While nobody was looking, a new year snuck in and took over. What do we get, besides older?

How about a free lunch?

Welcome 2,017.386. Are we having fun yet?

Nothing much has changed since last year, nothing much from the years before that. Life appears easy because we don’t have to do anything but sit back and let the days spool out one after the other; mad, bad and dangerous to know, like Lord Byron. The physical becomes metaphysical under our noses: we inhabit both the ‘Age of Less’ and the ‘Age of Nothing Less’ at the same time. “Impossible,” we cry but think of the convenience efficiency!

The driving concept of twilight industrialism turns out to be nothing. It’s the perfect crime; after all, what can ‘nothing’ be charged with? A: nothing, that’s the beauty of it. We are uneasy about ‘nothing’ because we understand the blind-alley-ish implications, because we can get away with murders we are soon enough infested with them. With nothing in hand the detectives have just that to work with. What can anyone do? Boiled down to its essence nothing … is semantics: a roman à clef, the void, a ‘kinder, gentler’ death, something like ‘compassionate conservatism’.

Meanwhile, in its artless manner, ‘less’ advances relentlessly without attention behind the blank veneer of pillow talk, public relations, marketing non-sequiturs and random violence.

At this point I'm just like, whatever.

— God (@TheTweetOfGod) January 20, 2018

Problems, problems; nothing is fixed. The difference is the fresh coat of invisibility paint like something out of a Roadrunner cartoon. The new paint allows us to pretend progress is finally working after centuries of demonstrable … um, something or other? Because the emergencies that concerned us as recently as last year are now a decade safely past, we get to pick and choose exactly what we will forget. Economists declare the US economy has hit its stride at last! Nobody asks questions because everyone knows the answer is a shrug.

You have to wonder how guys like John Hussman keep going month after month, year after year. David Rosenberg switched to bullish years ago and never looked back …

Last week, Investors Intelligence reported the most lopsided bullish extreme in over 30 years, with 64.4% of investment advisors bullish and just 13.5% bearish. Likewise, the Daily Sentiment Index for both S&P 500 and Nasdaq futures reached the most extreme levels in their history.

Hussman weeps bitter tears of free lunches not eaten:

In hindsight, the stupidest thing I ever did as a professional investor was to imagine that there was some limit to the stupidity of Wall Street.

How could the smartest people in the room repeat the same errors that blew up so badly not quite ten years ago?

The answer blows in the wind …

That comment may not seem terribly humble, but as a dear friend and mentor once told me “There’s a difference between humility and false humility.” Sometimes you have to speak your truth if you believe it will be helpful to someone, even if others don’t want to hear it. I’ve got no antidote for those who believe that the dot-com bubble, the housing bubble, or the current “everything bubble” are more than a salad of reckless speculation, herd mentality, and fear of missing out. Having anticipated the collapse of the other two bubbles, and correctly projecting the extent of those losses, it’s clear that my error in this bubble was to underestimate the tenacity of blind speculation (and fail to take advantage of it). The error wasn’t overlooking some kind of justified or durable legitimacy to this madness. As I wrote at the March 2000 bubble peak, just before the S&P 500 dropped by half, and the Nasdaq lost four-fifths of its value, “On Wall Street, urgent stupidity has one terminal symptom, and it is the belief that money is free.” Here we are again.

