Led by these mighty knights of the automobile industry,

the steel industry, the radio industry… and finally joined

in despair, by many professional traders who, after much

sack-cloth and ashes, had caught the vision of progress,

the Coolidge market had gone forward like the phalanxes of Cyrus,

parasang upon parasang and again parasang upon parasang …— Prof. Amos Dice, from ‘The Great Crash’ John Kenneth Galbraith

Since 2009, Americans have been privileged to participate’ in one of the great Wall Street bull runs in history. It is the longest other than the rally from October, 1990 until March of 2000. There have been other great runs; none quite so bizarre as ours considering the economy of much of the world is coming apart at the seams. Credit the banks and their ability to make magic, to lend enormously into the void, to deny reality.

Figure 1: Dow bull markets compared, Notice the little green line that goes up and down precipitously – the Roaring Twenties: (Schaeffers Research).

Bull markets are both psalms and proverbs of the progress narrative; they are driven by ruthless Ayn Randian ‘innovators’ and risk-taking ‘entrepreneurs’ who become rich by dint of their genius, producing gadgets heretofore only imagined, items revealed in the fullness of time to be indispensible.

The car industry is central to this narrative, its products and dependencies were the ‘tech story’ of the 1920s, as smartphones, and Bitcoin are today. Like today’s gadgets, the auto was disruptive: cars were fun to play with and conferred status on the owners. Driving challenged operators as there were multiple ways for the things to murder- strand or otherwise embarrass those who were unlucky or not paying attention. The challenge was part of the fun: industrial workers generally served the needs of their employers, they were slaves to the machines. Cars worked the other way ’round: the machines answered the desires of the operators, the interactivity between the two was a novelty.

More practically, cars offered an alternative to the grip of railroad monopolies and from the, uh … ‘languidity’ of shoe leather, horse-drawn carriages and steamships. It also promised to transform what up to that point had been an unending liability — distance — into an massively valuable asset. Talk about progress: America was a big country that was largely ‘underutilized’. The auto would convert scruffy backlands and hard-scrabble farms into valuable suburban developments; the farther away they were the greater need for auto ‘tech’! Adding more suburbs meant adding more automobiles. The more automobiles, the more areas to be set aside to accommodate them. Needless to say, the money-making potential of this process appeared to be without limit.

For the car industry, its rise was universally virtuous, coinciding as it did with Wall Street finance, the rise of media and marketing, of oil extraction and processing; of industry itself: steel and radio, heavy manufacturing and construction, tool-and-die making, foundry, precision machinery and materials handling equipment along with incremental automation. Along with millions of new cars, thousands of destinations were needed along with new paved roads to knit them together: all of this offered the promise of millions of new jobs. Also, service stations, refineries, pipelines, terminals and ports: electricity would be needed to power these things, money was needed to pay; in advance, on the barrel-head, borrowed at six percent or better.

During the ’20s, government was oblivious; the freshly elected Hoover regime of 1928 was like all others before or since: a prosperity government. The idea behind modern politics is that the various publics (and their bosses) are entitled as a birthright to live beyond their means. It was and is the responsibility of government to provide … or else a new collection of big-business lackeys government would be installed.

Part of governments’ responsibility is to make necessary resources available to business cartels at the lowest possible cost. Politicians were expected to lightly manage the prosperity that resulted; making certain that those at the bottom of the economic food chain were not over-supplied. The expression of this idea can be found in every kind of government including the dictatorships, republics and monarchies, constitutional and otherwise: all of these are prosperity governments. The various politics functioned more or less because there were always more resources to exploit: apparent resource growth and accompanying gross domestic product was able to race ahead of populations and their advertising- driven expectations.

