The past year and a half has seen the relentless unraveling of the post-Lehman recovery, the vaudeville act duct-taped and wired together on the ruins of shadow banking … taking the place of a reflective determination why ‘shadow banking’ is necessary in the first place.

Deflation, or rather, entropy has set up shop on our doorsteps. Call it ‘capital E’ entropy: the Golem we have created by way of our blithe and dithering squanderousness. Entropy cannot be bargained with, it can’t be reasoned with; it doesn’t feel pity or remorse … etc.

Entropy has put all the countries, the regions; all the economies under siege. All are struggling with credit market distortions to some degree, from the diminution of purchasing power to the greatest degree. An important and growing fraction struggles with the consequences of pointless wars and the resulting tides of migrants, other fractions are crushed by debts that can no longer be serviced out of cash flows. There is insolvency, inter-temporal contagion and more deflation in a vicious cycle.

Along with the cycle is the frantic scramble for the next ‘solution’ … even as the only workable response to ‘less’ is stringent conservation. Purposefully doing without is never part of any conversation, it’s unpleasant, it does not offer a fabulous future or much in the way of hope …

There are endless attempts to escape consequences: to cash in, (cash out?); cries for bank bail-ins, increased austerity or the relaxation of it, more quantitative easing or less of it, negative interest rates or higher ones; always more loans adding to what we have in monstrous proportion, a mountain of claims looming over relentlessly diminished purchasing power. We are insolvent, in that purchasing power is the ‘currency’ which we must obtain in order to retire our debts.

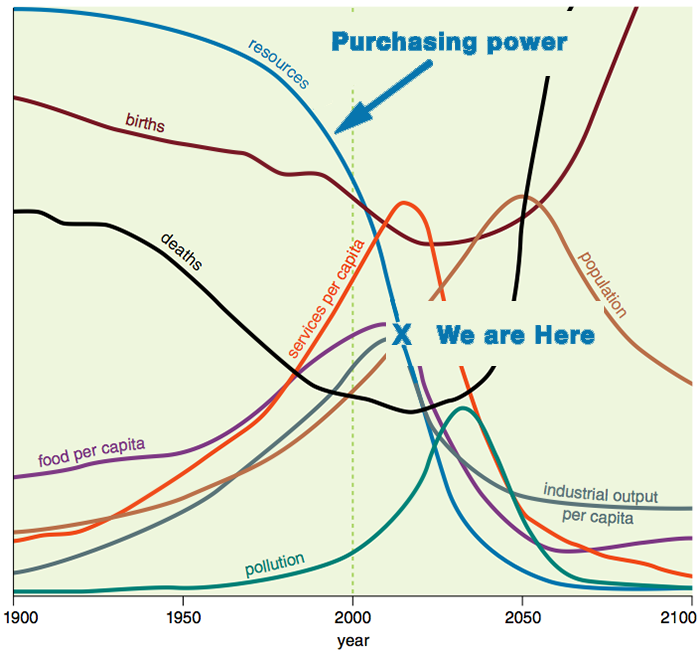

Figure 1: The long meander to oblivion, this diagram from 1972 ‘Limits to Growth’, Meadows et al, illustrates what we are up against. The best the establishment can come up with is a non-sequitur:

It’s time to kill the $100 bill

… illicit activities are facilitated when a million dollars weighs 2.2 pounds as with the 500 euro note rather than more than 50 pounds as would be the case if the $20 bill was the high denomination note. And he is equally correct in arguing that technology is obviating whatever need there may ever have been for high denomination notes in legal commerce.

It’s hard to know whether to laugh or cry over the absurdity of it all. Absurdity of it all … Absurdity of it all.

Illegal money transfers have been made electronically, in their billion$ by HSBC and other giant banks. The largest recent single user of US currency is the US military. Summers conveniently ignores the greatest criminals are the bankers, who pay themselves, not with used, non-sequential $100 bills in brown paper bags, but with electronic bonuses.

Establishment economists such as Lawrence Summers can be excused for failing to understand ‘purchasing power’ the way it is described here at Economic Undertow. It isn’t taught at Harvard or any other school nor is it a part of an equilibrium economics curriculum. It tends to be understood as the amount of finished goods or services that can be gained in exchange for a unit of credit. More units = more goods = greater wealth. More valuable units also = more goods and wealth. The idea is to manipulate the number of units to access more goods and to prosper; manipulations haven’t been working lately and the economists have no idea why.