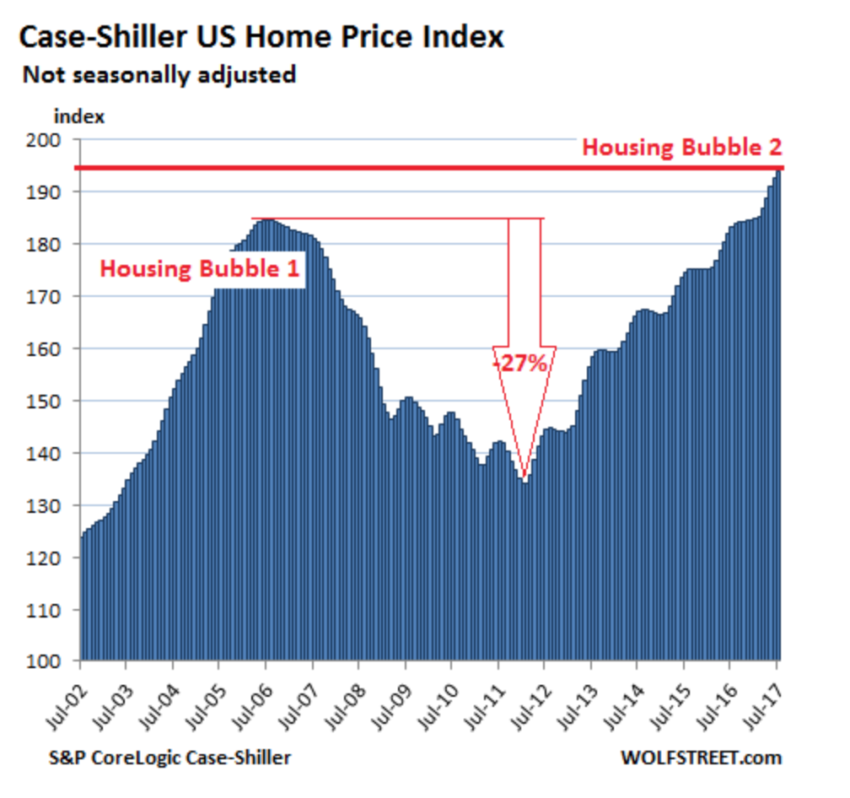

Here is the ‘Son of Housing Bubble’, a monument to forgetfulness:

Figure 1: The S&P CoreLogic Case-Shiller National Home Price Index from Wolf Richter, (click for big). As Andy Xie pointed out a few months ago, these are the same houses that were worth a fraction a few short years ago. What has changed are the numbers and nothing else.

What is said about it or done? A: nothing. Having burned through a large percentage of our non-renewable resource base (wealth), asset price inflation is about all we have left. We Americans live for the bigger number. When our numbers shrink we can blow our brains out or get drunk. Or we go to the government and demand bigger numbers as our birthright.

What Happens When Your Number is Up?

“Deja Vu all over again,” said Yogi Berra: because nothing changes, nobody can tell if the recession is really over or if it has just started.

– Public corruption and the purchasing of influence by corporations and special interests = nobody cares as long as the numbers go up.

– The ‘revolving door’ of officials taking jobs with companies that they formerly regulated = the normal course of business.

– Unprincipled partisanship.

– Undisciplined populist style pandering to extremists = these are some very fine people (if you squint).

– Corporate welfare, including:

– “Too Big To Fail’, public support for monopolies and cartels = citizens are compelled to compete against their own government!

– Accelerating concentration of wealth and resources in the hands of the (inept) few: the widening gap between rich and poor and the erosion of the middle class = good for elites and a handful of economists, an unsupportable burden for everyone else.

– Uneducated policy makers = ignorance is bliss.

– Bottomless conflicts of interest = it isn’t a conflict if it’s part of a business plan.

– Election processes corrupted by private funds and advertising = a little whining but nothing that would make a change.

– Erosion of Constitutional protections limiting intrusions of state power into the lives of the citizens; a little whining but otherwise = nothing.

– Creeping privatization; the rise of ‘Shadow’ states- within- the- state such as private militias and security departments, the transfer of public assets to private interests for private gain.

– A wasteful and incompetent military establishment which is rewarded for failure after failure => the absurdity of a US ally by treaty bombing a US ally in fact = who cares?

– The shift from a public military to a mercenary military = not a topic of discussion.

– ‘The Untouchables’: unquestioning support for the defense/security industrial complex and its excesses = platitudes as a substitute for strategy.

– Unaccountable intelligence services and opaque intelligence gathering activities, including torture, domestic spying and detention- without trial.

