the smart money. The fact of the abandonment speaks for itself.

The vicious cycle of unproductive labor leaves insufficient returns to service mortgages made upon houses – er – ‘large, wooden gambling bets’. What the banks demand is a blatant transfer of funds of borrowed taxpayer funds to themselves. What they offer in return is irrelevant to anything at all. When cheap energy disappears of what value are cheaply made suburban tract houses?

The much- made- of municipal and state finance crisis in the US is a part of the same piece; the availability of cheap energy allowed the flourishing of a form of consumption that is too expensive for (strapped) taxpayers to support. Not only are suburbs too energy- expensive directly but the preceding flight that suburbs engendered put paid to many of the urban areas that the suburbs now surround.

Where are the rats going to go? Europe? Singapore? How about a flight to Pandora? Since the problems are energy- related rather than debt or finance related there are no havens. Even Saudi Arabia is in many ways energy- poor:

The Gulf Co-operation Council are traditionally seen as hydrocarbon-rich, but in recent years that been a balance shift with the GGC now importing natural gas instead of exporting it.

This GCC gas shortage has been described as a “reversal of a decades-old status quo” with Bahrain, Kuwait, Oman, Saudi Arabia and the United Arab Emirates now facing an increasing gas shortage in the region amid a “significant supply overhang” in the rest of the world.

This has been highlighted in a report from Booz & Company, which states that “while the global economic slump has reduced the need for gas in most regions, demand in the Gulf Co-operation Council [GCC] for power generation from some industrial sectors has far outpaced the region’s gas exploration and production. As a result, GCC countries find themselves in an uncharted territory.”

Despite the six GCC countries holding roughly 23 percent of global gas reserves, the extent of the gas supply-demand imbalance in the region has seen the countries, with the exception of Qatar, consider importing gas to meet rapidly rising demand.

Even with these measures, the GCC is still facing a serious gas shortage.

With increased power consumption and gas being utilised for generation combined with steady growth, the countries of the GCC have seen their economies grow at a rate of around 7.6 percent a year. While energy demand has kept pace with such growth, it is expected that power generation needs for the region will increase by 50 percent over the next two decades.

According to studies by the US Energy Information Administration (EIA), more than 90 percent of the region’s power generation will come from gas, significantly increasing the GCC power sector’s reliance on gas.

Here’s more on the shrinking energy balance sheet from Jim Hansen’s Master Resource Report:

Natural gas in the Middle East?

“What does Kuwait importing LNG from Russia, the United Arab Emirates (UAE) constructing nuclear power plants and Oman importing coal all have in common? They are all symptoms of the same problem – the Arabian Peninsula is gas short.” In fact some like Dubai are both gas and oil short because they live in one of the most energy intense environments in the world.

In a recent report Wood MacKenzie even faced up to how the natural gas problem will make the net export problem worse than it is expected to be. Constrained natural gas supplies “… in the Arabian Peninsula is forcing increased oil consumption to 2030. This has significant implication for oil exports from the region.”

This is not news to readers of this report but it is significant that a firm like Wood MacKenzie is beginning to wake up to the situation in the Gulf as it pertains to how natural gas and oil interrelate to impact not on LNG exports but oil as well. It will also have a very large impact on the development of industrial activities such as the growing petrochemical industries of the region.

“The development of shale gas in the US will free up LNG that was previously destined for the US for other markets – Arabia being the prime candidate,” it said.”

If global shale gas and the IS in particular don’t prove to be the panacea that its fans promote the global LNG market could prove to be a very expensive place to be buying energy. Even more important would be if some of the LNG exporters in the Gulf region in particular determined that their own internal demand wouldn’t allow those levels of LNG exports. In that case the LNG supply chain could become a broken chainOne area that is getting little attention that is built on the thesis that the Middle East will have abundant and cheap natural gas is gas-to-liquids. In particular the production of liquid aviation fuel for the rapidly growing airlines such as Emirates Airline based in Dubai. An entire industry is being built on assumptions that should already be called into question.