In Debtonomics, purchasing power is the relationship between resources and the ‘work’ needed to make resources available. Because resources DO the work as well as being made available BY the work, consuming resources also consumes our purchasing power at the same time. This mirrors what is observable in the real world and explains why adding ‘money’ hasn’t accomplished anything, we keep getting poorer all the time.

Resources and purchasing power are not the same but they may as well be, their relationship is unitary. One obtains or ‘purchases’ the other by way of the application of energy to displace matter over time: ‘power’. Each fraction of purchasing power represents an equal proportion of capital — resources — available to us. As capital vanishes into our machines, our purchasing power is irretrievably extinguished. With the passage of time- plus industrialization there is less of it. In Debtonomics, money is a derivative claim against purchasing power; so are labor, infrastructure, industrial production even the industries themselves. Changes to the particulars of the different claims such as numbers on a spreadsheet, technology, worker productivity or interest cost are irrelevant; when we run down our resources we are ruined regardless of how much ‘money’, or other industrial bits and pieces we have.

Summers’ argument is disingenuous; currency controls are not to thwart criminals but aim to prevent bank runs if- and when deposit rates turn negative. Runs destroy whatever system being run from, whether it is finance, currencies or banks. Summers’ proposal ‘works’ in the sense in that it traps depositors’ funds so a run becomes difficult, but it undermines depositors’ faith in the system at the same time, it is destructively counterproductive.

The establishment’s first instinct is to punish, to lash out and destroy. Our systems are built upon continuing, exponential monetization of waste. When punishment and devastation do not produce the desired outcome, we try harder, reaching for the succession of ever- larger hammers. After the $100 bill is turned to gristle, the $20 then the the $5 will meet the same fate. What’s left is change rounded up beneath the seat cushions. When that time arrives a nickel will be worth today’s $100, fatally undermining the well-crafted ‘policy proposal’ of the ex-Secretary of the Treasury and Director of the Mossavar Rahmani Center for Business and Government at Harvard University!

Summers proposal would effectively shrink the supply of liquid funds, amplifying dollar preference, something else not taught at Harvard. This would rebound against the fuel supply system. Removing funds from the customer = less of a bid for fuel products and lower wellhead prices which strands the drillers; ultimately rendering the entire industry insolvent.

Everything Has To Be Perfect Forever!

Excluding the rates paid (charged) on reserves held by central banks, negative interest rates are largely a market phenomenon, they reflect a retreat out of risk; the ‘flight to safety’. They occur when there are more loanable funds available than there are low-risk investments that can absorb them. There does not have to be much of an excess of these funds for interest to fall negative; like the price of crude oil, rates emerge at the margin. Negative rates apply to securities which are considered ‘money-like’ such as sovereign debt. It is government bonds that offer negative returns.