In 1928, both government and industry were eager to genuflect in the direction of self-serving pieties. The tried-and-true (antiquated) ideologies of gold standard, ‘sound money’ and laissez faire non-interference in private sector affairs were universally embraced. Regulation was an anathema, government borrowing during peacetime was frowned upon, neither of these conformed to the ‘small government’ orthodoxy of the time. Regulation would only stifle innovation. Public sector borrowing could only crowd out private borrowers and starve businesses of funds. Yet, even as the car- and related industries expanded explosively using borrowed money, borrowing at the consumer level — top line business revenue, cash flow — was faltering. Deprived customers, the ‘little fish’ at the bottom of the economic food chain were unable or unwilling to borrow to service and retire the industries’ heavy debts.

The American middle class at the time was enthusiastic but too small to carry the burden assigned to it. Most of America’s 120- or so millions were small farmers or laborers providing services related to agriculture. Returns were meager; farmers swept up relatively inexpensive, durable Fords and retired their horse carts, by doing so they removed themselves from both cart- and car markets. Non-union industrial, service, extraction labor tended to be ‘wage repressed’; only a few could afford to buy a car. Accounting, management, retail, marketing, clerical and other ‘white collar’ employment was paid well enough but represented a modest fraction of the workforce. They filled the big cities’ close in ‘trolley suburbs’; they were not inclined to buy second or third houses … or second and third cars. By the start of the Hoover period, the markets were on their way to becoming saturated. Demand for goods started to decline and then commodity prices. Instead of the once-certain returns from industry, there was a more general turn toward speculation financed with debt ‘on the margin’.

“Mitchell asserts stocks are sound; Banker, Sailing From Europe, Says He Sees No Signs of Wall Street Slump. Predicts more mergers, declares Movement Will Continue With “Fusion of a Number of Big Banking Groups.”

— New York Times. October 16, 1929

By October, 1929, the government had made itself irrelevant almost by habit; business was left to its own devices. Managers appreciated this but did not grasp the consequences: they were marching purposefully into a pit of their own making, there to remain until the rise of a more ‘innovative’, ‘entrepreneurial’ government in Hitler’s Germany … and the world’s necessary response to it.

Dow crosses 24,000 mark as banks climb, techs rebound(Reuters) – The blue-chip Dow Jones index raced past the 24,000 mark for the first time on Thursday, propelled by further gains for bank stocks and a recovery in technology shares.

The 30-member index has crossed four similar 1,000-point milestones this year on the back of strong corporate earnings, robust economic data and hopes that President Donald Trump’s tax plan would make headway.

Today, the government purposefully aims to do the same thing, to become irrelevant, to shrink itself until it can be drowned in a bathtub; to give free rein to gamblers without heed, to do so in order to answer obsolete ideological concerns. How can this end well? Speculation by nature escapes all bounds, taking on a life of its own. In the late ’20s there was a speculation frenzy in stocks and real estate. Now it’s bonds, stocks, real estate, art … the ‘everything bubble’. The consequences are not grasped: the fact of out-of-control speculation indicates the economy of physical goods and services is kaput: there is no more ‘real economy’: it’s gambling or nothing.

Stock prices have reached “what looks like a permanently high plateau,” Irving Fisher, Yale economist told members of the Purchasing Agents Association at its monthly dinner meeting at the Building Exchange Club, 2 Park Avenue, last night.After discussing the rise in stock values during the past two years, Mr. Fisher declared realized and prospective increases in earnings, to a very large extent, had justified this rise, adding that “time will tell whether the increase will continue sufficiently to justify the present high level. I expect that it will.”

— New York Times, October 16, 1929

Now as then, bank money flows like a river into speculative assets driving up prices without any change to the nature of the assets themselves. These loans are basically unsecured. Giant firms borrow to buy their own shares, removing them from the float of those publicly available. The resulting scarcity premium is added to ‘fundamental’ share prices. There is nothing else to justify the increase; a market manipulation that has little- or nothing to do with firms’ returns.