It is beginning to sound like there are plenty of countries building energy policy around everything working flawlessly as expected. Sounds more like a road to disaster.

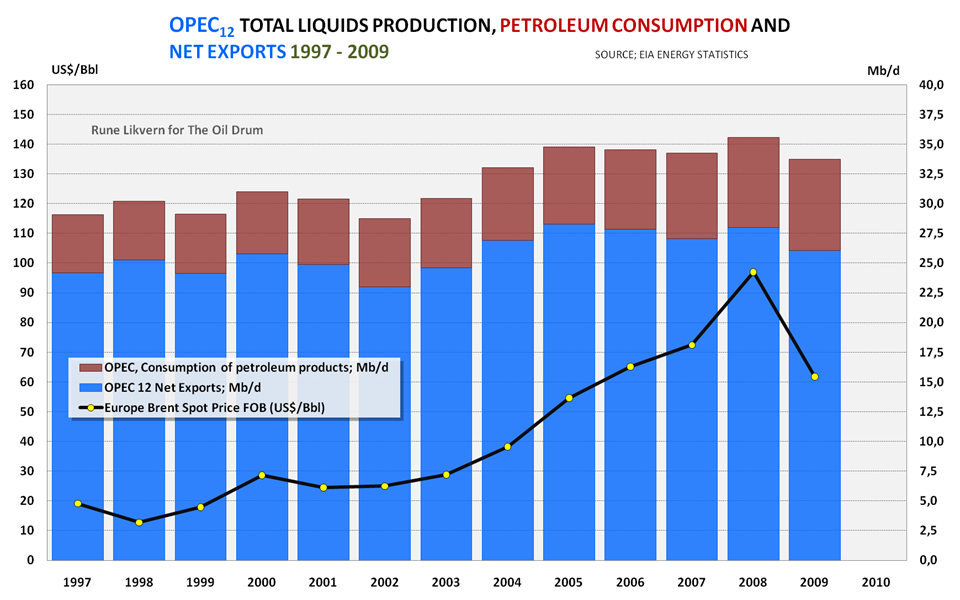

We are experiencing right now and have been for the past ten years an energy rather than a finance crisis. What matters is energy availability at a price.

It’s hard to escape interconnections in a global economy. Read Andy Xie:

We are seeing the interplay between the forces of globalization and policy mistakes. Globalization has severely restricted the effectiveness of economic stimulus. Trade plus FDI are half of the global GDP. Trade is visible in terms of stimulus leakage. But, where investment occurs in response to demand growth is far more important. Multinationals can invest anywhere in response to demand. It cuts the linkage between demand stimulus and investment response. The latter is crucial to employment growth, which is necessary for sustaining demand growth beyond stimulus. Essentially, demand is local, but supply is global. This is why the old assumptions on stimulus are no longer reliable.

Energy availability at a price: availability of anything (of oil, coal, cola, hair dryers, etc …) is dependent in turn on four things:

– the production of (lower priced) existing reserves,

– production of (higher priced) replacement reserves,

– net exports,

– the price that supports all the above.

If the price of fuel is too high demand will eventually drop. Then the price will drop. When the price is too low the production of replacement reserves above that price is shut in, net exports above that price are not shipped and what remains is the shrinking amount of lower- priced fuel that can be produced out of existing reserves. Once it becomes apparent that this diminishing reserve of low- priced oil is all that is available it will likely be rationed carefully rather than being dumped on the market. The ability of an industrial economy to raise funds so as to produce reserves, import at a higher price out of output or to craft alternatives vanishes.

The amount of cheap, easily produced oil is shrinking fast. Why? Because of depletion’s effect on output profits AND because the marginal barrel is now located 25,000 feet below some ocean’s surface. The ‘effect of production costs on profits’ curve must be added to the net export curve and that of physical depletion.

Companies don’t make money selling goods, they profit by the steepest yield curve in history; borrowing from the Federal Reserve @ -1% and lending money to the US Treasury @ 3% … and by firing workers. Energy use at today’s prices is unprofitable, yet the price of crude that is unprofitable to business is at the same time too low to support production of new oil.

