Surreality is when the top story in the New York Times is about King Cakes but the idea is to not scare the horses. Informing the readership in plain English of our ongoing unraveling might provoke uncertainty … then panic … leading to questions about why we endure so many stupid managers everywhere in the world. At the very least, the stock market — which is now near all-time highs — might decline. People might then in theory put off buying a new car or a bigger house or not take on bigger loans. Best to roll out the pastries and downplay the Israeli air strike in Syria and the widening war there or the bank nationalization in Netherlands (Washington Post):

Dutch state nationalizes bank and insurer SNS Reaal NV, injects 2 billion euros in capital(Associated Press)

AMSTERDAM — The Netherlands nationalized its fourth-largest bank on Friday, injecting €2 billion ($2.7 billion) to recapitalize SNS Reaal NV and head off any chance of a messy collapse that would threaten the country’s already fragile economy and financial system.

The total cost to the Dutch government will be at least €3.7 billion, Finance Minister Jeroen Dijsselbloem told a press conference. That’s almost certainly enough to ensure that the Netherlands’ budget deficit in 2013 will be higher than the 3 percent allowed under EU rules, unless the Dutch Cabinet — which has already taken a series of unpopular tax hikes and spending cuts — comes up with further austerity measures.

“This isn’t what we wanted,” Dijsselbloem said. But he added that, without the nationalization, SNS “would have gone irrevocably bankrupt,” with potentially dire consequences.

Ah yes, dire consequences: secured (large) lenders to the bank would have lost some money. Much better for the ordinary citizens of Netherlands to take the billions in losses. The citizens haven’t even earned the money yet, they will never know what it is they have lost! Here is the latest innovative technology in action: the finance cost-morphing time machine. The establishment endlessly promises a high-tech utopia tomorrow. What it actually delivers is invisible public bankruptcy: money that is not earned tomorrow because it was diverted to a tycoon … yesterday.

High-tech time machine in operation, Pableaux Johnson (NYTimes)

Depositors and senior creditors (of SNS) won’t lose any money in the nationalization, the Finance Ministry said.

The closest the Dutch get to actual restructuring …

SNS shareholders will be wiped out, along with some junior creditors, including the state itself. SNS owed the government €800 million, including interest, left over from a 2008 bailout. Other junior creditors will lose around €1 billion, the ministry said. The three biggest Dutch banks, ING Groep NV, ABN Amro, and Rabobank will contribute a combined €1 billion to help save SNS — they are required to do so as under the same law by which the state guarantees their retail deposits.The nationalization shows the damage the crisis has wrought on the oversize Dutch financial sector and means that three of the five biggest banks in the country have now come under state control since the start of the crisis: ABN Amro was merged with the former Fortis and both were nationalized back in 2008. In addition, ING received several bailouts which have still not been fully repaid. Only Rabobank, a banking cooperative, has not yet needed state aid.

Big-bank shutdowns are historical indicators of greater finance system failures-to-come. This dynamic has been in force as recently as 2007 with the collapse of el cheap-o mortgage origination firms and two of Bear-Stearns’ hedge funds. The entire mortgage industry, shadow-banking and then Bear-Stearns itself all fell into the pit shortly thereafter. During the entire period there was a soaring stock market and soothing bromides from the establishment …

Attention must be paid to stumbling banks while the happy talk about ‘growth’ and ‘recovery’ is ignored.

The propping up of key-men works for modest periods only. Cures or resolutions must be put in the place of the props … since 1980 or so nothing has been done other than to entrench the status quo, expand credit and inflate serial asset price ‘bubbles’. Finance has not evolved, it has become an unchanging dead weight, a gigantic millstone around the corpse of modernity … ossified finance has become the final manifestation of ‘progress’. To support banks and the industrial welfare queens there are cheap loans offered by central banks, the laundering of assets, bailouts of businesses belonging to ‘special friends’ (owners) of corrupt government officials. All of this is accompanied by loud public proclamations of better times that are sure to come, tomorrow.

It is always tomorrow … when the positive outcomes are certain to emerge! As a fair exchange businessmen will poison the atmosphere and the ocean so that progress can take place. Meanwhile the key-men multiply like rabbits while the props diminish or crack under the strain.