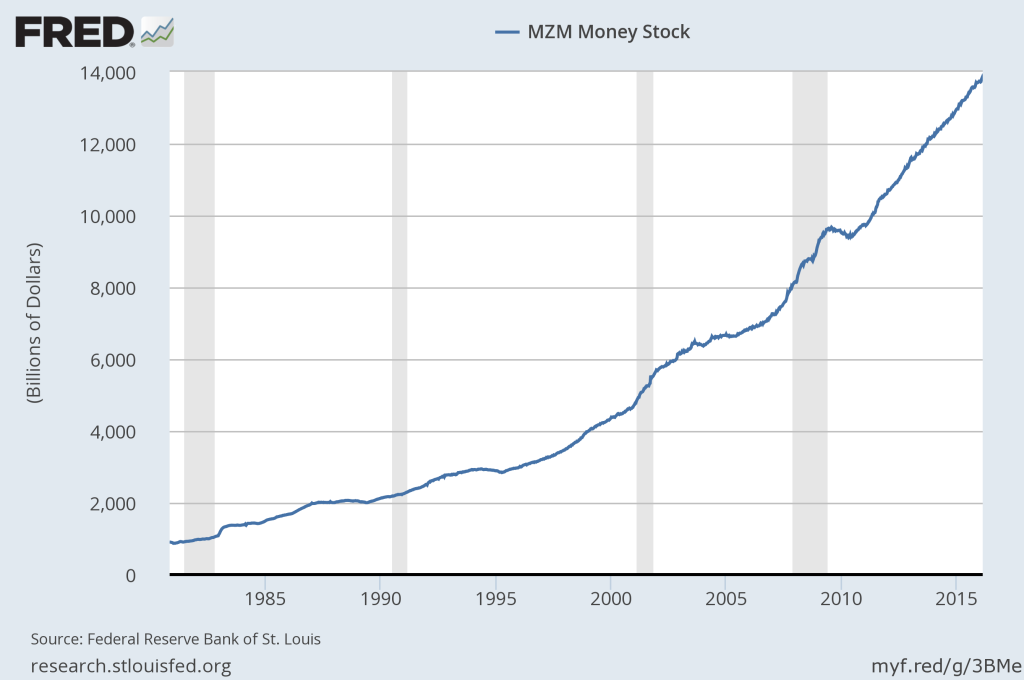

Figure 2: MZM money stock, (Fred). ‘Zero-maturity’ money is liquid funds in the economy (excluding time deposits/certificates of deposit). At the same time finance lends more funds into existence there are fewer destinations for them … they migrate into safe harbors such as bank deposits or credit equivalents.

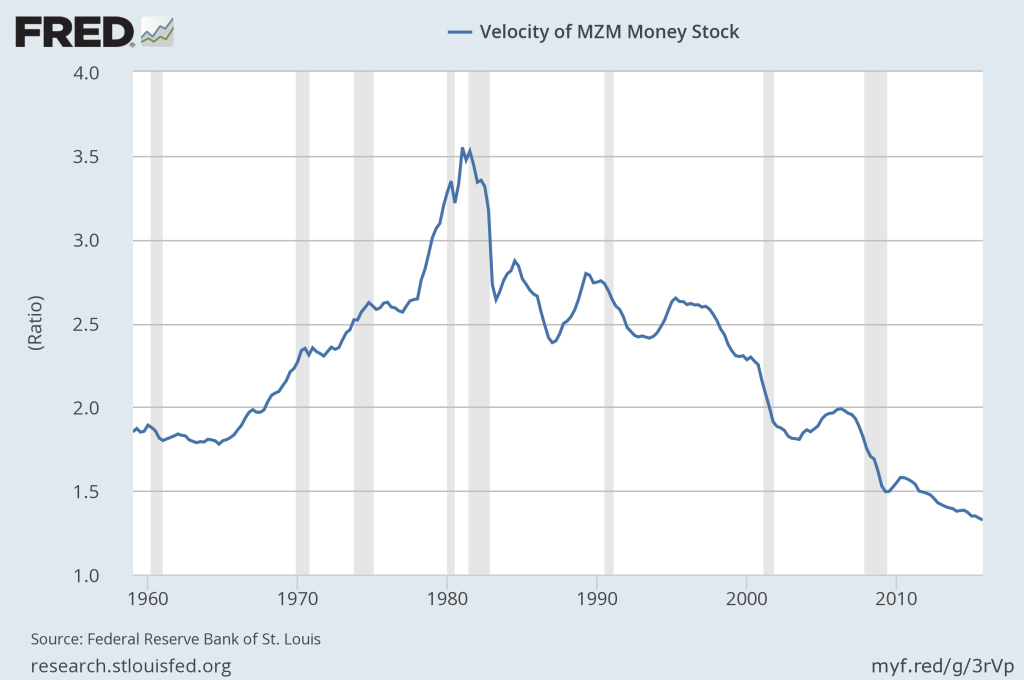

Figure 3: MZM velocity has been declining for years, the reduced flow cancels out increases in the money stock. The bankers are pushing on a string, no wonder they are desperate.

Negative rates indicate the absence of good investments in the functioning, day-to-day economy; they are the imprints of deflation. Whether or not the central banks are in control or not, promoting deflation is not the bankers’ intent. Instead, it’s an unintended consequence of efforts to bail out private finance at public expense.