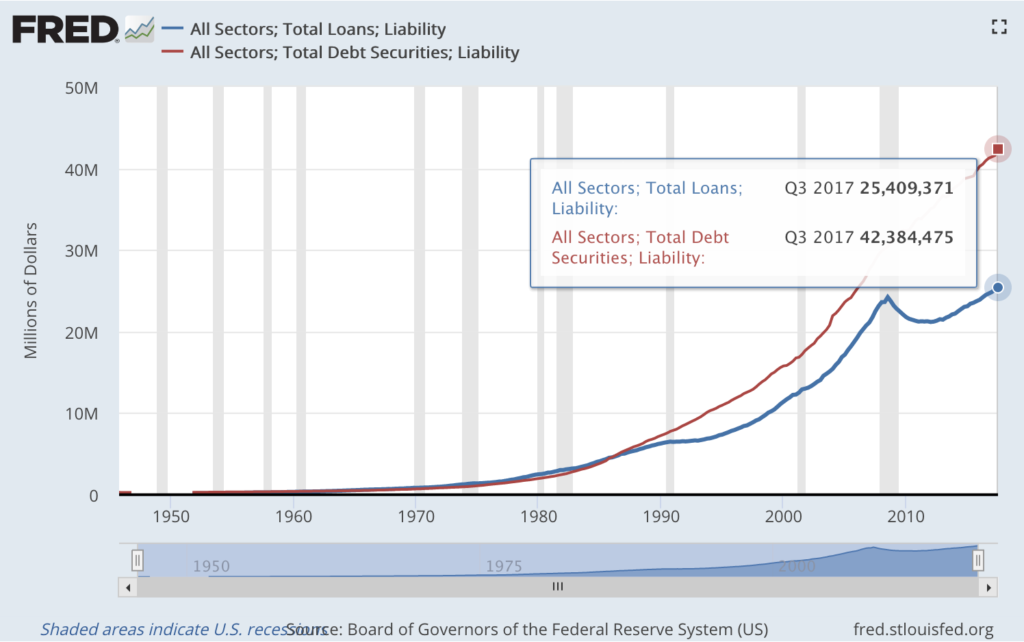

– The explosive expansion of liabilities …

Figure 2: – Add the red and the blue together = near $70 trillion in credit market debt excluding retirement- and pension obligations, public sector compensation and medical care programs = you can’t freak out about a problem if you don’t see it.

How does the amount of credit market liabilities square with the notion of a ‘sustainable’ industrial economy? The Western economy is really a debtonomy’ where the primary function is to borrow; all else is window dressing. Is there a discussion about any of this?

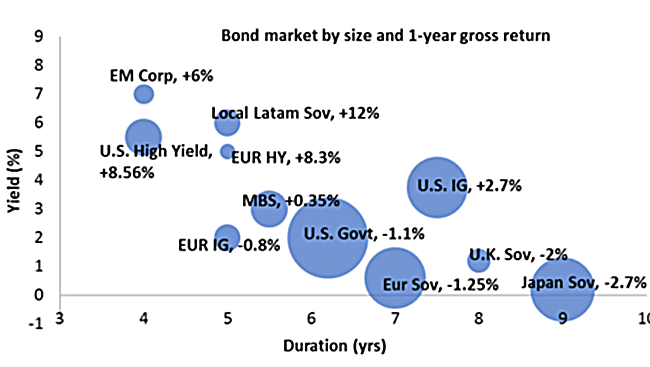

Figure 3: Bond ‘bubble’ by way of Bloomberg. Again, people on the economic fringes complain – including opportunistic politicians – but nothing is done.

– A rising and general sensation of high- level public lawlessness, that invariably translates into private lawlessness at all levels.

– The failure to formulate a population policy or even discuss one other than to proclaim, ‘it doesn’t matter’ … includes the failure to discuss any other policy: the ‘strategy of nothing’!

– The failure to discuss the material requirements and costs of lifestyle: meeting the ever- expanding marginal costs against ever- shrinking marginal returns. When is this topic ever heard about or seen in print?

– Commercial imperialism and the hegemony of commercial interests at the expense of all else, including longer term US political and security interests. What’s good for JP Morgan-Chase (Citigroup, Boeing Aircraft and Facebook) is good for America!

– The privatization of business profits along with nationalization of private losses: ‘Socialism for the bosses, capitalism for the workers!’

– The institutionalization of impunity and moral hazard: that select individuals and firms can do as they will without regard for any consequences. What is ever done about this? A: nothing …

– Failure of the Establishment to prepare the country to withstand economic hardship = because economic hardship is never going to happen. Right?

– Reliance on propaganda – lies – as a primary policy tool (non-policy tool): ‘Potemkinism’.

– Structural impediments to productive employment and failure on the part of the Establishment to create effective employment strategies … outside of shipping high-paying US jobs overseas and relying on ‘illegal aliens’ for cheap labor.

– Pandering to religions, religious interests and cultists.

Stupidity Scales.

– Policy horizons are too short: the crisis of the next five minutes overrides the challenges of next week. Borrow short, lend long. Make that quarter. What about five years from now? You’ve gotta be kidding!

– The erosion of (true) capital as the byproduct of short-termism: eating the seed- corn. What do we hear about gobbling up our (sole) basis of support? A: absolutely nothing.

– Fraudulent accounting at all levels: the wilful ignorance of externalities as well as off- balance sheet manipulations, ‘extend- pretend’ and ‘mark to mockery’ control frauds.

– The tolerance of finance- level black markets: the shadow banking system.

– The rejection of economic restraint or self-discipline. “If I don’t do it, somebody else will.”

– Willful failure to restructure bankrupt firms that make ongoing claims against the public!

– An economy based on the monetization of waste, speculation and rent-seeking. Again, there are a few economists who complain but otherwise = nothing.

– The declining national level of critical thinking, skills and artistry. America, has become a nation of boobs fucking morons!

– Refusal to include natural resources and carrying capacity in policy level economic discussions = more ‘Strategy of Nothing’.