The credit flood increases because it must; how else to meet the credit-driven high prices? Going forward, there is no other choice but to lend and to do so without restraint. Industrial business is fundamentally non-productive: it exhausts its capital and ‘manufactures’ entropy as its sole product. Neither the exertions of human labor or the application of new machines can hope to retire industrial debt. Only more loans can do this: lending must continue to expand or the entire enterprise falls off the cliff: ‘once on the debt treadmill it is impossible to step off’ …

While not all land speculating met with success, most investors in the beginning stages of the Florida Land Boom made a profit selling the land to others. An elderly man in Pinellas County was committed to a sanitarium by his sons for spending his life savings of $1,700 on a piece of Pinellas property. When the value of the land reached $300,000 in 1925, the man’s lawyer got him released to sue his children.— Florida History

Fool me once … fool me over and over again! Even if lending continues without hesitation or restraint, it cannot do so forever as service costs are compounding, at some point marginal lending capacity is directed to debt service: the true ‘Minsky Moment’.

Moas now puts the line in the sand at $20,000 for the split-adjusted price when the new year hits. Looking at how things have gone so far for Moas, a month is a long time, and perhaps $20,000 will be broken before that time.Tom Lee, rather conservatively, set a Bitcoin growth of 40 percent to happen by the middle of 2018. His prediction put him at $11,500. That prediction was made a week ago, and in that time Bitcoin topped at around $11,300.

Max Keiser has a much more bullish view, but over a longer time frame as the host of Russia Today’s Keiser Report believes that $100,000 Bitcoin is an eventuality.

— Coin Telegraph, 2017

Uhhh… about bitcoin… it’s actually ruining the planet.

The bitcoin computer network currently uses as much electricity as Denmark. In 18 months, it will use as much as the entire United States.

Something’s gotta give. This simply can’t continue.

— Eric Holthaus (@EricHolthaus) December 5, 2017

Excess credit inflates the cost of new bitcoins which are basically math puzzles requiring increasingly expensive computing power to solve. Interesting … but to what end? The entire enterprise is the red-headed stepchild of unrestrained leverage: without bank credit, the gambling component and higher ‘bubble’ prices, bitcoin transactions and the infrastructure that supports them would be unaffordable. Like the incestuous/harmonious circular relationship between automobile and suburb, the relation between leverage and the ‘pseudo-currency’ is virtuously self-amplifying … up to a point: more bitcoins => higher prices => more bitcoins. In the end, the regime self-defeating because of the exogenous credit (and electricity) requirements. More suburbs => more cars => more sub … oops! More suburbs means older ones cannot generate the revenue needed to maintain them. More cars means it’s impossible to get anywhere because of the traffic!

The cryptocurrencies are Ponzi schemes, little different from those erected by Clarence Hatry and the ‘Match King’ Ivar Kreuger in the 1920’s. The term ‘currency’ here is simply a narrative flourish intended to shill the Ponzi as ‘innovative’. As with all other schemes of this sort the great majority of suckers who ‘invest’ in cryptos will lose everything, like those who invested in Goldman-Sachs’ Shenandoah- and Blue Ridge Corporations just before the crash:

Most exciting of all were the holding companies and the investment trusts [in the very late 1920s]. Both were companies formed to invest in other companies. And the companies in which they invested, invested in yet other companies that, in turn, invested in yet others. The layers could be five or ten deep. Along the way bonds and preferred stock were sold. The resulting interest payments and preferred dividends took some of the earnings of the ultimate operating company; the remaining earnings came cascading back to the common stock still held by the promoters. Or this happened as long as the dividends of the ultimate companies were good and rising. When these fell, the bond interest and preferred stock soaked up all the revenues and more. Nothing was left to go upstream; the stock in the investment trusts and holding companies then went, often in a week, from wonderful to worthless. It was an eventuality that almost no one had foreseen.— ‘The Age of Uncertainty’, John Kenneth Galbraith

Nothing lasts forever, particularly bull markets. Hyman Minsky observed periods of prosperity and accompanying bull markets carry with them the seeds of their own destruction. Certainly after almost ten years of credit floods and manipulations the seeds are ripened.

