Nobody likes bad news:

Bad news: the Trump government says it wants to eliminate medical care for the non-rich, eliminate the Department of Education and cut back the EPA, privatize Social Security and Medicare, repeal the Affordable Care Act … one way or the other, the Federales realize the game is up and are looking to repudiate their obligations, beginning with those to their own citizens. By invoking a bizarre combination of public rage- plus politics-as-usual, the managers hope nobody notices …

default

de·fault

(/dəˈfôlt/)Noun – English

Failure to fulfill an obligation, especially to repay a loan or appear in a court of law.

“it will have to restructure its debts to avoid default”

synonyms: nonpayment, failure to pay, bad debt

“the incidence of defaults on loans”

The strategy is to watch what the managers DO while discounting everything they SAY. The US has been defaulting for awhile but it’s hard to parse out behind the bullish frenzy on Wall Street and the non-stop circus in the media. Current market participants have put default out of mind, preferring instead the fabulous promises … that the US will cull out and expel job-stealing migrants and replace them with robots; build a trillion dollars worth of highways and bridges for the self-driving cars; re-create the Original Maginot Line along the US-Mexican border, cut taxes for corporations and the well-to-do while bailing out the military contractors. Little, if any of this, is likely to happen, the country long-ago passed the point of affordable grandiose gestures. None offer much in the way of returns; they are monuments to nostalgia, waste for its own sake and institutional denial taken to its toxic conclusion.

If we did not supply our own credit, we would be Turkey, looking to invade Mexico to steal their tacos.

The US began to paint itself into a corner before the nation was founded. When the UK became the world’s credit provider at the turn of the 18th century, colonists jumped eagerly onto the bandwagon, borrowing from London bankers with both hands. They were English after all, why not? The proceeds served to finance removal of the natives- then the stripping of the countryside of anything that could be sold. Obligations to repay were expected to fall onto ‘others’ including Europeans who had not yet made their way to the New World and African slaves.

The colonists quickly learned that once on the credit bandwagon there was no stepping off: that a revolution might sever political ties but not alter the relationship between lender and client, nor would it end the mutual dependence of each upon the other. In the face of diminishing returns, the only way to meet maturing obligations and pay interest was to borrow the necessary funds; to continually add more debt … which has compounded exponentially over the intervening decades to the hundreds of trillions owed collectively by Americans today. To insure that obligations are met the government both borrows and spends in the citizens’ place.

Even as governments promise to cease borrowing they cannot; every penny the government spends acts to service the private sector’s debts as well as its own. Far from being productive, industrial economies cannot pay their own way, they require subsidy, all of it borrowed. The need for subsidy expands along with the debts taken on and the cost of debt service. This in turn leads to ever-increasing expenditures, vast national projects such as highway systems, dams, canals, power grids, telecommunication, wars, social safety nets and space programs … Maginot Lines and tax cuts and bailouts. Only governments can spend at this scale, in order to borrow at this scale.

Only governments can ‘bleed red ink’ perpetually and not go out of business! Economies are finite, for one firm- or others to run surpluses (make profits) other firms must run deficits. The private sector is possessed of a singular constraint; by the iron law of capitalism firms cannot run deficits for long and remain in business. The compounding of business failures over time would wipe out the economy entirely unless there is a ‘special’ kind of firm that can run deficits continuously and not fail. This, then is a primary function of the public sector: to borrow at a loss and by so doing enable credit to expand; to put funds into the economy, to retire the debts of tycoons or inflate the worth of favored firms, to roll over debts as they mature and service the rest as long as possible.

Yet, there is an end to it: when the entire borrowing capacity of the economy is consumed by debt service the process implodes; no funds are available to put into the economy or anywhere else. This is the real ‘Minsky Moment’; afterwards, comes the debacle … or ‘reset’, when the debts are written off and creditors are presumably hanged from lampposts.

Money is debt; more reasonably money is a promise to borrow forever: default occurs when borrowing slows for any reason, if it stops the economy collapses.

Less borrowing is what is taking place under everyone’s nose. More to the point, there is a widening mismatch between the massive borrowing of tycoons and firms versus the dribbles allowed to the hoi-polloi whose loans are needed to retire those of their betters. Less borrowing => liquidating the Department of Education and the EPA … liquidating Social Security and Medicare …

“Liquidate labor, liquidate stocks, liquidate farmers, liquidate real estate… it will purge the rottenness out of the system. High costs of living and high living will come down. People will work harder, live a more moral life. Values will be adjusted, and enterprising people will pick up from less competent people.”— Andrew Mellon

Past US defaults have served to increase liquidity and reduce liabilities, they were currency adjustments. Expensive forms of money were swapped out for less costly versions. For example, in 1933, the US abandoned the gold standard and replaced specie with depreciated paper and credit. That — and the bank deposit guarantee — short-circuited the deflationary doom loop that had taken hold in the US after the stock market crash of 1929. The policy also stiffed creditors who expected loans to be repaid with gold. As it was, the creditors were repaid in paper, this turned out to be a small penalty: had the gold standard remained in force the creditors were unlikely to have been repaid at all. The US defaulted modestly in order to avoid the banker-driven Minsky Moment and the total wipe out of credit.