– Refusal to understand the fundamental nature of money and credit! This is mind- boggling in an establishment that claims to gain wealth by the manipulation of money and credit!

– Conflicts of interest involving economists and the agencies (central banks) which employ them.

– A multi- decade malinvestment in a physical and social plant that is stranded by its material and credit inputs.

– A multi- decade malinvestment in an economic metric that requires the constant input of new funds to pay returns – the ‘Ponzi economy’.

– Over reliance on automation and technology = smart machines, stupid humans.

– Industry- assembly line modeled social infrastructure such as education and ‘wellness’ systems which have all failed except as sinks for borrowed funds.

– A physical plant that is over- leveraged to the automobile.

– A counterproductive ‘War On Drugs’ (non-)policy.

– A perverse trade policy which depresses American business profits by means of ‘wage arbitrage’ = cheap labor, domestic or otherwise, cannot earn enough to support high- cost US businesses.

– Governments depend upon an accelerating levels of consumer waste which leads to repeat cycles of subsidies, failures and more subsidies.

– A cavalier disregard to the consequences of pollution and resource depletion.

– Public ignorance of the exponential function and thermodynamics.

– The elevation of fantasy and wishful thinking to equality with scientific facts as an element of the public policy discussion.

The (Fiscal) Policy of Nothing

– Mal-investment in unproductive enterprises = the endless bailouts and ‘key man propping’.

– Inability to hold finance accountable for its actions and/or negligence.

– Inability to enforce laws on the books against theft, influence peddling, racketeering, corruption and fraud.

– Inability to reject useless and counterproductive initiatives – ‘picking winners’.

– Top- line support for monopolies and foreign business interests.

– A government fiscal policy that is dependent upon bank credit.

– The absolute lack of any energy policy (other than using the military to steal consumption from other countries!)

– A ruinous and counterproductive tax ‘system’.

– Incoherent public accounting.

– Misleading, manipulated and inaccurate economic data = something else very few bother to mention.

Figure 4: Is there inflation or not? Velocity of M2 money stock says ‘no’. Meanwhile, prices of everything rise. Who are you going to believe?

– The abdication of serious economic policy making: deferring to a pretend ‘free market’ which doesn’t exist, kowtowing to the corrupt finance/banking apparatus.

– The shift away from the fruits of labor toward gambling and speculation;

– The uncontrolled expansion of uncollectable claims against productive labor: even if labor is granted unlimited amounts of time, it cannot retire finance level debts, even at the exorbitant wage rate of $15/hour.

– The politicization of regulation; regulatory capture as the means to advance partisan interests.

The Central Bank Illusion

– The over- reliance upon monetary policy to effect economic output, even when it is clear policy does … wait for it … almost nothing.

– Central Bank look to gain more authority = what they have now- plus what they might gain adds up to … nothing!

– Central banks are opaque, they do not allow audits of their activities or those of their clients; instead, obfuscating jargon.

– An inflationary bias to Fed monetary policies despite claims to the contrary. Because the economy is a debtonomy, it is dependent on new credit to service and retire loans already made. The addition of new credit depreciates the credit stock. The diminishing worth of credit over time is how the ‘real cost’ of lending is reduced, hence the desire for 2% inflation.

– A reliance on ‘carry trades’ — forex arbitrage — as a source of credit.

– This follows along with the abdication of monetary policy to ‘outside’ interests.

– The false premise of Fed effectiveness regarding deflation = you mean the deflation that would immediately appear the second banks were unable- or unwilling to lend?

– The general acceptance of questionable central bank activities because the ‘end justifies the means’.

– Manipulation and interference by the central bank in non-money markets.

– Ignoring bank crimes: substituting liquidity for oversight; aiding and abetting Wall Street crime as a form of monetary policy.

– Liquidity malfeasance; finance starving the Main Street economy while flooding finance; the bankers’ left hand lends to the right hand.

– Failing to recognize the deflationary implications of oil price upper bound and peak oil = not part of the discussion.

– The seemingly endless negative- or near zero real interest rates: punishing the prudent while rewarding gamblers. Meanwhile, central banks have been trying for the past several years to ‘jawbone’ market rates higher as the only tool bankers have to ‘fix’ the inevitable crisis is negative real interest rates.

– Currency and forex imperialism including flooding the world with dollar credit. = This is never even discussed except in the most general terms.

Americans believe they are entitled by divine right to free lunches, a kind of superstition. When leadership fails to provide the lunches = new leadership is found. After several rounds of replacement leadership it is hard to avoid the conclusion that the entire free lunch idea is obsolete. Where do we go from here?

Back to sleep!

Wake me up when ‘nothing’ is over.