There are banks and bank-like entities faltering in China, in Spain, as well as Italy, where the Banca Monte dei Paschi di Siena SpA is underwater due to self-dealing and looks ripe for failure. All of these situations have the potential to upend the economic applecart. Of course, there are the parallel political scandals in all of these countries including China. One must not overlook the Greek and Cyprus problems … or the foreign exchange ‘war’ that is underway between the US, the eurozone, China, Japan and Korea.

The term ‘Dutch’ can be replaced with the name of just about any country …

‘France is totally bankrupt’: French jobs minister Michel Sapin embarrasses Francois Hollande with shocking statement on state of the country’s economy …

Sapin is shocked … shocked! The economy of France is a Ponzi scheme where the funds/capital of other countries is taken in exchange for empty promises … gambling and fashion have bankrupted the country, there is nothing left for France but to become Greece.

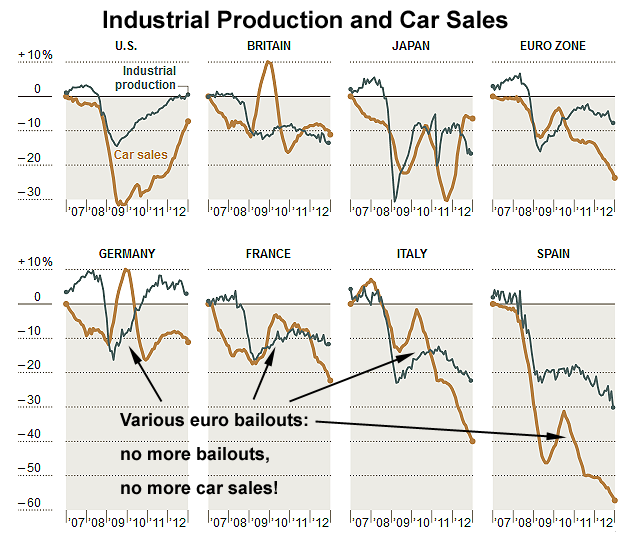

Figure 1: Charts of car sales here and there from the New York Times: sales nose-dive in Europe. Sales are dependent upon the constant addition of credit-plus central bank moral hazard … as these offer diminished returns there is nothing to support sales

Industrial production figures exclude construction, and reflect the change in each month from the average of 2006 figures. Car sales figures exclude light trucks, and are based on sales volumes in the United States and on registrations of new cars in Europe and Japan. They reflect the total for each 12-month period compared with the 2006 total.(Sources: Bloomberg, Haver Analytics, Ward’s Automotive, European Automobile Manufacturers’ Association)

Autos and other capital-extinguishing goods are collateral for our money, they are the tangible ‘products’ for- and by which we devour our pitiful remnants of real capital … We can continue to destroy capital only if we lie to ourselves about its nature. Currently, we insist that capital is money instead of resources. This is false: money is loans and nothing more. When capital is loans, there are insignificant consequences to its destruction. Old loans are easily replaced with new ones. Only when capital is something that must be dug out of the ground with great effort … does its fleeting existence within our state of affairs become an economic embarrassment … then an indictment.

Meanwhile, finance is losing its ability to paint capital destruction as ‘productive-appearing’ and to thereby prop it up. Here is the greatest key-man failure! The more effort expended to keep the current regime of capital destruction ‘growing’ the faster the costs accumulate … capital is extinguished with one hand while greater claims against the same capital are made with the other.