In 1965 silver coinage was replaced with base-metal composites and the public scarcely noticed. In 1971, the Bretton Woods Agreement was abandoned after the Treasury ended international redemption of dollars for bullion. The bad money drove out the good: gold was replaced with dollar credit, the dollar itself was allowed to float freely against other major currencies. What followed the end of Bretton Woods was a ten-year period of uncertainty, energy crises, recession and high inflation … followed by crushing high interest rates and a second severe recession. By 1982 the pain of default had faded; Reaganomics took hold, there were new cheap oil supplies from Alaska and the North Sea. A credit expansion commenced not just in the US but in Europe and Asia that has continued up to the present.

The aim behind these actions was to eliminate the scarcity premium attached to hard currency and to end the arbitrage between it and bank money; to streamline the exchange of commercial credit worldwide, to jettison money possessed with intrinsic value and replace it with abstractions available in unlimited quantity. Default allowed the US to become the world’s greatest manufacturer of credit, which in turn allowed Americans to gain a bounty of goods and resources from around the world in exchange for empty promises borrowed from Wall Street at interest … promises the resource- sellers themselves would have to make good at some point in the indefinite future!

At the same time, our post- Bretton Woods money would always be worth less than commerce, eliminating any incentive to hold it. Buy! Buy! Buy: over the short term, the outcome was an increase in world commerce and spending with borrowed money = more GDP growth which itself was- and is an indirect measure of the increase in the money supply.

GDP = an indirect measure of the increase of unsecured lending at the bottom of our difficulties. Our ongoing default is much different from prior currency modifications. There is the arbitrage between the dollar and other currencies, there is also collateral inadequacy, diminished returns on credit and the failure of credibility of those in charge of it. Our default is serious business, a reaction to the erosion of our national balance sheet, the longer term consequence of an economy built around non-productive waste. The US is following the same road as Greece, the difference is timing and the relative toxicity of denial. The can-kicking, key man propping strategies, the manipulations and plots have all failed. What’s left is to pretend … and to send in the flaming elephants.

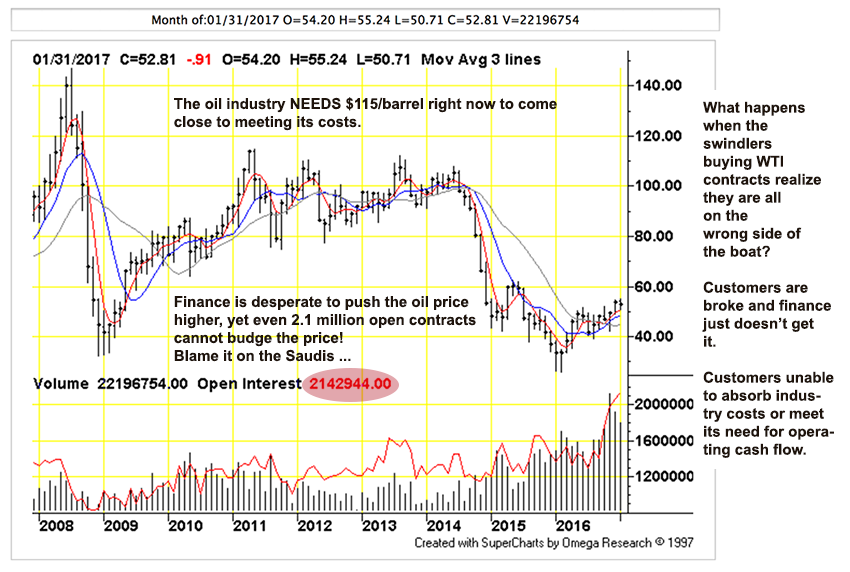

Figure 1: Unlike the equity markets, oil market is sputtering. Millions of bullish contracts @ WTI futures and the oil price is stuck below $60/barrel; (TFC Charts, click for big) Bad news: the oil industry’s customer base is broke and cannot afford expensive petroleum.

More bad news: expensive petroleum is the only variety we have left. An oil price sufficient to satisfy the cash flow demands of the drilling industry and allow the extraction of the needed volumes is far out of reach. We have built our economy around the waste of cheap resources, fuel is a loss leader for expensive real estate and automobiles. Even a moderately higher ‘low price’ is enough to torpedo our non-remunerative, credit dependent, chest-bursting puss-bag of an economy.

For oil prices to rise, there must be someone able or willing take on the final costs. While the major media endlessly serves up the ‘rebalancing’ meme and its lies about the utopia to come, not one word is spared for the hapless end-users whose borrowing keeps the entire enterprise afloat. Customers cannot generate their own wealth, they are tapped out => less borrowing => default.