Events of 2005- 2008 demonstrated the inability to replace current production at any price!

Start with the depletion rate of domestic (US) production, subtract net exports (to the US), subtract from the subtotal the amount of new production at a reduced cost (because of increasing poverty). The amount of oil available under this set of circumstances shrinks very fast indeed. And keep in mind, when the shortages hit, they will be permanent. In a depletion context there is no new wealth that can be shifted to oil producers to gain more available reserves.

Our industry ‘profits’ from the waste of fuel. The money return on destroying a resource must be greater than the money value of the resource itself otherwise the resource cannot be brought to the market. Scarcity makes the oil resource too valuable to waste. We have created a defective waste- based model and built a defective infrastructure to support that model. Now, we believe we must use the same defective model to craft a replacement on a scale that can only be enabled by destroying the last marketable resource!

Is this insanity or what? The combined energy costs of running the current model added to the energy costs of crafting a replacement are unsupportable on their face! The model cannot support itself now. The ‘return on waste’ nears zero! Attempting to use the model to leverage another will be the overload that collapses the system. We can only craft a replacement energy regime when the existing model and its demand on resources is powered down. Then we MIGHT be able to use what remains to craft a more capital- enhancing model.

Far more capital will be required to increase availability than is required currently. Note how much the Macondo well cost, (and factor in BP’s cheating). Oil is more and more expensive to produce. If we cannot leverage commerce profitable enough to pay the capital expense our experiment in industrialization is done.

What is that profit/price level? The current price of oil is a ‘wealth barometer’. In 2008 the world was rich and could afford $147 for a little while. Today we can afford $87. This is not a good trend when replacement oil costs + $70 a barrel to produce.

The wealth barometer could tip down to – $50 at any time, within months. The trend has been down since 2008. The world is getting poorer; what does ‘wealth’ mean, anyway?

Prior to 2005 it could have meant equity in real estate, credit derivatives or access to credit, now it becomes ‘cash in hand’.

The bottom line is the historical concern of living within our means, to cut the fiscal, personal – and energy – deficits to what can be supported by the careful husbandry, so that there is a return on oil’s USE not WASTE, where oil becomes capital to increase the same way agricultural capital is increased. This means an economy that makes capital use of what remains of our oil resources long term. Since we waste close to 20m barrels per day a reduction to a sustainable domestic rate of production over the long term (1,000 years?) would be less than one million barrels per day. This means an industrial economy that is ONE- TWENTIETH (1/20th) of our current version!

The same calculation can be made with finance capital; the size of an economy that is sustainable without a debt overhang is orders of magnitude smaller than current. No wonder the politicians and racketeers are scrambling. The tidal forces of gravity and entropy are pushing the world’s waste- based economies into terminal shrinkage.

Without easy credit and reduced to cash, what would be the value of residential real estate? Cars? Office buildings? Any other form of capital? The value would be excess earnings or surplus gained by labor: what people could save in a reasonable period of time – that is, before they died. The cash value of goods of all kinds would be the same as the balanced energy value; about 1/20th of current levels.

If the oil price drops low enough the shortages will start almost immediately and the system will grind to a halt in an energy- shortage compounding spiral. The time frame would be months not years. A low oil price would not mean a gift from oil producers but insufficient return on the energy input.

We are rapidly approaching the juncture where the current price of energy is too low to bring fuel to market while the same price is too high to allow “productive” and profitable returns on the waste of that fuel.

This is a shrinking corner that no industrialized country can escape. China and Germany claim the returns on their industrial output but that output is waste enabling. Without customers with funds they may as well produce nothing at all. The same is true for the US which has posted itself as the ‘great middleman’ demanding a rent percentage of all transactions in all markets … while representing the ‘final demand’ of a large part of these transactions. Yet, there is no net output from simple demand, nothing to exchange to those who create the output.

What is left is blatant thievery and the hope of escape … to where, exactly? Who knows?