Central bank manipulation gives the illusion that risk has been ‘legislated out of existence’. This is dangerously false; risk is a First-Law cost associated with the surplus of debt. Increasing the surplus of loans spreads risk around or pushes it out of sight, but only for a little while. Exponentially increasing risk lurks beneath very low/negative rates like a tiger in the jungle. The performance of the loans depends on the ability of international deadbeats such as the Italian government to borrow endlessly into the future, for everything to be perfect forever! Risk springs out of hiding when supposed pristine borrowers stumble and the loans are marked to market as junk. Under the circumstances, losses to the hapless bond speculators and central banks are astronomical, bankrupting the entire banking system at one go!

Risk also manifests itself as increased operating expenses for businesses that lack assets to sell to the central banks. These added costs accelerate vulnerable firms’ drift towards insolvency which in turn torpedoes the firms’ lenders, stampeding investors’ toward government bonds and (perceived) safety. All of this makes the risks worse. Surplus-related costs also discount the overall worth of commerce relative to holding currency = more dollar preference. Intervention endangers through the back door the very enterprises the bosses are desperate to support …

Bringing Excess Claims into Alignment With Purchasing Power.

As the bosses vie to increase growth they undermine themselves by destroying resources. They tilt the balance toward increasing claims while purchasing power is cannibalized. Whatever pittances are gained in the immediate-term are at risk going forward as the overhang of claims increases. Alternatively, removing claims tilts the balance the other way: borrower defaults, debt write-offs; by hoarding money or confiscation = ‘Conservation by Other MeansTM‘.

Managers want low-cost money to keep their Vaudeville act running as long as possible, even as it has exhausted itself by every reckoning including its own. Forced credit expansion no longer stimulates business expansion or growth. More costly money would accurately price in the risk that is ballooning (out of sight) within the system.

Managers want their currencies to be cheap so they might increase goods exports and gain foreign exchange. Forex becomes collateral for domestic loans leading to the mercantile increase in ‘wealth’, (China). This strategy fails when all managers strive to export at the same time. The outcome is diminished trade overall and less Forex collateral, amplifying deflation in a vicious cycle. Currency depreciation is also counterproductive for credit providers such as Japan, the US and UK. When credit is a country’s only real product, depreciation represents a reduction of the country’s output. This is also ‘Conservation by Other MeanTM‘ as the credit provider cannot finance imports by ‘borrowing’ them with its own currency.

Managers also want money that is worth less than commerce so customers lack incentives to hold onto it. This is also dangerous as money can become so cheap that commerce becomes unaffordable, (Venezuela).

Diminished finance sector returns, or Net Interest on Margin (NIM)

Figure 4: Because finance creates its own funds it has no need to borrow. Interest margin represents the narrowing spread between finance returns from loans to largest- and presumably most creditworthy borrowers and returns from lending overall. NIMs have been declining for decades along with velocity and are, ironically, the consequence of increased financialization and declining customer income. Reducing interest paid by the central banks on excess reserves narrows NIMs further, undoing the bailout effects of QE.

Outcome

There is no overcoming entropy or declining purchasing power, only strategies to ameliorate the consequences and preserve resources/purchasing power for the future, along with some small component of institutional integrity. Managers fail to grasp the seriousness of our onrushing predicament: the destructive potential of declining resource availability/purchasing power is equal to- or greater than a nuclear exchange, the results are just as permanent. If managers aim to destroy this country, doing nothing- or more of the same is a good way to go about it! The establishment obsesses about money even as the real problem is a shortage of resources needed for our economy to produce the goods and services we expect. What needs to change are expectations. The money-system failures are symptoms of our resource shortfall, including declining petroleum prices and the widening circle of related industrial and finance insolvencies. Schemes that seek to maintain the status quo are certain to fail. Almost all of them are variations on the theme of bond-buying, dubious accounting and trickle down economics = robbery. Almost all of them depend upon central banks which have grounded themselves on their own policy contradictions. Absent change, financial accountability will enter through the back door as central bankers and the their private sector clients are engulfed by the system collapse taking place under their feet. One way or the other, finance claims will be brought into alignment with purchasing power. The hardest path is the annihilation of claims along with finance at the same time.

Thinking Outside the Banking Box.