End users’ failure is no accident. Policy makers since 2008 have worked hard to repress them, particularly those in developing countries. Monetary policy — including QEn almost everywhere — has seen countries beggaring their neighbors in an endless round-robin, in the attempt to depreciate their currencies and gain the export advantage. The robin also rises: you have to know something is seriously wrong when you are unable to fail no matter how hard you try! In the currency war, everybody loses: depreciation pushes every citizen in a country toward poverty by degrees. The citizens borrow less => oil prices decline => less funds available to retire driller loans => banks become insolvent along with the entire oil industry … everybody loses!

The oil market prices both oil AND dollars. Both sides of the dollar-oil market are caught up in tightening positive feedback loops. When customers can only afford a modest price for fuel, how much reserves at that particular price are available? Not much because humans have been burning cheap oil for 150+ years and the cheap stuff is long gone! Meanwhile, lower oil prices mean the dollar is worth more. More costly dollars => hoarding => less borrowing (it costs too much) => default. This is all nominal, of course, but we all live and work in the nominal, immediate world: if quantities did not matter there would be no billionaires.

With industrial output becoming more a product of machines and vanishing petroleum, the ability of labor to do much of anything other than ‘consume or die trying’ is shriveling. There are millions of professional economists in this world but few- if any of them concern themselves with the absence of economic return on consumption.

Oil price is now the channel by which credit breakdown propagates itself though the economy, (Quartz):

In an announcement today, Exxon said it had written down its proven oil reserves by a massive 19.3%, a stinging reduction to what is a primary measure of any oil company’s value. As of the end of 2016, Exxon had 20 billion barrels in proven reserves, compared with 24.8 billion a year earlier. This includes the erasure of all 3.5 billion barrels of Exxon’s proven oil sands reserves at Canada’s Kearl field. Last year’s low oil prices made it uneconomical to drill at Kearl, which had been at the core of Exxon’s growth strategy.

It’s uneconomical for Exxon because it is uneconomical for Exxon’s customers, soon enough uneconomical for Exxon’s shareholders. Exxon will survive as an independent firm only as long as its lower cost, conventional oilfields continue to be drained; only as long as there are banks willing/able to lend to it.

More cracks in the edifice of denial, from last September’s research report by (HSBC):

– Oil demand is still growing by ~1 million barrels per day every year, and no central scenarios that we recently assessed see oil demand peaking before 2040.

– 81% of world liquids production is already in decline (excluding future redevelopments).

– In our view a sensible range for average decline rate on post-peak production is 5-7%, equivalent to around 3-4.5 mbd of lost production every year.

– By 2040, this means the world could need to replace over 4 times the current crude oil output of Saudi Arabia (>40mbd), just to keep output flat.

Anyone paying attention to petroleum subjects over the past few decades has seen this before, but almost never in the mainstream. Instead, there is endless public relations blither about fracking, technology, efficiency and an ‘energy revolution’ which is proving to be too costly for the consumption economy to afford.

In this report, we look at the theory and practise of decline rates. We have reviewed several academic studies on declines, notably, the IEA study from the 2008 and 2013 editions of its annual World Energy Outlook and the University of Uppsala (Sweden) papers published in 2009 and 2013. The IEA and Uppsala studies were based on the analysis of over 1,600 fields (covering two-thirds of global oil production) and just under 900 fields respectively – large enough to be statistically significant.How quickly is production declining?

The studies we have compiled (IEA and Uppsala) coincidentally appear to agree on a ~6.2% average post-peak decline rate. Decline rates are higher for offshore fields and smaller fields, reaching 12% or more for deepwater fields and for fields of less than 100mbbls. The chart below shows the IEA’s average post-peak decline rate calculations for various field categories and sizes:

Anything like 5% or above is a kick in the pants. Since ’08 increases have been meager but increases nevertheless. Even so there is the stumble into delinquency and default. It is hard to imagine the status quo shrugging off reduced fuel availability at any percent much less the declines suggested in this report. No wonder the bosses are panicking; they are passengers on the Titanic throwing deck chairs overboard and setting lifeboats on fire. They cannot think of anything else to do: panic, blame others and lie about everything.

The bosses panic while the rest sleepwalk toward the television. The HSBC report is nothing new, but what of it? Since the beginning, when the first European staggered out of a rowboat onto the Virginia shore, our people have embraced ignorance; living in denial about our debts, about our relationship to others here before us, about the Europeans and our non-European ‘laborers’ we imported; we’re in denial about resources and our limitless greed and rapaciousness, our business folly and waste; in denial about our relations to other nations and what these peoples mean (and don’t mean) to us; in denial about our interrelationship- and absolute dependency upon a complex web of living organisms making up our life support system; also our relationship with reality and how that reality has transferred whole to our entertainments while it is stripped, pounded, genetically modified, cut, drilled and sold to nothingness on the installment plan outside our front doors …

The imaginary intergalactic spacecraft in our movies are remarkably real; denial has been given the gloss of a high art like public relations or maybe a replacement for it. Underneath the glossy exterior is disease. As in the movies, we invent our monsters, make them real and give them power over ourselves then set them loose to do what they will and we laugh … a kind of perverse last chance at something or other we cannot put a finger on. We’ve been practicing our lies for too long: there are consequences, the lies become poisonous from over use, the monsters we have made of ourselves.