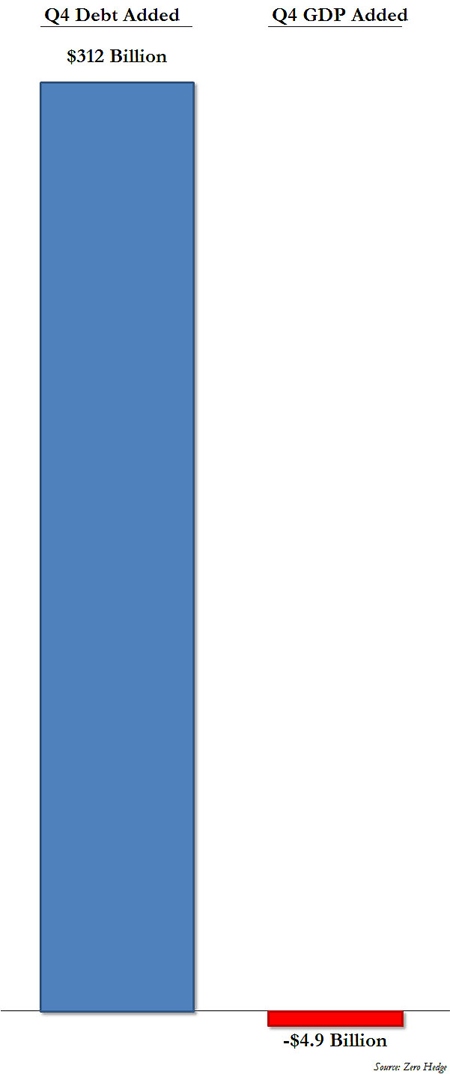

Figure 2: What sort of un-balanced sheet is this? Here are diminished returns made graphic … the declining productivity of US debt, as $300+ billion borrowed dollars ‘buys’ a $5 billion dollar decline in GDP (by Zero Hedge). This decline can be ignored as long as … the stock market keeps rising! (click on the image to see it in its entirety)

Meanwhile, from the ‘Let The Eat King Cake’ department … in China, (Patrick Chovanek):

What Causes Revolutions?A surprising number of people in China have been writing and talking about “revolution”. First came word, in November, that China’s new leaders have been advising their colleagues to read Alexis de Tocqueville’s classic book on the French Revolution, L’Ancien Régime et la Révolution (The Old Regime and the Revolution), which subsequently has shot to the top of China’s best seller lists. Just this past week, Chinese scholar Zhao Dinxing, a sociology professor at the University of Chicago, felt the need to publish an article (in Chinese) laying out the reasons China won’t have a revolution (you can read an English summary here). Minxin Pei, on the other hand, thinks it will.

This is like the German high command during the Barbarossa winter of 1941 re-reading Armand De Caulaincourt’s classic account of Napoleon’s doomed 1812 Russian campaign. Sentries that have frozen to death tend to focus the mind: so do the endless rounds of Chinese outrages and miscalculations. Doubts about China’s enterprise are growing … in China, where such doubts matter most.

What would a China revolution look like? Pundits offer a political story about the Communist Party but the problems are economic: the failure of Chinese business ‘success’. Any revolution would certainly take some form of public rejection of automobiles … otherwise there would be no real revolution at all. Such a radical change is unlikely at the moment … The Chinese love their cars … the passage of time and the ongoing bankruptcy of China will do the heavy lifting. The Revolution will come after China becomes Greece.

What must be watched are the banks which are saddled with US$ trillions of bad loans, mostly for ‘capital investment’ which in this case means redundant factories, showy-but-useless public infrastructure and property developments. None of these things can or do pay for themselves, they require endless rounds of new loans … the result being pyramiding debts. Amazingly, it has taken the Chinese only 20 years to reach the profound level of insolvency that has taken the West 400 years to achieve. It is hard to see the Chinese expanding their particular form of capital investment Ponzi scheme … and the accompanying smog … for another 20 years.

The Chinese are not the only folks struggling with air quality: the smog is worse in India … for many of the same reasons as China. The smog is also bad in Athens … Greeks are putting heating oil into their cars and heating their houses with stolen wood.

Another finance debacle in the making is Japan’s desire to ‘Whip Deflation Now’ and depreciate the yen all at once, (Bruce Krasting):

Figure 3: The chart looks like the Yen has weakened in lockstep with both the Euro and the Dollar. But when you look at the scale, you see that the Yen has lost 22% against the Euro, while it has only given up 13% versus the dollar. From this you might conclude that the logical next step is for the USDYEN to “catch up” to to what has happened with the EURYEN. This thinking takes you in the direction of USDYEN 100.But … the FX markets don’t work like that. If USDYEN moved to 100 while the EURYEN remained “stable” around 122, then the EURUSD rate HAS to fall to 1.22 (-9%).

Sorry, that’s not in the cards.