One way to start down the road to voluntary alignment is to ‘buy down’ claims. The US government has the authority to produce money by itself, without borrowing; “to coin money, regulate the value thereof, and of foreign coin, and fix the standard of weights and measures;” (the implication is that money is a tool of measurement.) Article 1, § 8, Constitution US, (Legal Information Institute, Cornell University).

— A $100 US Note, a late(st) model ‘Greenback’. Congress allowed the ‘float’ of $346,681,016 of these notes, however, they are out of circulation with the vast majority having been destroyed by the Treasury.

“If the Nation can issue a dollar bond it can issue a dollar bill.

The element that makes the bond good makes the bill good also. The

difference between the bond and the bill is that the bond lets the

money broker collect twice the amount of the bond and an additional 20%.

Whereas the currency, the honest sort provided by the Constitution pays

nobody but those who contribute in some useful way. It is absurd to say

our Country can issue bonds and cannot issue currency. Both are promises

to pay, but one fattens the usurer and the other helps the People.”— Thomas Edison

Last Summer the Undertow examined the possibility of Greece issuing ‘greenback’ or non-liability fiat euro notes. Greece would use the euros to retire maturing debt and to facilitate internal exchange that was — and currently is — stifled by the overhang of debt and the accompanying demand for repayment. While note issue cannot ‘fix’ structural problems outright, it is possible to ease immediate monetary pressures and use the opportunity to put into effect a conservation plan, (get rid of the machines).

As in Greece, the purpose of US notes would be reduce the overhang of debt-claims and the accompanying demand for repayment funds; to bring claims and purchasing power into better alignment. Issued notes would retire maturing debt without requiring new debt to replace it. It’s a legal ‘cheat’, Bankers will object, but creeping system insolvency leaves them in no position to do anything but complain. By way of notes, debts are ‘repaid’ rather than haircut or defaulted upon; the third alternative is a crash or for funds to be forcibly extracted from the citizens and then a crash.

– The Treasury would issue zero-liability US credits — effectively ‘greenback’ dollars — as legal tender under current law or new legislation. Unlike the balance of our money supply, notes would simply be issued by the US Treasury rather than ‘borrowed into existence’ from finance.

– Government fiat has been issued for almost a millennium beginning in China. A notable example of sovereign issue money are Demand Notes first introduced during the Civil War by Edmund Dick Taylor. The notes were necessary because London bankers and their Philadelphia- and New York agents would not extend credit at reasonable rates to the Lincoln administration to fund the onrushing war against the southern separatists (Civil War).

– The notes would retire government obligations on a fixed schedule, for example, the current $19+ trillion$, to be retired over a period of 20 years. The notes could be applied against any liability that is a claim against circulating dollars.

– Payments would be made electronically, out of ‘thin air’, the same way loans are made by banks, as credits on borrowers’ accounts.

– Notes would be legal tender; to repay any debt, private or public everywhere dollars are made use of. Dollars are fungible: Larry Summers notwithstanding, each dollar is the same as all the others. Fiat issuance by the Treasury is the same as fiat issuance by a private sector bank. The difference is no liability to the government issue. The government can provide funds without digging itself deeper into the debt hole.

Loans are simply issued by banks as credits on a spreadsheet. ‘Bank money’ does not exist until a loan is made. The return from lending is the requirement on the part of the borrower to repay with money that is more costly to him than the loan is to the lender. Bank money costs the lender almost nothing to create as it requires only keyboard entries. The borrower must repay with circulating money; he cannot create repayment on his keyboard but must beg, steal or more likely borrow repayment- or have it borrowed by others in his name (government). Whereas interest cost tends to be a small fixed percentage of the principal payable over time, the expense of circulating money is determined by its availability in the marketplace, by supply and demand. When circulating money becomes scarce the real worth of repayment can be much greater than the nominal balance due, yet this is invariably when the demand to repay is fiercest, as during a margin call. If the loan is secured and the borrower cannot repay, he must surrender collateral along with other rights. These are always worth more than a keyboard entry.

US Notes would give the Treasury the ability to make keyboard repayments, to pay lenders ‘in kind’. By doing so the Treasury would remove the currency drain on the private sector (cash demands against depositors).