If you see a Swiss banker jump out a window, jump after him. There’s surely money in it.

— Voltaire

Just don’t jump out unless it’s close to the ground, good advice that’s rarely followed. Both manias and crashes are expressions of the ‘Paradox of Thrift’, a condition that ordinarily prohibits one-way markets — one where all are buyers or all sellers (or all are thrifty). One-way markets cannot exist for long without severe consequences. A market where all participants are buyers means a market that is ultimately deprived of them. Everyone who is willing to buy expensive bitcoins, tract houses, Leonardo paintings, Manhattan penthouses, Tesla shares has done so: no one remains able to ‘buy from the buyers’. A market where all are thrifty is one where money is ‘saved’ out of circulation so that day-to-day business becomes impossible. A speculators’ market unravels when the supply of free-spenders is used up, then all are forced by conditions to become sellers at once …

Over time, citizens have been made over into ‘consumers’, investors have been forced into becoming speculators: this is the paradox of non-thrift. Americans are forced into penury on account of it, there is too much ‘stuff’ too much quasi-businesslike nonsense; goods have been over-consumed leaving markets that are saturated. As during 1928, businesses cannot endure periods when there is no consumption and they fail, the outcome is the same as too much thrift. Instead of a shortage of currency, there is the shortage of timely demand.

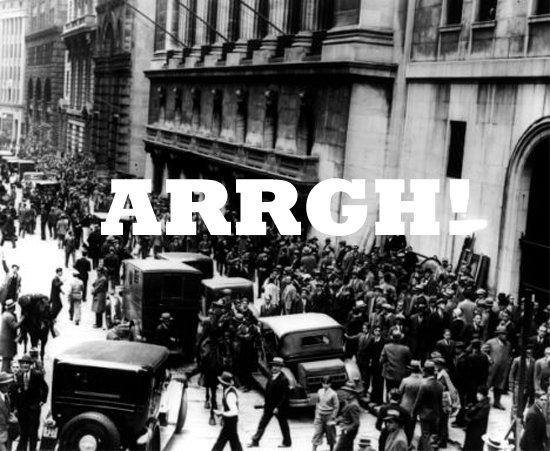

Unknown photographer, crowd outside the New York Stock Exchange building during Black Thursday, 1929.

Q: How would you describe the economy?

A: It is a system that allows a select few to borrow immense fortunes. The rest of us; you, me, everyone else, repay the debts.

Q: That’s it?

A: That’s it.

Donald Trump’s tax plan may not be perfect but its timing is: The world’s powers have just wrapped up their central banks’ Quantitative Easing giveaway to tycoons and corporations that began in 2009. Now the tycoons look to government with upturned fluttering hearts. In any case there is little but obligations for those at the bottom of the economic ladder. An unhappy consequence of QE was the oil price crash of 2014. As in 1928 the little guys lacked the credit to bid up the price of fuel. Without high prices, oil drillers were, and still are, underwater.

Tycoons and corporations have taken on more than debt than the rest — and their children — can ever hope to repay. Without credit access to those at the bottom of ladder, the tycoons must retire their own loans. By doing so they become non-tycoons just like everyone else. Thrift — whether it’s intentional or not — denies the tycoons funds, they are ruined by their own creditors, the creditors are likewise ruined. This is happening right now, behind the speculative razzle-dazzle; the steady pauperization of those at the bottom. The rise in asset prices offers a false impression, or more likely, gives a warning …

The only market indicator that matters, the price of gasoline: $2.50 per gallon is affordable for most Americans, over $3.50 and ‘problems’ start to appear in various world credit- and currency markets as they did in 2008. A worrying sign is the nearly three dollar price jump for premium gas, the kind required for luxury- and high performance cars. No wonder owners of these cars are begging for a tax cut.