Depreciation from ¥80 to the dollar to ¥100 means a ‘Great Leap Upward’ in Japanese fuel prices because the country has no native sources of petroleum or other fuels. Japan beggars itself instead of its neighbors: whatever the country hopes to earn by exports is offset by the increased cost of the fuel it must import. At the same time, dollar-fuel prices are increasing because of ‘growth’ propaganda, moral hazard for petroleum ‘investors’ as well as threats of war in petroleum producing regions. With depreciation and higher producer costs the Japanese driver can look forward to paying a deflationary 30% or greater premium for fuel compared to the rest of the world. Certainly, here is conservation by other means!

The foregoing omits systemic risk to Japanese banking and finance which cannot be easily measured. The smallest error can have shattering consequences. For example, the Bank of Japan central bank can be perceived by the marketplace to be making unsecured loans … that is, loans in excess of collateral that it takes on as security. If this is so, the central bank is instantly insolvent … as are other Japanese banks and for the same reason: bad loans and excess leverage! Keep in mind, the only reason why a central bank would think of offering unsecured loans is if the country’s commercial banks are insolvent and unable to lend. The outcome is no effective lender of last resort to guarantee bank liabilities: a run occurs as depositors hustle to remove funds from a defunct system. In this light the recent months’ acquisitions of overseas companies by Japanese businesses is ominous.

There is also the issue whether Middle Eastern suppliers will accept a strongly depreciated yen or if they will demand another form or payment (dollars). The Japanese are playing with fire, looking for an easy, conventional approach that cannot possibly work as intended. Whatever the country attempts there are unintended consequences … which often cannot be discerned until after the attempts are made and it is too late to change course.

What the establishment in Japan fails to understand is the effort to accelerate consumption — either within the country or by trading partners — offers sharply diminished returns. This is because irretrievable capital is consumed instead of rapidly multiplying ‘money’. Because of consumption over the course of decades real capital has become more costly relative to the amounts that can be lent against the consumption process. When returns become negative … the country in question instantly enjoys a Greek-like national bankruptcy.

The bankruptcy is permanent, by the way … the only way for a Greece to become prosperous again is for another country to become more bankrupt than Greece is now.

This net-negative process may indeed be underway in Japan as what it exports must be imported first then subjected to entropy-creating industrial-commercial processes. Every process exacts a thermodynamic levy or ‘tax’, certainly export goods cost Japan more in energy losses than what Japan imports.

A country can make water flow uphill by pushing costs onto unwitting trading partners by way of foreign exchange and leverage against that partner’s account. Japan’s trade surplus — which has subsidized Japan for decades — is nothing more than faulty bookkeeping and overseas loans. Japan has pushed its energy costs onto its customers: the attempt at depreciation is an effort to restart the pushing process.

Meanwhile, all the other consuming countries in the world desire to depreciate their own currencies as well! More of Japan’s customers are broke, they cannot afford to subsidize Japan’s waste any more … or their own.

Certainly, there must be intelligent, perceptive analysts in France, America, China and Japan … however the power of habit and wishful thinking is very strong and the current lesson of Greece being played out on the public stage in real time … is ignored.

While countries beggar their trading partners, many of the same countries are bent on outright theft. War intensifies in the Middle East, in Africa, it stirs off the coast of revolutionary China … every place there is oil or oil consumption that can be ‘exported’ to countries such as the United States. The outcome is increased war premium (Bloomberg):

| Commodity | Units | Price | Change | % Change | Contract | Time(ET) |

|---|---|---|---|---|---|---|

| Crude Oil (WTI) | USD/bbl. | 97.97 | +0.48 | +0.49% | Mar 13 | 11:45:10 |

| Crude Oil (Brent) | USD/bbl. | 116.96 | +1.42 | +1.23% | Mar 13 | 11:45:16 |

| RBOB Gasoline | USd/gal. | 302.58 | +2.21 | +0.73% | Mar 13 | 17:15:00 |

Crude prices increase until the customers cannot borrow any more … from here it looks that $120 Brent will be where customers are shut out of the market. Ugly noises from the banks are the indicator.

King cake is a New Orleans tradition served on Fat Tuesday before Mardi Gras. King cake by Sara, who clearly knows how to bake a good one! Any recipe will do as long as it includes sugar. A small plastic doll stuck into the cake after removal from the oven. Note: there are no such things as ‘clashing colors’ in New Orleans …

The survivors of the current state of affairs are those small businesses that do not require credit and can obtain organic returns. As for the others, let them eat king cake.