– What makes up our supply of circulating money is the unpaid debts of others, funds that are ‘temporarily’ out of circulation, overseas (petrodollars) or hoarded. Money created by lending is extinguished when the loan is repaid. The net increase in circulating funds that results from note issue is zero.

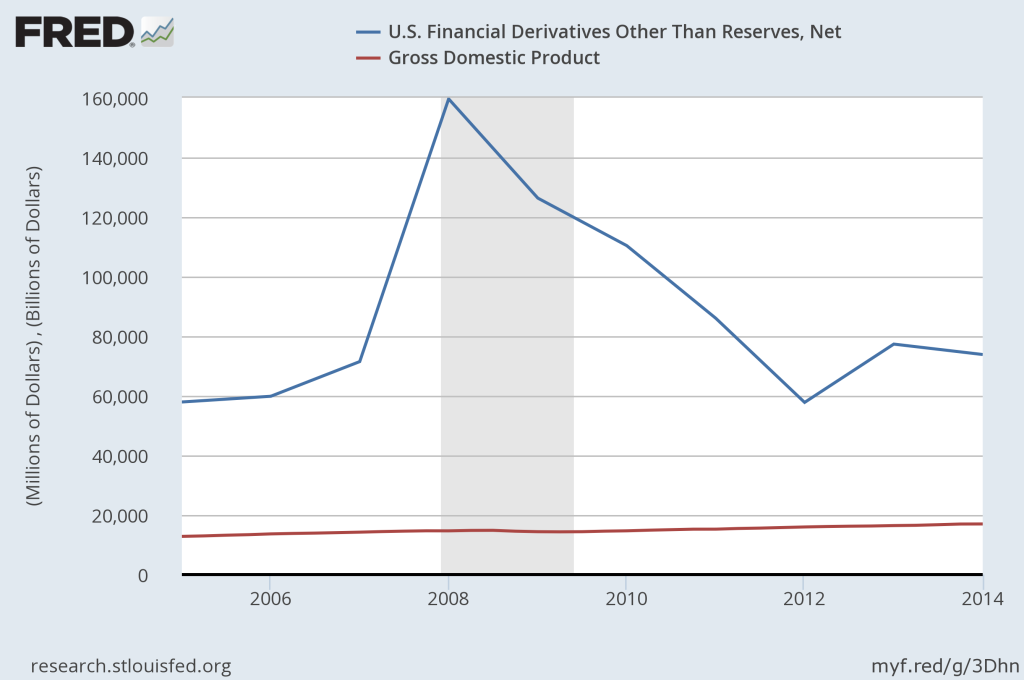

– The Treasury can recapitalize banks directly a with note issue, rather than by bailing in unsecured creditors and depositors. The Treasury could act as ‘issuer of last resort’ in place of- or alongside the central bank. The Treasury can also make up account shortfalls in accounts of deleveraging derivative accounts:

Figure 6: US domestic derivative exposure (dollars) is over four times GDP, (FRED). Unforeseen changes in conditions affecting holders’ collateral position could create liabilities that are too large to meet with funds in hand. Central bank funds are loans lodged against the public. Derivatives shortfall could be made up in any amount with note issue, which would then become a liability tallied against the (criminal) speculators who let their derivatives positions get out of hand.

– Notes would be available in any amounts to plug liability holes until positions could be closed and accounts zeroed out.

– Note issue would re-balance the relationship between banks and sovereigns, the influence of the banking cartel would be reduced.

– Foreign exchange can be leveraged or merged with Note issue. Because the dollar is the primary reserve currency, Note issue would be very effective as a means of backup liquidity everywhere dollars are made use of.

– Lenders would not be able to hold the US or its citizens hostage by withholding funds.

– Notes would render mercantile leverage against Forex unnecessary – dollar depreciation.

– Any fiat regime would require stringent energy conservation as the external (overseas) flows of borrowed dollars to purchase fuel have bankrupted the country in the first place.

– The US and many other countries are in the same situation as hapless Greece. Our debts cannot be retired because our wasteful lifestyle does not provide the means for us to do so.

– Financialization is both incentive- and means to strip-mine our capital base. This regime falls apart under the weight of its own costs. As a necessary component of reform, financiers must be held accountable for their negligence. The present conditions cannot be endured much longer. If managers refuse to act, citizens will take matters into their own hands.

…